Letter from the United States Department of Commerce

U.S. Under Secretary of State

21

Dec

Letter from the United States Department of Commerce

U.S. Under Secretary of StateAmidst the general uncertainty in the world, one thing you can rely on is our December predictions for the year ahead. This year, we look at tech trends and developments and their impact on the law, with a focus on Web3 and the metaverse. We also predict the key issues and developments in data and life sciences, and consider whether 2023 will really see the end of the influence of EU law in the UK.

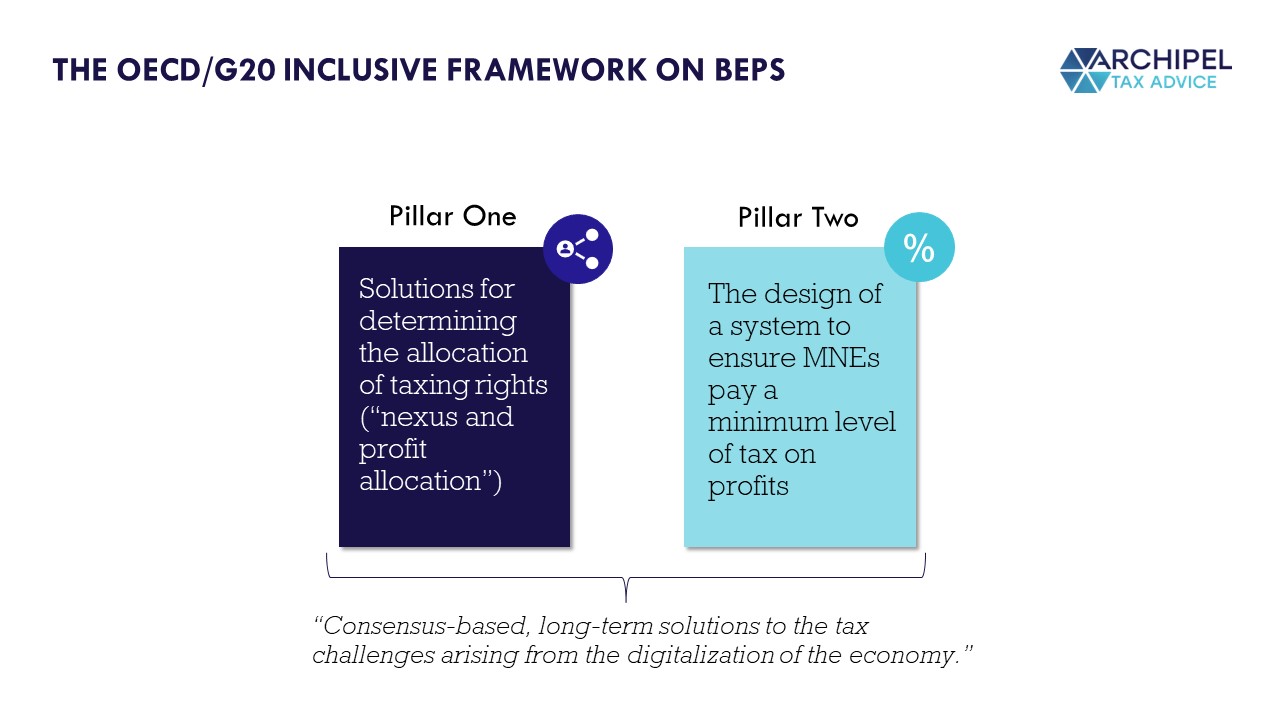

You may have heard about Pillar Two, and you may have also heard that the Netherlands, as the first country in the EU, published Pillar Two draft legislation on October 24th, 2022. This draft will now be updated following a round of public consultation, after which the amended draft legislation will be presented to the Dutch Parliament, with the aim to get it implemented and effective by the start of 2024. Now you may be wondering what this is all about, if and when this is actually going to happen, and whether you should care – below we summarize, visualize & cover some FAQs on Pillar Two general systematics and the Dutch draft rules.

Pillar Two is part of a two-pillar solution resulting from the OECD’s BEPS Action 1 (set back in 2015), calling to address the tax challenges arising from the digitalization of the economy. Per October 2021, over 135 jurisdictions have signed on to the statement on the Two-Pillar Solution to Address the Tax Challenges Arising from the Digitalisation of the Economy, to reform the international tax system in light of this ongoing increasing digitalization.

In short, Pillar One aims to realign taxing rights towards ‘market jurisdictions’ where MNEs lack a physical presence, and Pillar Two aims to ensure that a minimum level of tax is paid, addressing the challenges of the digitalizing economy where the relative importance of intangible assets as profit drivers may still leave room for profit shifting planning.

To put it in a nutshell (with reference to the following questions for further details):

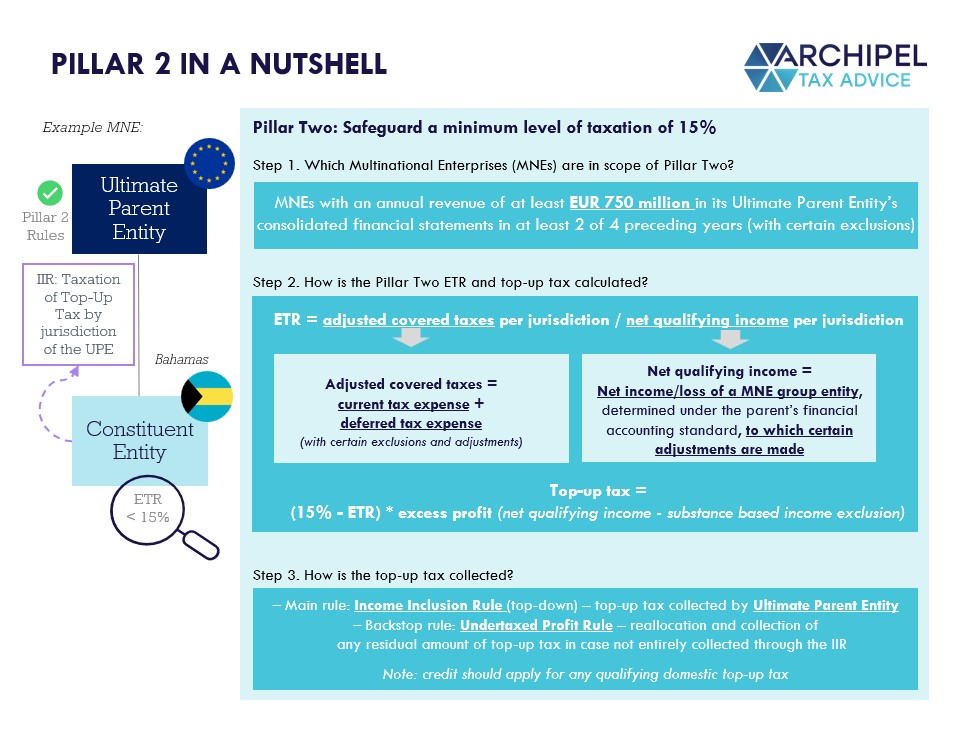

Pillar Two is designed to ensure that MNEs pay a minimal level of tax in every jurisdiction in which they have a taxable presence, therewith also lowering the incentive for MNEs to ‘shift’ profits to lower tax jurisdictions, for example through moving IP or other tangible assets to those jurisdictions. The minimum level of tax is set at a rate of 15% over a ‘common’ tax base determined based on the Pillar Two rules.

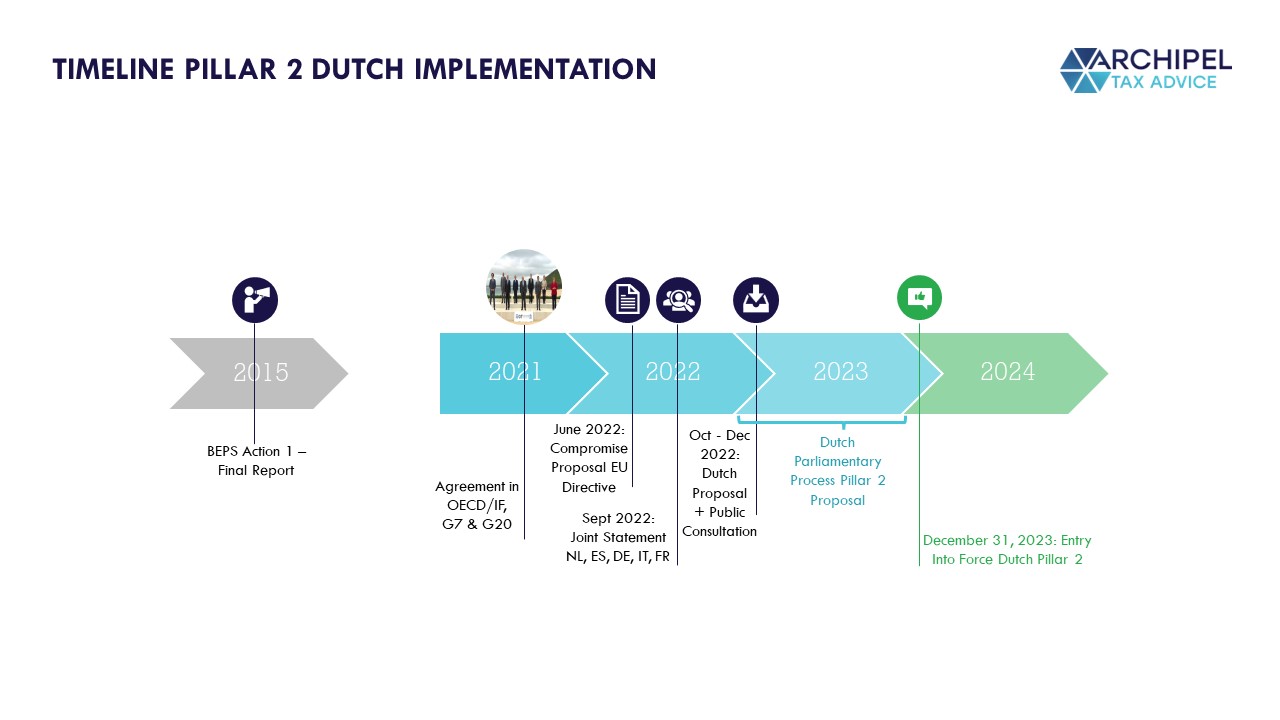

While originally presented as a combined ‘two-pillar solution’, the implementation of each Pillar is now following a different track and it seems likely, at least in a number of jurisdictions, that implementation will take place separately. In December last year (2021), the OECD/IF released its first draft of the Pillar Two ‘Model Rules’, closely followed by the European Commission releasing its (largely similar) draft Pillar Two Directive. These drafts, once finalized, are meant to serve as a template for the implementation into domestic law.

