Speech by IMF Managing Director Kristalina Georgieva at the 2026 Spring Meetings in Washington, DC

Good morning.

A resilient world economy is being tested again by the now-paused war in the Middle East. The conflict has caused considerable hardship around the globe. My heart goes out to all people affected by this war and all wars.

When we welcome ministers and central bank governors to our Spring Meetings next week, our focus will be on how best to weather this latest shock and ease the pain on economies and people.

This requires understanding the nature of the shock, the channels through which it affects the economy, the size of the impact, and the policies that can mitigate it.

So what hit us? A supply shock that is:

Large, with the world’s daily oil flow cut by some 13 percent, and its LNG flow by some 20 percent;

Global, with all of us now paying more for energy and with supply chains disrupted across the world;

And asymmetric, with its impact depending on proximity to the conflict, whether you are an energy exporter or importer, and your policy space.

As always, a negative supply shock pushes prices up. As a point of reference, Brent jumped from $72 per barrel on the eve of hostilities to a peak of $120. Thankfully, oil prices have fallen, but they remain much higher than before the war—and many countries are paying high premiums for access to precious supplies.

Spare a thought for the Pacific Island nations at the end of a long supply chain, wondering if fuel will still reach themin the wake of such a severe disruption.

The supply interruptions have had—and will for some time continue to have—ripple effects, such as:

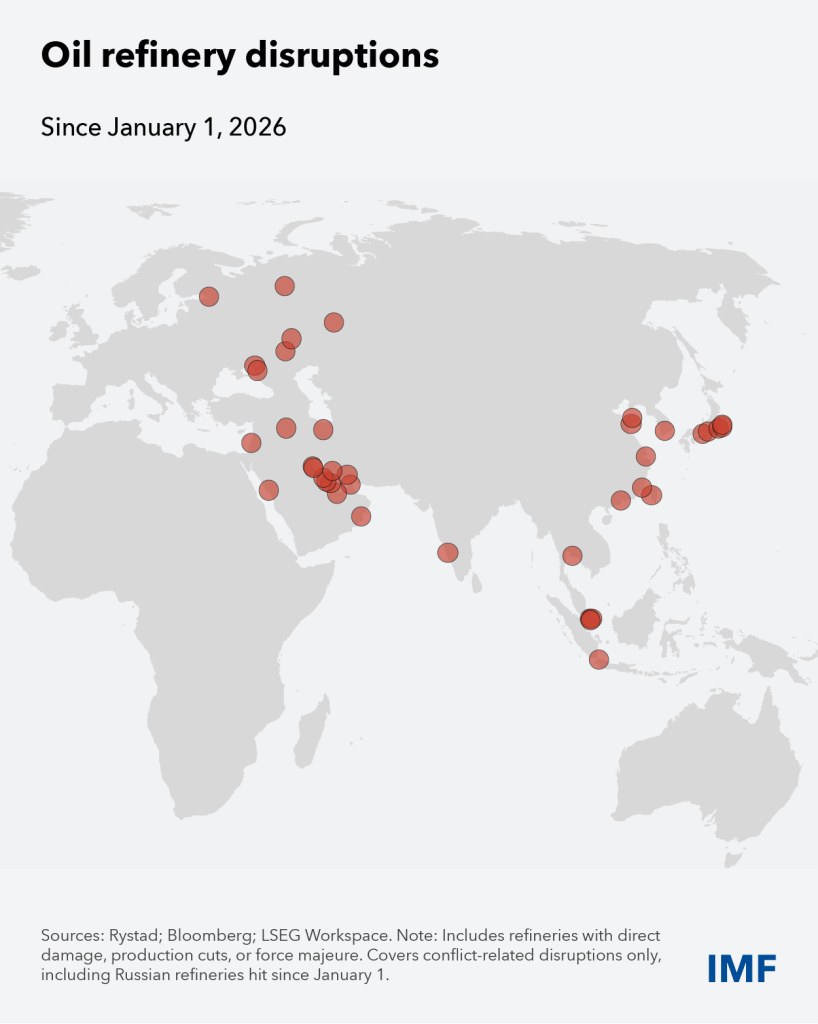

Oil refinery disruptions given the need to maintain minimum flow rates, with warning lights flashing red in many far-flung places;

Shortages of refined products including diesel and jet fuel, which have disrupted transportation, trade, and tourism in a world more interconnected than ever;

Food insecurity for another 45 million people given the transport issues—taking the total number of people in hunger to over 360 million—with the problem potentially worsening over time because of higher fertilizer prices;

And supply chain disruptions given industrial dependencies such as on sulfur, helium for silicon chipmaking and MRI imaging, and naphtha for plastics.

