Fighting Inflation with Rate Hikes and Balance Sheet Reduction | Governor Christopher J. Waller | At the Economic Forecast Project, University of California, Santa Barbara, Santa Barbara, California |

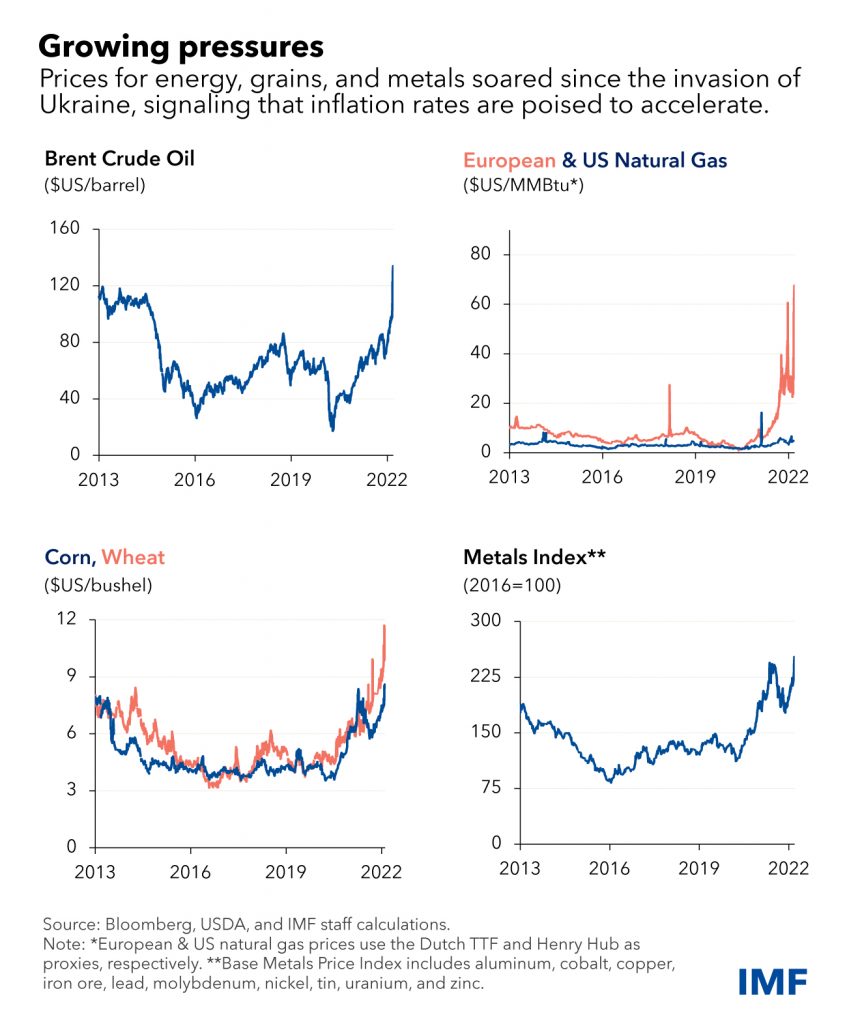

Thank you Peter, and thank you to the UCSB Economic Forecast Project for the invitation to speak today. My plan is to start with my outlook for the U.S. economy in 2022, and then describe what I consider the appropriate path of monetary policy to keep the economy on a healthy and sustainable course.1 But, before I get into that discussion, let me comment on what I think is on everyone’s minds today, Russia’s attack on Ukraine. Obviously, there are people in harm’s way and we shouldn’t lose sight of them. It is far too early to judge how this conflict will affect the world, or the world economy, and what the implications will be for the U.S. economy. But this situation adds uncertainty to my outlook and will be something I will be monitoring very closely. As my speech will say, we will need to carefully look at the incoming data, especially during a time of heightened uncertainty.

Turning to my outlook for the economy, my greatest concern is continued elevated inflation. Inflation is too high, and I think concerted action is needed to rein it in. The Federal Open Market Committee (FOMC) has multiple tools to tighten monetary policy, and I will go into some detail about how I believe the Fed should approach increasing the target range for the federal funds rate and reducing the size of the balance sheet.