Although Pillar Two was initially back on the agenda for the last Ecofin meeting on December 6th, 2022, the draft EU Directive has still not been adopted, as the required unilateral agreement by all EU Member States has not yet been reached. Recently, however (September 2022), a joint statement was issued by the governments of France, Germany, Italy, the Netherlands, and Spain, reconfirming their commitment to the implementation of the global minimum tax (essentially Pillar Two). Following that statement, as mentioned, the Netherlands is now the first of these five to have published its draft Pillar Two legislation, with intended implementation for financial years starting on or after 12/31/2023.

The Pillar Two rules apply to entities that are part of an MNE Group with an annual revenue of at least EUR 750 Million based on an Accepted Financial Accounting Standard (similar to the threshold for the existing Country-by-Country Reporting or ‘CbCR’ rules). To be in scope, the Ultimate Parent Entity (‘UPE’) of the MNE Group must meet the revenue threshold on a consolidated basis for at least two of the four years immediately preceding the relevant fiscal year. The UPE is described as an entity that has a Controlling Interest -directly or indirectly- in any other Entity (and is itself not owned -directly or indirectly- by another entity with a Controlling Interest in it). A Controlling Interest is a recurring term in the Pillar Two rules and is defined as an Ownership Interest in an Entity for which the interest holder is -or would have been- required to consolidate the assets, liabilities, income, expenses, and cashflows of the Entity. In addition, a Main Entity is deemed to have the Controlling Interest in its Permanent Establishments, based on which the Model Rules also apply to companies with Permanent Establishments in one or more jurisdictions. Certain entities, such as NGOs, Investment Funds, and Pension Funds, are excluded from the Pillar Two rules.

The ETR of an MNE under Pillar Two rules is determined by dividing the amount of ‘Covered Taxes’ by the amount of income as determined under the Pillar Two rules. In short, Covered Taxes include any tax on an entity’s income or profits (including a tax on distributed profits) and include any taxes imposed instead of a generally applicable income tax. Covered taxes also include taxes on retained earnings and corporate equity. The MNE’s income is calculated starting with the standalone financials of group entities (or permanent establishments) determined under the same accounting standards as the consolidated financial statements at UPE level, i.e. the Financial Accounting Net Income before consolidation to eliminate intra-group transactions. Subsequently, certain adjustments (some mandatory, some elective) are to be made in order to align the determination of the income base better with common (tax) standards.

Once the Covered Taxes, as well as the (adjusted) income (or loss), has been determined under the Pillar Two rules, these amounts are grouped for all in-scope entities (or permanent establishments) within the same jurisdiction (with certain consolidation eliminations for income/loss of entities in tax groups in the same jurisdiction) to eventually determine the Pillar Two ETR for that jurisdiction. Note that when calculating the ETR, the taxable income for a jurisdiction may be lowered with a substance-based carve-out (a percentage of payroll costs and tangible asset value) to allow for a fixed return for ‘real economic activity’ to be out of scope.

Finally, the amount of Top-Up Tax for each group entity is equal to the difference between the ETR and the minimum ETR under the Pillar Two rules, multiplied by the adjusted income of the group entity.

Although these can be a good starting point, the ETR for purposes of the Pillar Two rules may be different in some cases as it is calculated based on a new set of rules determining which income (or loss) and which taxes should be taken into account as described above.

To get into the details a bit – the rules based on which we determine what goes into the ETR calculation in terms of taxes and income for Pillar Two purposes are different from the rules used for the existing ETR calculations. And although there are quite some similarities, there can also be some differences that could lead to a different ETR for Pillar Two, for example:

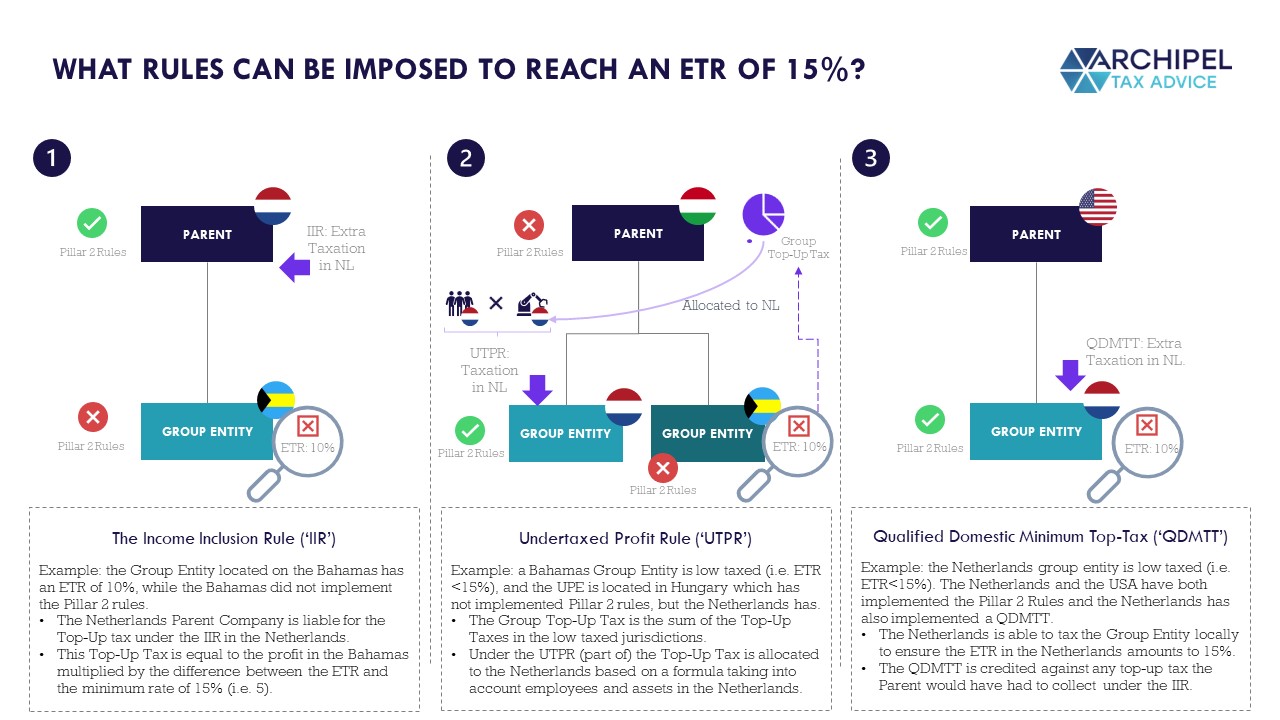

The key systematics of Pillar Two have been designed to include a main ‘top-down’ rule, the Income Inclusion Rule (‘IIR’), and a backstop rule, the Undertaxed Profit Rule (‘UTPR’). The IIR imposes a Top-Up Tax on the UPE with respect to low-taxed income (below 15%) of a foreign subsidiary or permanent establishment (comparable to a sort of CFC rule). The UTPR acts as a backstop rule to collect any top-up tax that is not collected under the IIR, and is effectuated through the denial of deductions (or other profit adjustments) applied by the (lower-tier) group entities in other jurisdictions that have implemented the UTPR (divided based on the number of employees and tangible asset value in the UTPR jurisdictions).

Next to the IIR and UTPR, the OECD and EU Pillar Two draft rules however also leave room for so-called Qualified Domestic Minimum Top-up Taxes (‘QDMTT’) which, if imposed, lower the top-up tax to be collected under the IIR and UTPR. As this QDMTT allows jurisdictions to collect the additional tax determined under Pillar Two rules themselves instead of potentially having other jurisdictions do so under the IIR or UTPR, it is expected that a lot of jurisdictions will introduce such a domestic tax, meaning that the collection of the top-up tax will, in that case, happen in the jurisdiction where the Pillar Two ETR is below 15%. Refer to the below visual for some simplified examples of how the IIR, UTPR and QDMTT could apply.

Looking at these systematics, it is rather crucial that the rules are implemented consistently across jurisdictions, producing the same overall result to ensure that the MNE Group is subject to a minimum level of taxation in each jurisdiction without exposing it to the risk of double taxation. Although the OECD and EU drafts aim to facilitate such consistency, local implementations may still differ in terms of exact rules or interpretation/application thereof.