The second question is: how can this shock play out? Through three main channels:

First: the price impact and supply shortages. Higher prices for key inputs feed into many consumer goods, lifting inflation. This, coupled with shortages, reduces demand by brute force.

Second channel: inflation expectations. These can break anchor and ignite a costly inflation process. Here is the distribution of near-term inflation forecasts for the U.S.; notice how the curve has moved to the right, indicating higher short-run inflation expectations. And here is the curve for the euro area; it also moves right, and it widens, indicating higher uncertainty. Fortunately, longer-run expectations have not budged—this is very good and very important.

Third channel: financial conditions. From a highly supportive starting point, these tightened, in an orderly manner. Emerging market bond spreads widened substantially; equity prices adjusted; and the dollar appreciated. And now we see some easing.

We have been here before in the 1970s and earlier this decade. We know eventually a significant part of the shock will dissipate, leaving us in a new equilibrium. Supply recovers and demand adjusts. New capacity comes on stream. Energy efficiency rises.

As proof, please appreciate how the world has become progressively less energy intensive since the 1980s, which cushions the shock. Renewable energy increased its share, yet oil remains our number one fuel.

As the world responds, it is important that we maintain our collective quest for energy efficiency and energy diversification. Different countries have different paths to energy security, but all must strive for it.

Let me move to the third question: how large is the growth impact?

The answer very much depends on whether the ceasefire holds and leads to lasting peace and how much damage the war leaves in its wake.

Given the uncertainties, our World Economic Outlook, to be published next week, will include a range of scenarios, going from a relatively swift normalization, to a middle scenario, to one where oil and gas prices stay much higher for much longer and second-round effects take hold.

All these scenarios start from a situation where strong AI and tech investment, supportive financial conditions, and other factors were driving considerable momentum in the world economy.

In fact, had it not been for this shock, we would have been upgrading global growth.

But now, even our most hopeful scenario involves a growth downgrade. Why? Because of significant infrastructure damage, supply disruptions, losses of confidence, and other scarring effects.

Take Qatar’s Ras Laffan complex—a tremendously important example of strategic investment done right; producer of 93 percent of the Gulf’s LNG, some 80 percent of it going to Asia-Pacific, a region that now endures serious fuel shortages. Ras Laffan has essentially been shut since March 2, took direct hits on March 19, and could take 3‒5 years to restore to full capacity.

Even in the best case, there will be no neat and clean return to the status quo ante.

Another relevant fact: see how ship passages through Bab-el-Mandeb on the Red Sea have never quite recovered from the devastating disruptions there—they remain stuck at about half their 2023 level.

So the reality is, we don’t truly know what the future holds for transits through the Strait of Hormuz or, for that matter, for the recovery of regional air traffic.

What we do know is that growth will be slower—even if the new peace is durable.

And we also know there are significant variations across the world. Countries able toexport oil and gas undisturbed are the least affected. In contrast, countries directly disrupted by the war—including oil and gas exporters who suffered the blockade—and countries relying on imported oil and gas, still bear the brunt of the impact.

How bad this impact will be will depend, in no small measure, on how much policy space countries have, including oil and gas reserves, given the five-week gap we have seen in tanker traffic from the Gulf.

Let me walk you through a few key charts to illustrate three points of differentiation:

First, let’s separate the world into oil importers on the left and oil exporters on the right. As the pile-up of dots on the left shows, over 80 percent of countries are net oil importers.

Second, let’s highlight countries directly hit by this war. Note how the hits have disproportionately fallen on major oil exporters—although the red dots on the left remind us of the war’s toll on regional non-oil economies as well.

Third, let us add a vertical scale for countries’ sovereign credit ratings, as a proxy for policy space. The bottom left is where we find vulnerable oil importers. Let’s color Sub-Saharan Africa in yellow, and small-island nations in orange. Notice how these two sets of countries largely fill that quadrant of vulnerability—they will very much be in our focus next week.

And yet, with oil being a global commodity, even oil exporters far from the affected region and enjoying terms-of-trade gains have felt the effects of costlier oil.

Let me move to the last question: what should countries do?

A word of caution upfront: this being a classic negative supply shock, demand adjustment is unavoidable.

Policymakers can help in multiple ways, and—certainly—they must be careful not to make things worse. So here I appeal to all countries to reject go-it-alone actions—export controls, price controls, and so on—that can further upset global conditions: don’t pour gasoline on the fire.