But let me start with the outlook for economic activity. I expect the economy to continue expanding at a healthy rate this year, slower than in 2021 but still at a solid pace that will keep employment growing strongly. While there are some signs that the effects of the Omicron variant have dampened economic growth in the last month or two, it does not appear to have affected hiring, given the healthy jobs report for January. Even COVID-sensitive sectors such as leisure and hospitality saw big job gains last month. With COVID cases dropping sharply, I expect this latest surge in infections will not be a major factor affecting the economy in 2022. Supply bottlenecks and labor shortages, some of them related to the pandemic, continue to weigh on economic output, but I expect those to diminish later this year.

The combination of strong consumer demand and supply constraints has produced very high inflation. The consumer price index (CPI) was up 7.5 percent for the 12 months through January, the highest yearly rate in 40 years. With appropriate monetary policy, and the expected easing in supply constraints, I am hopeful inflation will move down over the course of this year, even with the recent geopolitical developments. Nevertheless, the path of inflation is the biggest risk to my outlook.

As we move through this year, I can’t emphasize enough how much this outlook, and the appropriate stance of monetary policy, will be influenced by the data that we see about the performance of the economy. I know, I know. Saying you need to be data dependent is like saying you are for motherhood and apple pie—who would disagree? But in the current situation, it is urgently important to be data dependent. For example, like most people, I expected the Omicron surge would hammer job creation in January, but the data showed that this didn’t happen. The ups and downs in forecasts during the pandemic should be evidence enough that policy decisions this year, more than ever, will need to be guided by the data, and not by what past experience suggests should happen.2 Missouri, which is home for me, is the Show Me State, so if you want to know how my outlook will evolve, show me the data. With that in hand, I will evaluate the outlook with respect to the Fed’s dual mandate in determining the appropriate setting for monetary policy.

The Labor Market

Let’s start with where the economy stands with respect to maximum employment. In December, I said that we were “closing in” on this objective.3 Since then, the labor market has continued to strengthen. I now believe we have achieved the FOMC’s objective of maximum employment. So, what has changed and made me more certain about that?

A big factor was the jobs report for January, which included very strong data for that month, upward revisions for November and December, and revisions for all of 2021. What we learned from those changes was that a reported slowdown in job creation in the second half of the year never happened, and that in fact job creation was remarkably steady throughout the year, averaging 555,000 a month and never deviating very far from that trend. These revisions helped explain why we saw such large and steady declines over the year in the unemployment rate, which fell from 6.4 percent in January 2021 to 4 percent in January 2022, which happens to be the median of FOMC participants’ December estimates of the longer-run unemployment rate. Accounting for retirees leaving the workforce, I estimate that employment is close to the levels of February 2020, right before the pandemic shock hit the economy and when the target range for the federal funds rate was much higher than the current target range.

The January job numbers were just one monthly report, but one reason I have the confidence to declare that maximum employment has been reached is the message January sent about the durability of the continuing recovery. Based on recent data, including a big increase in retail sales in January, it sure looks like a very significant surge in COVID has failed to derail or even appreciably slow the economy. It has been hazardous to predict much about the economic effects of the pandemic more than a month or two out, but I’m comfortable saying we are at maximum employment in part because of the evidence that the labor market is continuing to strengthen.

Another message from the January report, including the revisions to each month of 2021, is that, so far at least, labor shortages do not seem to be having a huge effect on the economy’s capacity to create jobs. Job creation didn’t slow appreciably in November and December as originally reported; it actually was higher than the average for the rest of the year. Labor force participation isn’t growing as much as one would expect with the hot job market, but apparently it’s growing enough to keep the job creation machine humming.

Another factor that signals we are at maximum employment is the continued rise in measures of labor compensation. The broadest measure of labor compensation, covering wages and benefits, is the employment cost index, which for private sector workers rose at a 4.7 percent annual rate in October, November and December, the fastest pace in 20 years. Average hourly earnings also continue to grow more strongly than they have in decades, and the gains are widespread across sectors. Job vacancies also indicate labor demand is exceptionally strong with nearly 3 million more vacancies than individuals looking for work.