Following the publication of the draft rules and the closing of the public consultation round, the draft proposal will now be updated and then presented to the Dutch Parliament, where the legislation will be discussed in both Houses. The rules are then intended to be finalized and implemented during the course of 2023 to start applying for financial years starting on or after December 31, 2023 (and December 31, 2024 for the UTPR).

The Dutch draft legislation is meant to implement the proposed EU Pillar Two Directive (specifically the compromise text of June 16, 2022). Even though agreement at EU level has not yet been reached, the Dutch government still favors a common EU approach. The joint statement brought out together with France, Germany, Italy and Spain in September this year reconfirms the wish to reach agreement at EU level and therewith the commitment of the Netherlands to implement the Directive timely. The Dutch government indicated the draft legislation can form the basis for definitive proposed legislation, whereby EU developments are monitored closely.

To implement the rules in its domestic legislation, the Netherlands has chosen to create a separate tax act in addition to its current Corporate Income Tax Act (‘CITA’). The reason for having a new and separate act is primarily to avoid adding complexity to the current CITA.

The Dutch draft legislation includes the optional QDMTT. The QDMTT aims to ensure that the Netherlands will be able to collect the Top-Up Tax of Dutch-based low-taxed entities (or permanent establishments) locally in the scenario the parent entity is not located in the Netherlands. If the Dutch domestic rules qualify as a QDMTT, a UPE located in another jurisdiction is, in principle, obliged to give a credit for the top-up tax collected under the Dutch QDMTT (we refer to the explanation above).

An MNE group is a group of entities that are connected by ownership or control. The Pillar Two rules are linked to the group concept in the accounting standard rules as applied at UPE level when drawing up the consolidated annual accounts. The second form of an MNE group could be an entity with one or more permanent establishments – provided that the entity is not already part of an MNE group.

In that case, the company can still qualify as a large-scale domestic group, which is in principle also in-scope of the Pillar Two rules.

The Dutch draft legislation identifies three types of group entities:

A permanent establishment is treated as a separate group entity for purposes of the Dutch Pillar Two rules. This ensures that the income derived by the permanent establishment is not included in the calculation of the ETR in the jurisdiction of its Parent.

An ‘entity’ is treated as such if it has legal personality and/or if it prepares financial statements, which is also the case for partnerships or trusts. It is, therefore, not necessarily required to have legal personality. Individuals do not fall under the definition of ‘entity’.

The rules deviate from the existing rules of the Dutch participation exemption in the CITA. Where the Dutch participation exemption generally excludes dividends and capital gains derived from qualifying subsidiaries in which ownership interests of 5% or more are held without a minimum holding period, the draft Dutch Pillar Two rules only allow for the exclusion of dividends and other income derived from a subsidiary if the ownership interest in that subsidiary is 10% or more and/or if the subsidiary has been held for at least a year. Based thereon, the taxable income under the Dutch CITA could look different from the income under the Dutch Pillar Two rules.

Another example of where the rules deviate is in relation to liquidation losses, which can under circumstances be taken into account when determining the taxable income under the Dutch CITA, while such losses are not taken into account under the Dutch Pillar Two rules.

The innovation box effectively lowers the CIT rate from 25.8% to 9% for income derived from qualifying innovative activities. As a result, companies applying the innovation box may have a lower ETR in comparison to other companies. Although the Pillar Two rules will not impact the application of the Dutch innovation box as such, the effectiveness may be impacted by the Pillar Two rules if these would result in additional taxation up to the 15% minimum tax level. It is, however, expected that in most cases, the application of the Innovation Box will not result in an overall ETR of less than 15% (on a blended basis, seeing as the Dutch headline rate is 25.8% and generally only part of the revenue of a company is attributable to the innovation box). Therefore, it is not expected that this will impact many Dutch-based companies according to the explanatory statements to the Dutch draft Pillar Two legislation.

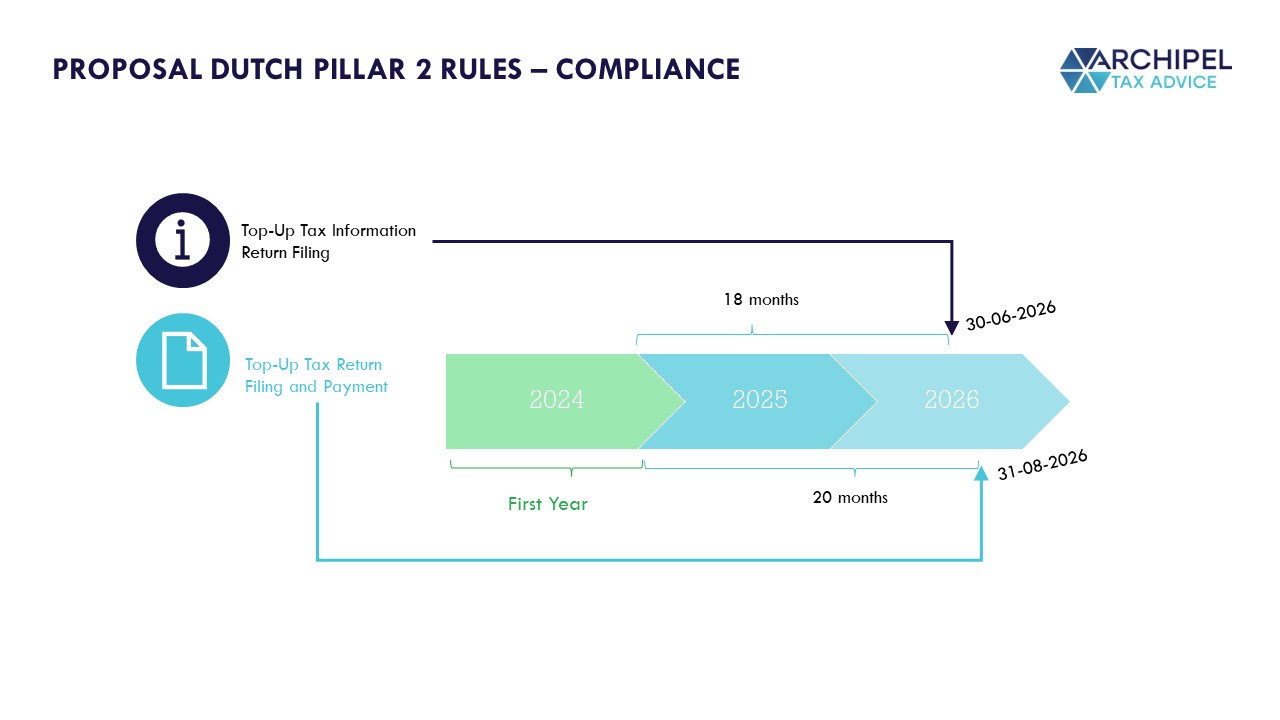

It is proposed that the in-scope Dutch-based UPE or group entity of an MNE should file a Pillar Two specific top-up tax information return separate from the actual top-up tax return. This top-up tax information return should contain the calculation of the top-up tax and the distribution thereof across the jurisdictions. Following the initial year in which the Pillar Two rules take effect in the Netherlands (likely 2024), a Netherlands-based UPE or MNE group entity has 18 months to file the top-up tax information return. Two months later, the consequent Pillar Two top-up tax return and payment term end, i.e. 20 months following the end of the initial year. In the second year (likely 2025), the information return should be filed within 15 months after the end of the second year, and the top-up tax return and payment term end 17 months following the end of the second year. As such, there is a bit more runway for taxpayers to allow for sufficient time to process the complex Pillar Two top-up tax information return calculations in a proper top-up tax return.

For this first episode Flora sat down with pitch coach David Beckett of Best3Minutes on how to create a winning pitch. Pitching is a very important part of a US expansion but not necessarily something that all European entrepreneurs are prepared for. In this episode David talks about the key elements of a great pitch, what US investors are looking for in a pitch and he explains the cultural differences between Europe and the US.

David Beckett is an international pitch coach, who has trained over 1800 Startups and Scaleups to win over €400Million in investment. He’s also trained more than 250 Dutch startups to pitch in the USA, for trade missions, and at events such as CES. David is the creator of The Pitch Canvas©, author of the books Pitch To Win and Blue Moon Pitch, and has coached over 30 TEDx speakers.