Beyond that, as in past shocks, alertness and agility are key. The challenge will be to detect if and when changing conditions take us from one state of the world to another:

For now, there is value inwaiting and watching, with central banks stressing their commitment to price stability but otherwise staying on hold—with a stronger bias to action if credibility is in question. Fiscal authorities should provide targeted and temporary support to the vulnerable, aligned with their medium-term fiscal frameworks.

Next, if inflation expectations threaten to break anchor and ignite a costly inflation spiral, then central banks shouldstep in firmly with rate hikes. Fiscal support should remain targeted and temporary. Rate hikes, of course, would further dampen growth—that’s how they work.

Finally, if a severe tightening of financial conditions adds a negative demand shock to the supply shock, then monetary policy returns to a delicate balancing act while fiscal policy—if and only if there is fiscal space—switches to well-calibrated demand support.

Let us have a quick look at what hasactually been happening out there.

In monetary policy, markets have been expecting major central banks to tighten their policy stance. Here we see four key market-implied policy rate paths, each showing an upward shift.

In energy policy, we see many countries putting in place emergency conservation measures—from general campaigns, to limits on private vehicle use, to remote work. These and other steps are well-documented in the International Energy Agency’s energy policy tracker, which is summarized here.

Such information-sharing, let me add, underscores why we have joined forces with the IEA and the World Bank to form a coordination group within which the IMF will lead on the macroeconomics.

And finally, coming back to fiscal policy, we see that most countries have appropriately held the line, avoiding untargeted tax cuts, energy subsidies, and price-based measures, although a few have chosen to deliver broad-based support. Again we see the IEA summary here.

We will point out that measures that mute the price signal also mute the necessary demand response, resulting in higher global energy prices. And we will work with countries to help them target their fiscal support and craft effective sunset clauses for temporary measures.

As we do so, we will also stress that it is important for fiscal and monetary policies to not pull in opposite directions.

Already, the world has seen benchmark yield curves rising, driving up the cost of debt. Adding deficit-financed stimulus to this mix at this moment would increase the burden on monetary policy and amplify such shifts. It would be like driving with one foot on the accelerator and one on the brake—not good.

As we will flag in our forthcoming Fiscal Monitor, the world has a fiscal space problem. Public debt is generally much higher than 20 years ago—including in most G20 countries—reflecting widespread neglect of fiscal consolidation in the periods when conditions permitted it.

As a result, interest payments are rising as a share of revenue at all income levels. The implication is clear: all countries must deploy their limited fiscal resources responsibly, and most must move decisively to rebuild fiscal space after this shock. I cannot emphasize this enough.

Let me move to financial sector policies. As our Global Financial Stability Report will insist, it is essential that financial regulators and supervisors be alert, nimble, and responsive to a fluid situation.

Financial conditions have been highly accommodative for some time, spurred by tech optimism and new financial intermediaries, many of them nonbanks. While this has lifted growth, it also creates risks of reversal. If investors were to start worrying about energy insecurity holding back the growth of AI, for example, given AI’s huge energy needs, then we could find ourselves in a spot of trouble.

Micro- and macro-prudential policies must work to reduce financial stability risks and ensure a resilient system.

With that, I want to stress the most important lesson of all: good policies make a difference. There are forces countries can’t control, but they do have authority over their own policies and institutions.

Take heed: the strength and agility of your fundamentals is your best defense when shocks come—and come they will.

And, as you deal with the long tail of the current shock, do not forget to steer the great global transformations in technology, demographics, geopolitics, trade, and climate and build a better future. Your structural and regulatory policy choices underpin productivity and long-run growth—and growth potential matters enormously for stability.

For us at the IMF, supporting you to build strong policies and institutions, this is our raison d’être. And, as the firefighter, we are here for you when crisis hits.

Once more, let’s take into our lens the vulnerable oil importers of the world, those rated in the speculative grade, and let’s color in blue all countries with IMF-supported programs. We can scale these programs up if needed and—be sure—there are more programs to come.

Given the spillovers of the Middle East war, we expect near-term demand for IMF balance-of-payments support to rise by somewhere between $20 billion and $50 billion, with the lower bound prevailing if the ceasefire holds.

Two points worth noting here. One, this range would be much higher were it not for the sound policymaking of many emerging market economies—including some of the largest ones—over the decades. And two, we are well resourced to meet this shock.

So, yes, our 191 member countries can count on us to support them with financing if needed. And they can count on us to bring them together to find a path forward through the fog of uncertainty. This is what next week will be about.

Thank you, and let us hope for lasting peace in the Middle East and everywhere—because war takes away everything that we work for.

Compliments of the International Monetary FundThe post IMF | Cushioning the Middle East War Shock first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.