Inflation

While I will continue to watch data on the labor market, I am focusing most of my attention on inflation, which is far too high and needs to come down. In December, some people were a little surprised to hear me say that inflation was “alarmingly high,” but after the latest inflation numbers, I think we all should be alarmed. It is alarming because high inflation is especially painful for lower- and middle-income people, who don’t have a choice about paying more for gasoline, groceries, shelter, and other necessities. It is alarming because of the risk that high inflation could become ingrained in people’s expectations and prove difficult to rein in, undermining economic growth.

The 7.5 percent increase in the CPI in January came after a 7.1 percent increase in December. It was the 11th consecutive month that inflation exceeded 2 percent. The FOMC targets another measure of inflation, the price deflator for personal consumption expenditures (PCE), which will be reported tomorrow. But for both measures, inflation has been increasingly broad-based for quite some time. For the CPI, better than 70 percent of items measured are up 3 percent or more in the last 12 months, and for PCE inflation, 60 percent of items were up that much in December.

High inflation is a significant problem for individuals and families, and it makes it difficult for businesses to control costs and adjust prices. There is also the risk that the public’s expectations of future inflation rise significantly, which affects spending decisions in the short term and thus can have the effect of driving inflation even higher. Keeping longer-term inflation expectations anchored is vitally important for monetary policy. In fact, the FOMC’s Statement on Longer-Run Goals and Monetary Policy Strategy emphasizes that longer-term inflation expectations that are well anchored at 2 percent foster price stability and enhance the Committee’s ability to promote maximum employment in the face of significant economic disturbances.

Surveys of consumers’ expected inflation over the next year moved up quite notably through 2021 and are currently elevated. And the public’s expectations of inflation over the next five years have risen as well. That said, five-year inflation expectations are where they were over the past couple of decades when inflation stayed low. Importantly, longer-term expectations are much more stable. For example, future inflation measured by investors trading inflation-adjusted securities has 5-to10-year implied compensation around 2.2 percent, which, adjusted for the FOMC’s preferred measure, PCE, is close to 2 percent. In the same way that expectations of much higher inflation can drive a cycle of ever-increasing inflation, when expectations are “anchored” and don’t move significantly, it can have the effect of helping moderate surges in inflation, such as the one we have seen over the past year.

As for what inflation does next, I think anyone who makes a forecast has to own the fact that very few of us foresaw how much inflation would increase in 2021. We underestimated the extent to which supply constraints—from bottlenecks to labor supply shortages—and strong demand would drive up inflation, and we thought bottlenecks and shortages would begin to resolve sooner than now. I think we have a clearer idea today of the effect of those factors on inflation but going forward we need see how geopolitical effects influence energy, commodity, and other prices. With some humility, while I am alarmed about the level of inflation and a bit uncertain about how the near-term may play out, I am hopeful that these factors and their price effects are likely to ease in the second half of 2022 and that with appropriate monetary policy, inflation will be coming down significantly by year end.

I will be watching closely the data on supply pressures and how those feed into total consumer prices, and I’ll be monitoring carefully to see whether expectations rise out of a range that would suggest they are becoming unanchored. As I said earlier, it is too soon to know how Russia’s attack on Ukraine will affect the U.S. economy, and it may not be much easier by the time of our March meeting.

Appropriate Monetary Policy

Now let me spell out what my outlook implies for appropriate monetary policy over the course of 2022. Based on the inflation data in hand, I believe the Fed needs to act promptly to begin tightening monetary policy. As I said earlier, I believe that we have achieved our employment goal and that the labor market will keep improving, which means there should be no delay in responding to inflation that is significantly above our target.

The FOMC has already taken actions to end asset purchases in early March, and I believe that the recent inflation and jobs reports have made the case to begin raising the target range for the federal funds rate at our March FOMC meeting.

Based on my outlook, my preference is to increase the target range 100 basis points by the middle of this year. That is, I expect inflation to remain elevated and only show modest signs of deceleration over the next several months. As a result, I believe appropriate interest rate policy brings the target range up to 1 to 1.25 percent early in the summer. That would be a bit below where rates were at the outbreak of the pandemic, when inflation was considerably lower, and before we more than doubled the Fed’s balance sheet, so I consider this a necessary and prudent start to tightening policy.