LinkedIn: linkedin.com/in/

Website: www.Best3Minutes.com

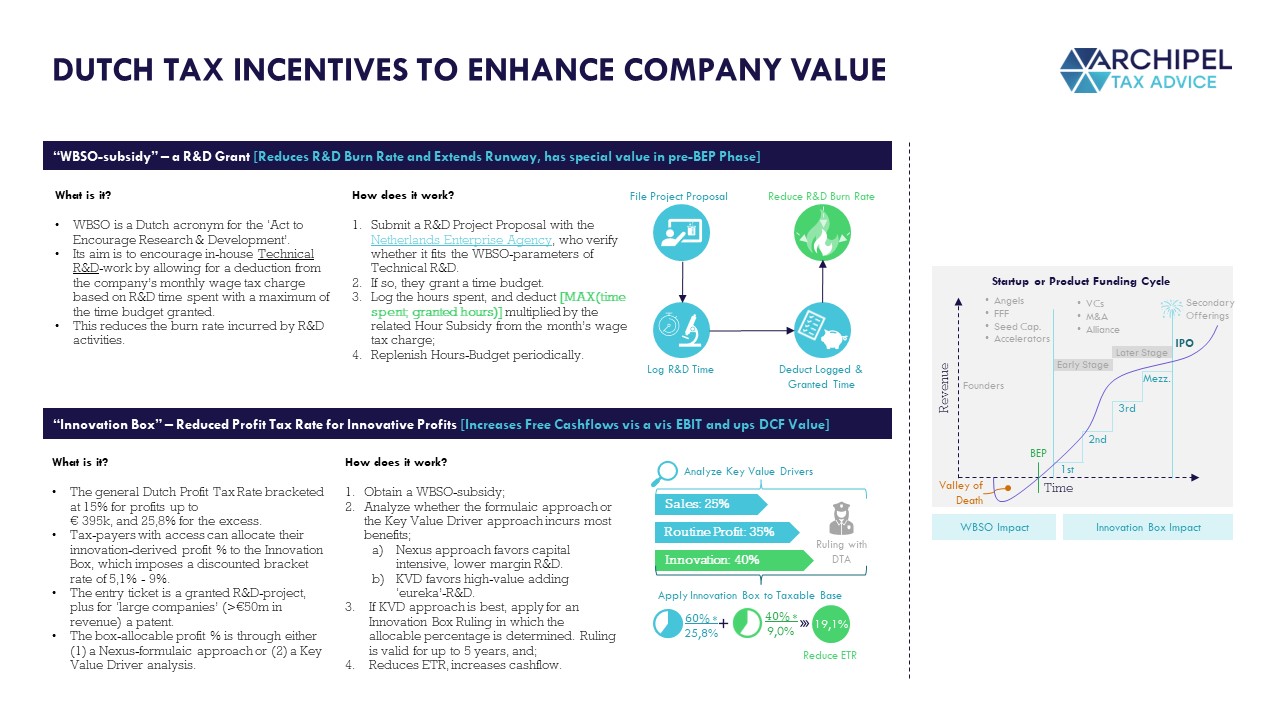

As a small country with a high-income economy, limited natural resources and little manufacturing, the Netherlands has adopted policies to facilitate the knowledge economy. The Dutch government is therefore looking for ways to highly incentivize R&D activities performed in the Netherlands by providing tax incentives to Dutch companies and individuals. This is done by 1) greatly reducing wage taxes on the R&D performed in the Netherlands (the cost-side) and 2) providing a special corporate income tax regime for any profit generated with R&D (the profit side). Both lead to a lower Effective Tax Rate, thus higher free cashflows, and as such a higher Company Value on a DCF basis (check out our explanation of the DCF method for valuating companies: NL/ENG).

In this long-read, we will provide you with the ins and outs of these Dutch tax regimes that incentivize R&D activities.

The WBSO is an R&D remittance reduction intended to incentivize businesses to invest in research & development. This incentive greatly mitigates the cost-burden of R&D-companies by reducing the wage tax of employees conducting R&D activities. To obtain the benefits, an application needs to be filed with the Dutch Enterprise Agency (RVO) (in Dutch: Rijksdienst voor Ondernemend Nederland). The application boils down to: 1) proving that you are dealing with a project that contains a technical bottleneck, which 2) cannot be solved by any known techniques, and 3) requiring you to perform R&D work to find a solution.

For wage tax withholding agents (i.e. employers), the WBSO entails a reduction in the wage tax to be paid for its employees conducting R&D activities. In 2022, this so-called ‘R&D remittance reduction’ is 32% of the R&D base up to € 350,000, and 16% thereafter. If you qualify as a ‘starter’ (i.e. you employ people for less than 5 years and were granted the WBSO-statement for <3 calendar years), you are eligible for an R&D remittance reduction of 40% over the first € 350,000.

| R&D Base | Regular | Starter |

| €0 till €350,00 | 32% | 40% |

| From €350.000 | 16% | 16% |

The R&D base – which functions as the basis for the wage remittance reduction – can be calculated in two ways:

Method 1: based on the number of R&D hours: this is the more straightforward regime, where the amount is calculated based on the number of hours granted, with an average hourly wage of € 29 plus an additional amount of € 10 per R&D-hour (up till 1,800 R&D hours) and € 4 for any additional hours on top of the 1,800 hours.

Method 2: based on the actual costs and expenses that relate to the R&D activities.

In case you would like to calculate the potential WBSO-benefit yourself, feel free to use our open-source Excel-file. You can download the Excel file here:

A WBSO-statement always applies to any future R&D work performed by the company. As a result, you will need to make a forecast of the number of R&D hours you are planning on spending (method 1).

Make sure to apply for a reasonable number of R&D hours. The reason is that the RVO 1) checks whether the number of R&D hours requested isproportionate to the project and the amount of FTE involved, and 2) the RVO regularly audits companies on their number of R&D hours spent. In case the number of R&D hours for which you applied cannot be justified, you risk a correction and a fine.

While analyzing the R&D activities of a potential WBSO-applicant, we sometimes notice that the company itself does not consider the project to be ‘innovative’. In most cases this is caused by 1) R&D employees perceiving the R&D work as ‘simple’ due to them being experts in their respective field, or 2) comparing the R&D activities/ the unfinished product to the (finalized) product of a competitor. Though we understand that this might seem problematic when filing a WBSO-application, we would like to stress that both these factors are completely irrelevant for WBSO-purposes. The only relevant factor when determining if a project qualifies for WBSO-purposes is whether you aim to solve a technical bottleneck that cannot be solved by any known methods. It is therefore irrelevant if this work is perceived as simple by the R&D employees or whether a competitor has already solved this bottleneck. For instance: the RVO will not reject a WBSO-application in case you are planning on solving a technical bottleneck for a new ‘Google-like’ search engine, just because Google itself might have a way of solving the technical bottleneck. What isn’t considered R&D work – and will not qualify for WBSO-purposes – is using existing technologies to solve technical bottlenecks. For example: creating a machine learning model by utilizing certain libraries (such as Tensorflow) will not qualify as R&D work, but developing a machine learning model from scratch (and solving a technical bottleneck in the process) will.

The Dutch innovation box is a special corporate income tax regime for companies who generate profit via a self-developed intangible asset. Any profits that fall under the scope of the innovation box are effectively taxed at a corporate income tax rate of ~9% instead of the statutory rates of up to 25.8%.

The Dutch corporate income tax act differentiates between so-called small-sized companies and larger-sized companies. The requirements a company needs to meet in order to apply for the Dutch innovation box vary depending on its size. For the small-sized companies, the application can be filed as soon as a WBSO-statement is issued by the Dutch Enterprise Agency. Larger-sized-companies require a patent or a so-called plant breeders’ right (in Dutch: Kwekersrecht).

A company qualifies as a ‘small-sized company’ if:

The innovation box benefit can be calculated via four methods:

Which method is best suited for your business depends on your business model as well as the role R&D fulfills within your company. In practice, a functional analysis of your company will determine which method is most suited and which percentage of the profit is subject to the innovation box scheme. For completeness’ sake, we would like to note that it is a common misunderstanding that 100% of a company’s profits can attributed to the innovation box. Even the most high-tech companies in which R&D is interwoven in their entire business process cannot allocate all of their profits to the innovation box scheme. The tax authorities will – in such a case – always consider a part of the profits to be allocable to an entrepreneurship-like function within a company.

In case R&D is a core activity within your company and the profits that relate to an intangible asset cannot be determined on a stand-alone basis, the peel-off method is the most suited method. The peel-off method is – in most cases – the most beneficial way of determining the innovation box profit, as the entire EBIT (‘Earnings before interest and tax’) of the company will be considered the starting point. This method works by allocating a small part of the profits to the more routine-like functions within the company. The remainder of the profits is then allocated to the core divisions/functions within the company. In a way: you are ‘peeling off’ the company’s functions layer by layer.

An example of the peel-off method allocation per core-division would be:

| Entrepreneurship | 20% |

| Sales | 10% |

| Production | 30% + |

| Total: | 60% |

| Attributable to R&D | 40% + |

| Total: | 100% |

In the above example, 40% of the company’s profits are allocable to innovation, and will therefore be taxed against an effective corporate income tax rate of ~9%.

Well, that depends on the activities of the company. The Dutch tax authorities will take the position that the peel-off method is the most suited method if the R&D-activities are an essential part of the day-to-day operations. This is the case if R&D activities are interwoven in all of the company’s operations and the R&D function is one of the most important functions in terms of value creation for the company.

When applying the peel-off method, a functional analysis determines which part of the profits is allocable to each division/function. The exact percentage per division depends on the size of the company (smaller or larger size), the industry and the function R&D fulfills within the company. Factors that may be relevant in this analysis are:

It is important to note that the innovation box regime contains a hurdle for the development costs that relate to the development of the intangible asset. In short: the innovation box regime will only be applicable if the development costs for the intangible are compensated by the profits generated by said intangible. The goal here is to prevent a deduction of development costs against the standard corporate income tax rate of 25,8% (maximum), while the profits are taxed against an effective tax rate of ~9%.

In case innovation is not considered a core-activity within the company but rather complementary to the company’s core activity, the Dutch tax authorities may take the position that the innovation box profits should be determined on a cost-plus basis.

The cost-plus method entails adding a mark-up on all costs (direct & indirect) relating to the R&D work. This mark-up is determined by benchmarking the remuneration an independent third party would receive for these R&D activities.

Under normal circumstances, a mark-up between 8% – 15% is accepted by the Dutch tax authorities.

The single intangible asset method is very similar to the peel-off method. When applying the single intangible asset method, the operational profit needs to be divided between routine functions and core activities/divisions of the company. The difference here is that – while the peel-off method considers the EBIT (‘earnings before interest and tax’) as the starting point – the single intangible asset method only takes the development costs and the ‘benefits’ that directly relate to the intangible asset into account. The single intangible asset method is generally used to calculate the innovation box profits in royalty structures, where there is a direct and easily identifiable revenue stream that relates to the intangible asset.