The pace of tightening will depend on the data. One possibility is that the target range is raised 25 basis points at each of our next four meetings. But if, for example, tomorrow’s PCE inflation report for January, and jobs and CPI reports for February indicate that the economy is still running exceedingly hot, a strong case can be made for a 50-basis-point hike in March. In this state of the world, front-loading a 50-point hike would help convey the Committee’s determination to address high inflation, about which there should be no question. Of course, it is possible that the state of the world will be different in the wake of the Ukraine attack, and that may mean that a more modest tightening is appropriate, but that remains to be seen. With the economy at full employment and inflation far above target, we should signal that we are moving back to neutral at a fast pace based on the performance of the economy, and a 50-basis point hike would help do that. Consequently, should the data break against us in the coming weeks, we need to be prepared to hike the policy rate by 50-basis points.

No matter the near-term path of reducing accommodation, the FOMC must respond decisively to the data so as to maintain our credibility that we will bring down inflation. We constantly say we have the tools to fight inflation, and now we must demonstrate the will to use them.

While I believe that we should raise the target range by 1 percentage point over the next several months, I will be assessing the incoming data to decide whether further rate increases in 2022 are warranted and, if so, at what pace they should be implemented. If high inflation persists, then I would most likely support that we continue hiking, and potentially increase the pace of tightening. If inflation moderates in the second half of the year, as I expect, and as market participants expect, then we can slow the pace of tightening or even pause. As I said earlier—show me the data.

Turning to balance sheet policy, as I noted, the Committee has decided to end asset purchases in early March. Initially, we will be keeping the size of the Fed’s balance sheet constant by reinvesting the proceeds of maturing securities. The FOMC has not decided when to begin the reduction in the size of the balance sheet, but we issued a set of principles last month that make it clear that changing the target range of the federal funds rate is our principal monetary policy tool, and that balance sheet reductions through the “runoff” from maturing securities would commence after rate hikes have begun.

I support starting this process no later than the July FOMC meeting. The pace of the reduction in asset holdings has not been determined but will be consistent with promoting the FOMC’s employment and inflation goals and will be communicated well in advance to the public so that the plan is predictable.

The last time we reduced our balance sheet we did the following: First, we waited two years after our first-rate hike before commencing balance sheet runoff. Second, we imposed monthly caps on the amount of maturing securities that we would let run off. These caps started out very low and were gradually lifted over a period of 12 months. So, why not follow the same strategy this time?

First, back in 2017 and 2018 we had never intentionally reduced our balance sheet before. This was new territory for the Fed, so we went slow. Second, the Committee was considering moving to an ample reserves regime for conducting monetary policy, where we wanted to keep the banking system flush with reserves. Thus, we had no idea how far we could let reserves fall before we might cause an unwelcome shortage of reserves. Third, the economy was in a much different place; in particular inflation was much lower. Finally, we only expected to run off about $2 trillion of securities from our balance sheet. In that environment it made sense to go slow and gradual in terms of balance sheet reduction.

Fast forward to today. This is now the second time we have done balance sheet reduction and we learned from experience and can go faster than before. Policymakers and markets have a good understanding now of how the process works.

In terms of the appropriate size of the caps, I believe they can be larger than last time for several reasons. First, we have a very large balance sheet—securities holdings have increased $4.5 trillion since the start of the pandemic and the balance sheet is nearly $9 trillion. So even with a hefty reduction in holdings over the next year, we will still have a balance sheet that will be more than sufficiently large enough to conduct monetary policy. Second, the Fed’s overnight reverse repurchase agreement facility, put in place to help conduct monetary policy, receives a large amount of deposits each day. The daily average take-up of $1.6 trillion so far in 2022 tells me that there is tremendous excess liquidity in financial markets. Large redemption caps will assist in removing this excess liquidity. Third, we have learned a lot about operating in an ample reserves regime over the past decade. And we learned lessons from the 2019 experience in reducing reserves. In the first quarter of 2019 the ratio of reserves to nominal gross domestic product (GDP) was approximately 8 percent and financial markets worked well and banks were flush with liquidity. Right now, reserves are far more than ample, standing at 17 percent of GDP. When evidence suggests that we are getting closer to a more appropriate and sustainable level of reserves, we can slow the pace of redemptions. Finally, we have the newly established standing repurchase facility, which acts as a backstop to buffer any unexpected liquidity needs. This facility can help assist us with any unexpected bumps along the way.