Note that – same as for the peel-off method – a hurdle based on the development costs applies.

In the event that the earlier described methods are deemed to be too complex, there is always the possibility of utilizing the flat rate method. Based on this method, 25% of the profit will fall under the scope of the Dutch innovation box. The benefit is however capped to € 25,000 on a yearly basis, making this – in most cases – only a viable option for a small/ start-up company.

Although it may seem a bit nitty gritty, it is important to note that the innovation box benefit is actually a tax base exemption -rather than a tax rate reduction- calculated via the following formula: (16/25.8) x innovation box profits (2022). This exemption results in an effective tax rate of ~9% for any profits that are subject to the innovation box scheme. It also results in an additional – and in most cases unforeseen – benefit that the innovation box scheme ‘extends’ the first corporate income tax bracket.

Besides the fact that the innovation box reduces the effective tax rate of profits that fall within its scope, the innovation box also positively influences the remainder of the profits. This is a result of the fact that the remainder of the profits (i.e. part of the profits that are not subject to the innovation box) are taxed against the regular, below-mentioned corporate income tax rates.

| Taxable profit (2022) | Tax rate |

| € 0 till € 395,000 | 15% |

| From € 395,000 | 25.8% |

Consequently, the remaining profits will first be taxed in the first bracket at a tax rate of 15% up to € 395.000, thus further reducing the effective tax rate. In case you are wondering how this would affect the effective tax rate of your organization, feel free to use our Excel-file which shows you the effective tax rate depending on the taxable profit and the innovation box percentage. Note that we based this Excel file on the peel-off method. You can download our Excel file here:

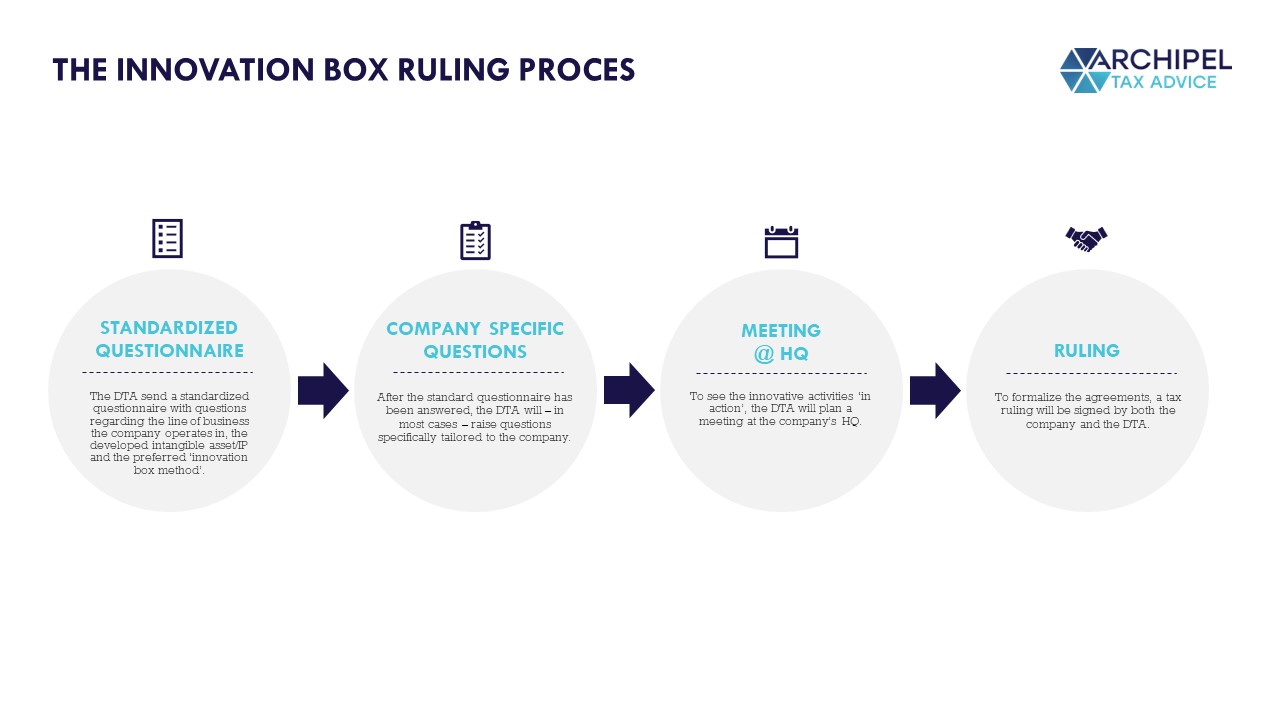

The innovation box ruling process starts with a ruling application request. Once filed, the Dutch tax authorities will send over a standardized letter containing several questions to get to know the applicant. These questions relate to: 1) the line of business in which the company operates, 2) the intangible asset/ intellectual property developed by the company and 3) the preferred method to determine the innovation box profit. In most cases, the Dutch tax authorities will request a company specific questionnaire following the initial application. Once the Dutch tax authorities have a clear initial image of the company’s business, they will plan a meeting at the company’s HQ. This meeting is meant to help the Dutch tax authorities understand how the business operates and what role R&D fulfills within the company. After the meeting, the Dutch tax authorities and the company will conclude a tax ruling . The ruling will contain:

To further specify which part of the profits will be subject to the innovation box scheme, an addendum to the ruling request will be concluded, based on the company’s commercial forecasts. The ruling will be concluded for a period of 5 years.

You are able to outsource some of the R&D work as long as the costs that relate to the R&D work (as well as any potential risks) are borne by the innovation box applicant.

Outsourcing to an affiliated entity is possible, but may impact the total innovation box benefit. The Dutch corporate income tax act contains a limitation on the innovation box benefits that relate to the outsourcing of R&D work to an affiliated entity. The reason is that – in most cases – affiliated entities are able to structure their R&D activities between different jurisdictions. To mitigate any unwanted tax structuring which might arise in such a case, the innovation box benefits will be limited based on the following formula:

| Qualifying innovation box benefits = | Qualifying expenses X 1,3 ________________________ Total expenses |

X benefits |

In the above formula, the outsourced R&D expenses to an affiliated entity are not considered ‘qualifying expenses’. As a result, a maximum of 30% of the expenses can be outsourced to an affiliated entity without it impacting the innovation box benefits.

Every tax ruling contains a clause stating that the ruling remains valid as long as the relevant facts and circumstances do not change. In such a case, you are obligated to notify the Dutch tax authorities accordingly. This may result in the termination of the current ruling.

Unfortunately, it is not possible to file a WBSO-application to retroactively receive a wage remittance reduction for any additional R&D hours. As a WBSO-application does need to be filed on a yearly basis however, you are therefore able to file a new request next year. For completeness’ sake, we note that you are obligated to notify the Dutch Enterprise Agency in case you spend less than the requested number of R&D hours. As a result, the wage remittance reduction will be reduced accordingly.

While concluding an innovation box ruling, the Dutch tax authorities may consider an start-up phase to be present. The duration depends on the innovation type as well as the business structure. As soon as this period ends, you are able to allocate the full amount – 15% of the EBIT – to the Dutch innovation box. For example: in case you conclude a start-up phase of 3 years and an R%D percentage 15%, you will receive an innovation box allocation of 5% in the first year of the ruling, 10% in the second year and finally 15% in the third year.

Where R&D-cycles generally see any revenues being proceeded by a cost-burning phase, a cost-side tax benefit can logically make an R&D project more feasible, as it (1) reduces the burn rate and (2) lengthens the runway. The WBSO does exactly that and therefore provides great value in the ‘pre Break Even Point’ phase.

Investors investing in ‘post-BEP phase’ companies are generally enticed into the high-risk financing of an R&D cycle by the calculation of (1) the chance of success * (2) the rate of return. As the investor rate of return is influenced heavily by profit tax functions, the innovation box can make an R&D project in the post-BEP phase more feasible as well since it increases the outlook of factor (2).

By combing both the WBSO and subsequently the innovation box, a more attractive investment case can thus be achieved.

Interested in applying the WBSO and/or innovation box to your company? Book a timeslot with us below, it’s on the house!

Partner at SAMMAN, President at European Network for Women In Leadership, Board Member Focus Home Interactive

Chief Quality Officer and member of the Executive Board, Deloitte Netherlands

Women on Supervisory Boards: Why is this issue important? Who is affected?

Liesbeth

In the Netherlands, supervisory boards have traditionally shown the same picture: white men in grey suits. Luckily this picture has been changing over the past five years. As the role of the supervisory board became more relevant and gained in-depth, awareness rose that the presence of diverse viewpoints within them is important in order to avoid “groupthink” and tunnel vision. Yet the tendency was still to appoint new supervisory board members from the “old boys network.” Forcing a breakthrough legislation was necessary. In the Netherlands, we now have so-called quota legislation, in which it is ruled that 1/3 of the supervisory boards will have to be comprised of women. As long as this quotum has not been reached, appointments of new male supervisory board members are invalid. The impact of this legislation on the supervisory boards is already being felt. A lot of listed companies now have at least 1/3 of women on their supervisory boards. The next important step will be that management boards also have the necessary diversity.

Thaima

The issue of the representation of women in all facets of life goes to the heart of democratic values and governance. In my role as President of the European Network for Women in Leadership, I see the subject of the feminization of leadership and management under discussion all over Europe. Studies have shown that companies with higher levels of gender diversity outperform those with male-dominated management, and the larger goal—beyond women on supervisory boards—is for more women in executive roles generally.

Following Norway’s lead in 2006, eight EU countries have adopted mandatory gender quotas for listed companies, including France, Belgium, Italy and the Netherlands, with ten others having taken a more incentive-driven approach. In their search for female talent, male leadership is discovering that this talent exists! The visibility of successful women and a constellation of heterogenous role models contributes to the development of a pipeline of female talent and future female leaders.

This trend, however, is not irreversible, and we need to remain vigilant, especially in times of social and economic upheaval. Some companies appoint women to their boards to comply with the law but make sure that they have no real power or influence. Having the same few women sit on several supervisory boards rather than looking for other talent is also not uncommon.

What have you seen on the ground?

Liesbeth

The NSE supervisory board has oversight over the NSE executive board. NSE is Deloitte’s European organization and consists of 28 geographies.

On our board, we have over 50% female representatives, all with different cultural backgrounds. We also have three independent non-executives on our supervisory board, which assures the objectivity of this board. We strive for a certain percentage of women and different cultures on this board and have open conversations about how to reach the targets. We have a strong focus on people and on the long term, and we keep in mind the impact our decisions will have on our legacy. We believe strongly that our diverse board provides the diversity of thought necessary for discussions and decisions of value, for both the short and long term.

My main takeaway is that inclusivity and diversity are a “must” for boards; we have to take firm steps and be open about dilemmas and our values. Whatever form of diversity we strive for, cultural diversity, gender diversity, ultimately, it is about diversity of thought. And we in our NSE board see the benefits of having diversity of thought: in decision making and in having meaningful discussions.

Thaima

The Deloitte example is a great one and a best practice to communicate broadly.

I am currently a board member of Focus Interactive, a gaming company. The company clearly wants to work with their supervisory board members on business strategy. The other board members coming from the same world, my female colleague and I bring fresh air and new perspectives, she with a financial background, and I with my law and public affairs perspectives—gained from ten years at Microsoft as Legal and Corporate Affairs General Counsel, and subsequent work with a Law and Corporate Affairs firm.

My takeaways:

What’s coming next?

Liesbeth

An important next step is moving from diversity to inclusion. The good news is that there will be more women on boards as a result of quota legislation. However, if the culture does not change and women do not feel safe enough to ask questions and express differing views, there is no inclusion and no benefit from having diverse points-of-view. The Chair of the supervisory board must create an atmosphere in which everybody can be open to ask questions and express views. At this moment, diversity is too often seen as just a check-the-box exercise. If boards look different but still act the same, there has been no real progress—the company will not benefit from diversity of thought. More action is needed to go from diversity to inclusion.

Global progress on gender equality is encouraging, but overall, progress is slow. It has therefore become even more important to take concrete action, appointing more women not only to supervisory boards but also to boards of directors. We should also challenge if 1/3 of women on boards is sufficient because then it still doesn’t give a balance in boards since you have a predominance of men, which obviously has its effect on discussions, decisions and also on inclusion.

Thaima

Companies now have a diversity of profiles in their workforce, and management and leadership teams are more resilient and more successful as a result. The coming together of different skills and ideas helps align companies in the diverse societies they operate in and better understand their markets and customers. These types of factors, while well understood, are not always taken into account at the right level of management, and old reflexes and stereotypes are still alive and kicking.

Women are now equally, if not more, educated than men. Aside from the topic of women on supervisory boards, tackling the broader issue of women in leadership positions also addresses corporate governance and the need to recruit and retain female talent.

There is not one legal tradition in Europe but several. This results in huge differences between countries according to their cultures, histories and legal traditions. I believe it is necessary for the European Union to continue taking initiatives to align the policies of member states, levelling them up to the standards in the more advanced countries. The recent deal on the Directive on Women on Boards, which had been blocked for ten years, should make a big difference and will complement EU efforts to mainstream gender into wider policy-making processes, including, most recently, by making it a criterion for receiving EU Covid recovery funding.

#internationaltravel has resumed and as of June 12th #covidtesting

Yet members across the #EACC #network report that entry to the #us remains fraught.

Let us know either way through the link below!

(takes 1 minute)

On the 22th of December, the European Commission (hereinafter: ‘EC’) has presented an initiative to combat the misuse of shell entities for improper tax purposes (‘ATAD 3’). This proposal will ensure that shell companies in the EU with no- or minimal economic activity are unable to benefit from any tax advantages, consequently discouraging their use. Furthermore, the Commission Ter Haar published a report on ‘doorstroomvennootschappen’ in the Netherlands last October.

Shell companies can be used for aggressive tax planning or tax evasion purposes. Businesses can direct financial ‘flows’ through these shell entities towards tax friendly jurisdictions. Similar with this, some individuals can use shell entities to shield assets – more specific real estate – from taxes, either in their respective home country or in the country where the property is located. The main purpose of this proposal is therefore to address the abusive use of so-called shell companies, being referred to as legal entities with no, or only minimal, substance and economic activity.

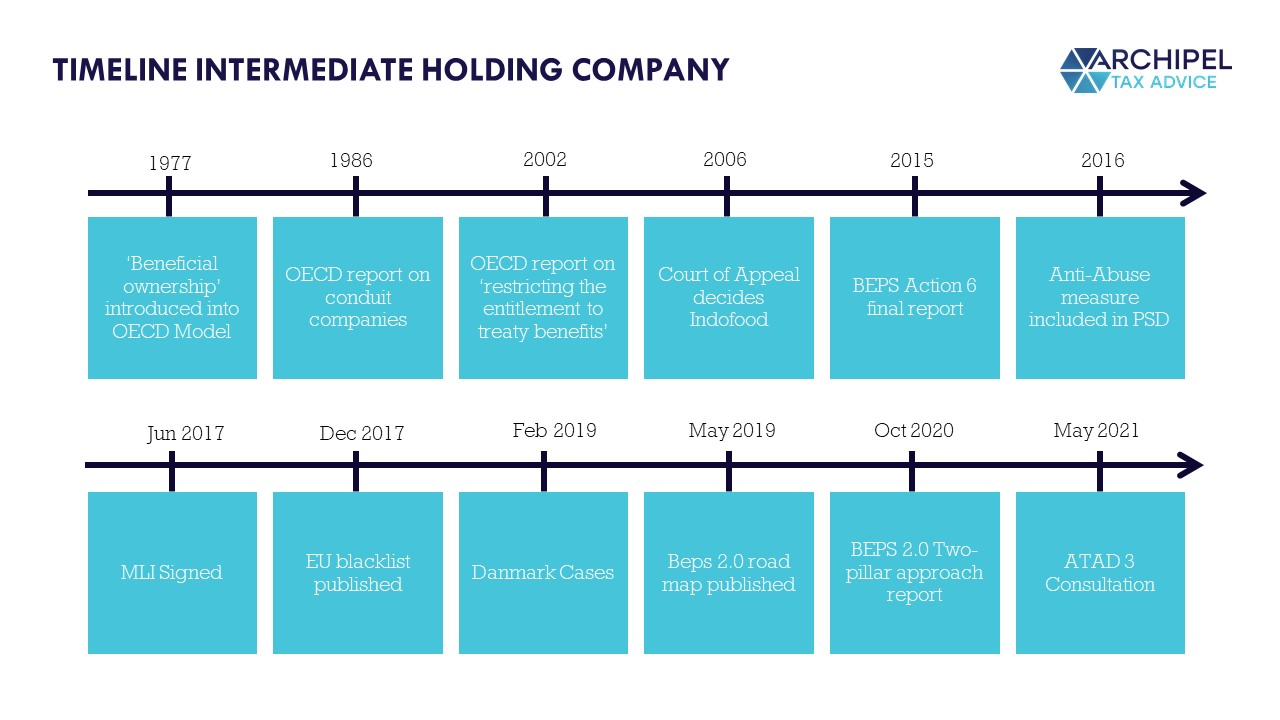

International groups often use intermediate holding companies to hold shares in subsidiaries organized on a regional or divisional basis. Furthermore, holding companies are often used as the vehicle for investing in portfolio companies in a private equity context. In past times, it was not particularly controversial that holding companies were entitled to the potential benefits of tax treaties and potential directives in their country of residence. This would frequently restrict the right of investee jurisdictions to tax dividends and gains derived by the holding company from its local subsidiaries. As shown in the timeline underneath, the perception and position of these companies has changed, with an accumulation of measures that potentially restrict the access to the benefits and directives.

This all started with the introduction of the term “beneficial ownership” into the OECD’s Model Tax Convention in 1977. The question was asked: who does actually benefit from this/these payment(s)? Whilst being slightly controversial in the 70’s, the term now appears in most tax treaties and intents to prevent treaty shopping by ensuring that the benefits of the dividends, royalties and interest articles are only accessible to residents of the contracting state that are the beneficial owners of the payment. After this, the OECD’s report on the use of conduit companies in 1986 ruled conduit companies out of the beneficial ownership regard. Nevertheless, there was no generally agreed definition of the term ‘beneficial ownership’ in tax treaties and the interpretation would follow the domestic law of the contracting states. The first hint of an international fiscal meaning of this term stems from the Indofood case (Indofood International Finance Ltd. V JP Morgan Chase Bank NA, 2006). To prevent falling foul of the beneficial ownership test, certain groups reviewed their holding structure(s) and looked to eliminate fully back-to-back financing arrangements. Furthermore, some structures which involved payment chains were set up with an “equity gap”. These structures reflected a widespread view that beneficial ownership was an objective test that was indifferent to the motives behind these holding company arrangements.