With large caps and sizable amounts of securities maturing over the course of the next year or two, I do not see the need to consider asset sales anytime soon. However, because the Fed’s mortgage-backed securities (MBS) holdings have long maturities and are quite sizable, prepayments are unlikely to bring these holdings down to de minimis levels over the next decade. So, MBS sales could be something the Committee considers down the road to satisfy our balance sheet principles long run goal of holding primarily Treasury securities. But that is a conversation for another day. In the meantime, I would support having no caps on MBS redemptions so our MBS holdings decline as fast as prepayments allow, which would modestly assist in moving us toward an all-Treasury portfolio.

Thinking about possible monetary policy actions in 2022, I expect it will be a very fluid year. The Chair has said we will be nimble. I believe nimble describes how we acted in 2021 as well, when nimbleness and good communications served the FOMC well. Think back to the middle of 2021. Just last June, markets expected tapering to begin sometime in 2022, the majority of FOMC participants called for liftoff in 2023, and primary dealers surveyed in July by the Federal Reserve Bank of New York predicted a decline in the balance sheet wouldn’t start until the middle of 2025. Wow, how things have changed.

Over the course of the second half of last year, market expectations of the taper’s beginning quickly moved to November, and then a month after it started, markets predicted it would be completed this March. Soon after, markets were pricing liftoff in March, with several rate hikes over the course of 2022. And now markets are also focused on the start of the decline in the balance sheet sometime this year. It is interesting to note that these dramatic changes in actual and anticipated monetary policy have occurred without volatility or strain in financial markets. I believe the FOMC has been highly effective in communicating its shifting outlook for the economy and appropriate policy actions as the data revealed that inflation was increasing much more than forecasters expected.

Another point to make about the big changes in actual and anticipated monetary policy is that they are showing up in the financial data today. Financial conditions are tighter, I believe, because of the credible, forward guidance policymakers have communicated to the public. Although the Fed hasn’t started raising rates or reducing the balance sheet, interest rates have moved up notably. For example, the 2-year Treasury yield is more than 1 percentage point higher today than at the start of the third quarter of last year. The 10-year Treasury yield is up 1/2 percentage point, and the 30-year fixed mortgage rate is up about 1 percentage point over this period. Going forward, policymakers will adjust policy as needed, which will reinforce the Fed’s credibility.

Let me conclude by saying I hope my remarks today contribute to the Fed’s effective and credible communications. One message you should take away is that the course of policy is not pre-set, and the course I favor will be determined by my interpretation of new data. In the past couple months, inflation and employment data have been sending the same, unequivocal message—it is time to start tightening monetary policy. We need to take the first step in March to get off the effective lower bound. Then we should continue with hikes as well as begin to reduce our balance sheet. I will continue to monitor the geopolitical situation to assess the appropriate timing of this near-term monetary policy tightening. These actions will get us into the second half of the year, when we will have six months of inflation data, and we can assess what the appropriate path will be for the rest of 2022. Our goal is a soft landing for the economy that keeps output and employment growing at a healthy pace and inflation moving toward the FOMC’s 2 percent objective.

Compliments of the U.S. Federal Reserve.

1. These views are my own and do not represent any position of the Board of Governors or other Federal Reserve policymakers. Return to text

2. In December, I discussed lessons from the pandemic for economic forecasters, which included a review of forecasting misses for output and inflation. See Christopher J. Waller (2021), “A Hopeless and Imperative Endeavor: Lessons from the Pandemic for Economic Forecasters,” speech delivered at the Forecasters Club of New York, New York, December 17. Return to text

3. See Waller, “A Hopeless and Imperative Endeavor,” in note 2. Return to text

The post U.S. FED | Remarks by Governor Waller on fighting inflation with rate hikes and balance sheet reduction first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.