Whilst having a long history, reverting back to said changes in the OECD model treaty in the 70’s, the real challenge to the treaty status of holding companies began in 2015, when the Base Erosion and Profit Shifting project (‘BEPS’) recommended measures to restrict inappropriate usage of tax treaties. The bar is consequently set higher and higher for the criteria that holding companies need to meet in order to benefit from relief from withholding taxes and exemptions to non-resident capital gains tax. The high apex for this approach is the just published proposal to end the misuse of shell entities. Some of the statements suggest that it may never be appropriate for an intermediate holding company (using the term ‘shell entity’) to benefit from reductions in withholding taxes under tax treaties and EU directives.

The Dutch government already set up a commission that investigated the use of the so-called shell companies and their potential misuse of the Dutch tax system. This report was published last October.

‘Doorstroomvennootschappen’ (as they’re often referred to in Dutch) provide little benefit to the Dutch economy, disadvantage developing countries disproportionately through loss of tax revenue for developing countries in particular, and the phenomenon damages the reputation of the Netherlands. These are the main conclusions of the Committee on Flow-through Companies, chaired by Mr. Ter Haar, which presented its final report recently.

The committee describes the relevant components of the Dutch tax system that, at least until recently, have made the Netherlands attractive to flow-through companies. These include the participation exemption, the extensive treaty network, the absence of a withholding tax on interest and royalties and the ruling practice. The report describes examples of unintended use of each of these aspects of the Dutch tax system. In combination with the well-organized financial advice and services sector, this has led, according to the Committee, to a sizeable financial flow. The Committee believes that the measures already taken are expected to put an end to (part of) the tax-driven flow of interest and royalties. This does not mean that the Netherlands should be expected to lose its position as a country of establishment for empty holding companies, even though the Dutch tax system is no longer unique compared to other countries. According to the Committee there will still be a large group of (almost) empty conduits that make use of the Dutch tax infrastructure, whose contribution to the economy is small. The Committee therefore recommends further steps, but at the same time sees that far-reaching unilateral measures do not immediately offer a solution. In the first place, the Committee recommends a proactive attitude and a pioneering role with respect to international and European initiatives. These include the revision of the international tax system within the Inclusive Framework of the OECD and the announced EU Directive proposal on flow-through companies. According to the committee, the Netherlands should advocate measures that involve both the targeted exchange of information and to limit the benefits of the Interest and Royalties Directive and the Parent-Subsidiary Directive.

The advantage of this structure is that the dividends, by making use of the Dutch treaty network, without or with reduced withholding of local tax, arrive at the company in the country of residence (Country A), without or with reduced withholding of local tax, compared to the situation where the payment is made directly to the country of residence (Country A) by the source country (Country C). This is just one example of a (flow-through) structure in which the Dutch treaty network plays a role, in combination with the participation exemption and the dividend withholding tax exemption in treaty situations.

Because the Netherlands has long had a large bilateral tax treaty network, the Netherlands is an attractive country for ‘treaty shopping’. When the tax treaties are concluded, it is assumed that it is up to the source country to prevent the reduced rate of withholding tax, which is wrongly applied mostly.

Unilateral measures cannot prevent other countries from playing the role as flow through country. To avoid international tax avoidance through ‘empty entities’, international agreements are therefore necessary. The committee lastly advises also a constructive attitude by the Netherlands to the ongoing initiatives of the European Commission.

The public perception of tax evasion has shifted in recent years, by taking a drastic turn. In particular, the credit crisis of 2008 has changed the social acceptance of tax avoidance by multinationals in particular. With government deficits and rising government debt, it was considered unfair that a number of multinationals paid (relatively) little tax on their world profits.

This all accumulated into a public hearing of officials of Amazon, Google and Starbucks organized by the Public Accounts Committee in the UK in 2012. The committee chair Ms. Hodge said (the later iconic words):

“We’re not accusing you of being illegal, we’re accusing you of being immoral”.

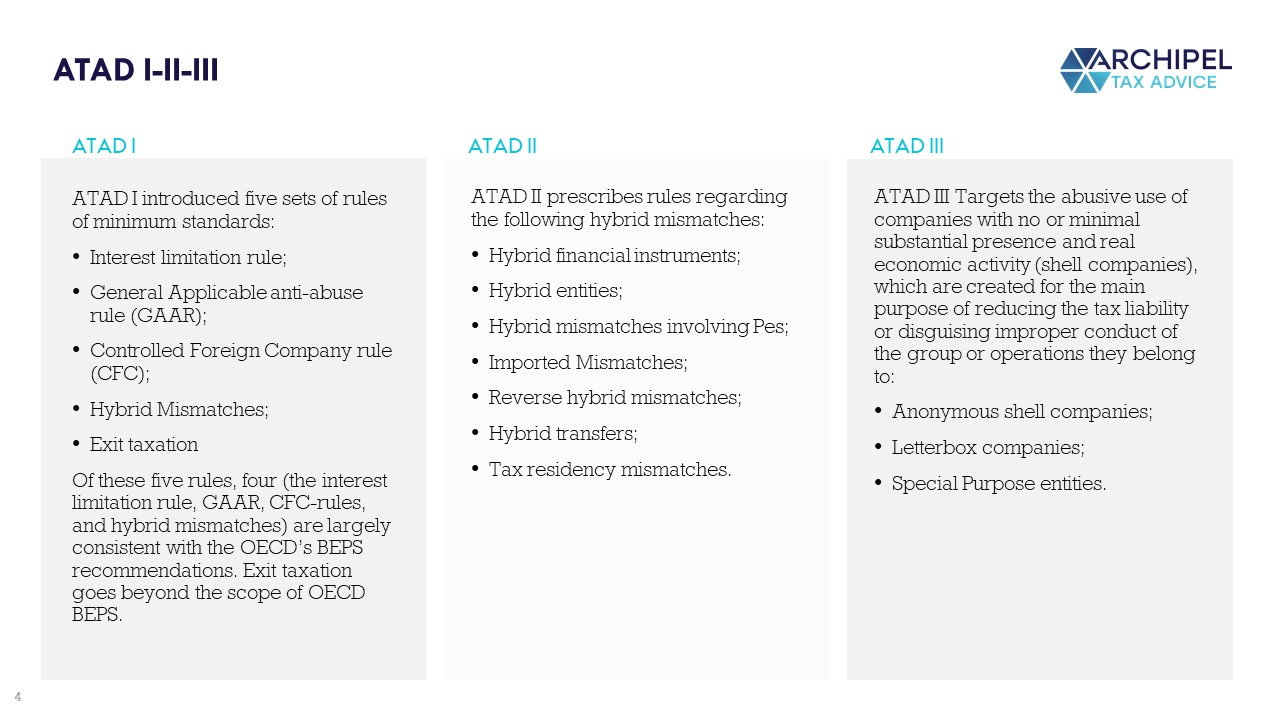

This all led to the BEPS-project and consequently ATAD. There have been 2 Anti-Tax-Avoidance-Directives already put into effect. ATAD 1 introduced 5 sets of minimum standards (interest limitation rule, GAAR, CFC rules, hybrid mismatches and exit taxation). In the second ATAD, subsequent rules relating to hybrid mismatches were finalized on 29 may 2017 when the ECOFIN accepted this directive. ATAD is based on Article 115 of the Treaty on the Functioning of the EU (‘TFEU’).

The definition of the widespread term ‘shell’, often interchangeably with terms such as ‘letterbox’, ‘mailbox’, ‘special purpose entity’, special purpose vehicle’ and similar, is defined differently in different contexts. For the purpose of ATAD 3, shell companies refer to three types of shell companies:

The main common feature of the above three types is the absence of real economic activity in the Member State of

registration, which usually means that these companies have no (or few) employees, and/or no (or little)

production, and/or no (or little) physical present in the Member State of registration

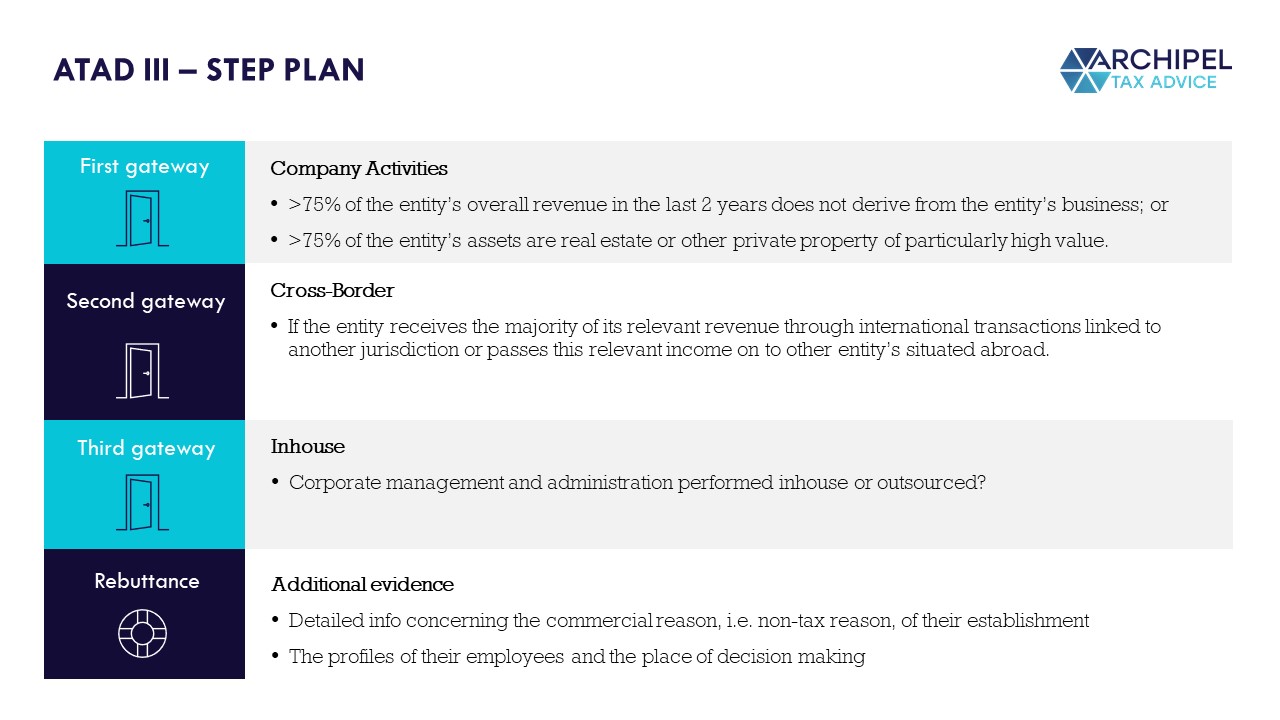

The proposed rules will establish transparency standards around the use of shell entities, so that their abuse can be detected more easily by tax authorities. Using a number of objective indicators related to income, staff and premises, the proposal will help national tax authorities detect entities that exist merely on paper.

The proposal introduces a filtering system for the entities in scope, which have to comply with a number of indicators. These different levels constitute a type of gateway. This proposal sets out three gateways. If an entity crosses all three gateways, it will be required to annually report more information to the tax authorities through its tax return.

The first level looks at the activities of the companies based on the income they receive. This gateway is met if >75% of an entity’s overall revenue in the last two tax years does not derive from the entity’s business activity or if more than 75% of its assets are real estate or other private property of particularly high value.

The second level requires a cross-border element. If the entity receives the majority of its relevant revenue through international transactions linked to another jurisdiction or passes this relevant income on to other entity’s situated abroad, the entity passed to the next and last gateway.

The third, and last, level focuses on whether corporate management and administration services are performed in-house or are outsourced.

An entity crossing all levels will be obliged to report information in its tax return related to the premises of the entity, its bank accounts, the tax residency of its directors and employees etc. These are the so-called substance requirements. All declarations should be accompanied by supporting evidence. If one of the substance requirements isn’t met, the entity will be presumed to be a ‘shell company’.

Once adopted by the Member States, the Directive should come into effect on 1 January 2024.

If the substance criteria are not met, entities still have the opportunity to rebut the presumption of being a shell. Additional evidence needs to be presented, such as detailed information about the commercial, non-tax reason of their establishment, the profiles of their employees and the fact that decision-making takes place in the Member State of their tax residence.

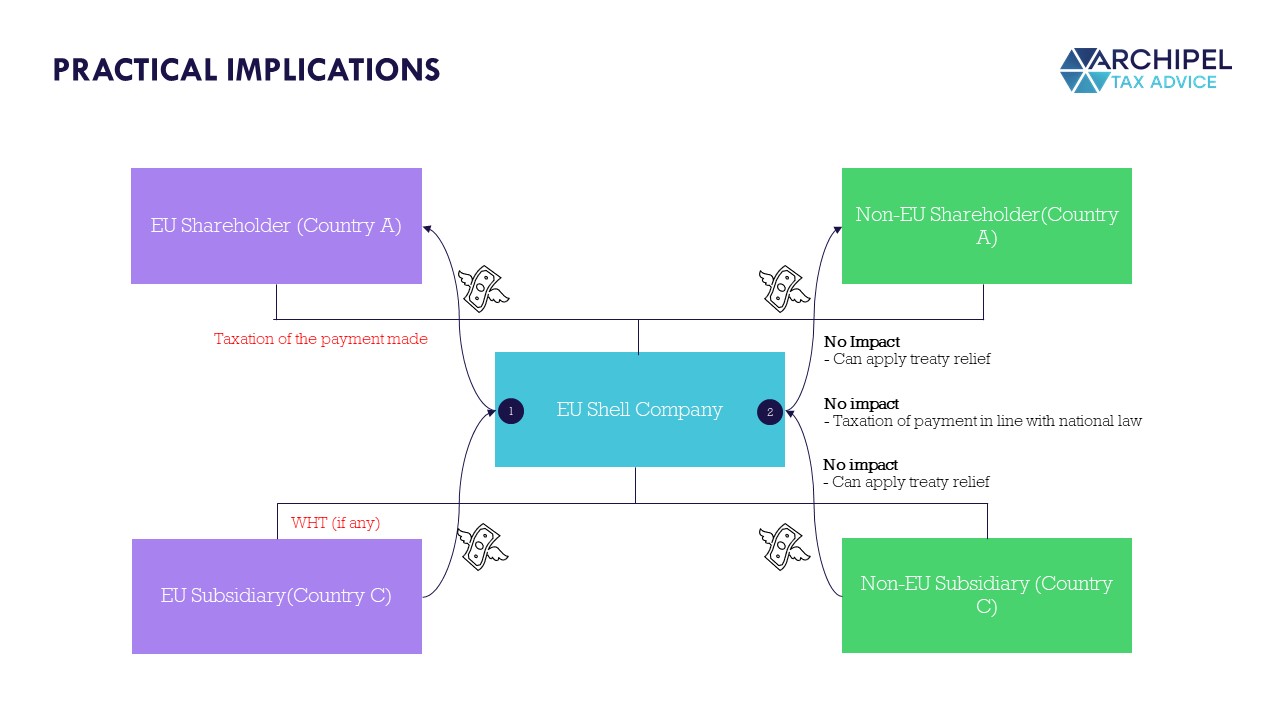

If an entity is deemed to be a shell company, the benefits and reliefs of the tax treaty network of its Member state are not applicable. Furthermore, the company will not be able to qualify for the treatment under the Parent-Subsidiary and Interest and Royalty Directives. To support the implementation of these consequences, the Member State of residence of the company will either deny the shell company a tax residence certificate or the certificate will specify that the company is a shell.

Furthermore, payments to third countries will not be treated as flowing through the shell entity, and will be subject to withholding tax at the level of the entity that paid to the shell. According with this, inbound payments will be taxed in the state of the shell’s shareholder. Relevant consequences will apply to shell companies owning real estate assets for the private us of wealthy individuals and which as a result have no income flows. Such real estate assets will be taxed by the state in which the asset is located as if it were owned directly by the individual.

Scenario 1 EU source jurisdiction of the payer – EU shell jurisdiction – EU shareholder jurisdiction

In this case, all three jurisdictions fall in the scope of the Directive and are consequently bound by ATAD3:

Scenario 2 Non-EU source jurisdiction of the payer – EU shell jurisdiction – Non-EU shareholder jurisdiction

Scenario 3 Non-EU source jurisdiction of the payer – EU shell jurisdiction – EU-shareholder jurisdiction

In this case the source jurisdiction is not bound by ATAD 3, while the jurisdictions of the shell and the shareholder fall in scope.

Scenario 4 EU source jurisdiction of the payer – EU shell jurisdiction – third country shareholder jurisdiction

In this case only the source and the shell jurisdiction are bound by ATAD3 while the shareholder jurisdiction is not.

Scenarios where shell entity’s are resident outside the EU fall outside the scope of ATAD3.

First of all, monitoring the developments in the BEPS 2.0 and ATAD 3 proposals is advised. Also, looking at whether there are operating entities withing the group in low tax jurisdictions, entities with primarily passive income, and companies where the local substance may fall short on the types of criteria suggested by the EC. When the key risks are identified, choices may include removing problematic holding companies, using different jurisdictions, or taking steps to bolster local substance. International groups should take the appropriate measures in time to get ahead of these changes.

Do you have questions regarding the implications of ATAD 3 for your company or do you need certainty in advance? Feel free to call us! This is really dynamic work, which also gives you insight into your compliance with the changing international rules. We are happy to help.

On 21 September 2021, the government submitted the 2022 Tax Plan Package to the Lower House. This package includes the following bills:

Moreover, a bill has been presented that aims to counter mismatches in the application of the arm’s length principle in corporate income tax.

Most measures will enter into force on 1 January 2022. Where this is not the case, we have indicated this. The bills may be amended during their parliamentary debate. The proposed measures per type of tax type are listed below.

Corina van Lindonk, Aart Nolten and Eddo Hageman discussed the most noticeable measures of Tax Plan 2022.

Outline of corporate income tax and dividend withholding tax measures

Outline of procedural tax law, collection of taxes and supplementary benefits

| Tuesday 21 September 2021 | Budget Day: introduction. |

| Wednesday 29 September 2021 | Closed technical briefing by civil servants of the Ministry of Finance. |

| Wednesday 6 October 2021 | Contribution date for the report. |

| Tuesday 19 October 2021 | Memorandum of reply. |

| Monday 25 October 2021 | First legislative consultation. |

| Thursday 28 October 2021 | Written answers to questions in response to the first legislative consultation. |

| Monday 1 November 2021 | Second legislative consultation. |

| Tuesday 9 and Wednesday 10 November 2021 | Plenary hearing. |

| Thursday 11 November 2021 | Letter on evaluation of motions and amendments. |

| Thursday 11 November 2021 | Voting. |