Why is the European Commission putting forward Accelerate EU?

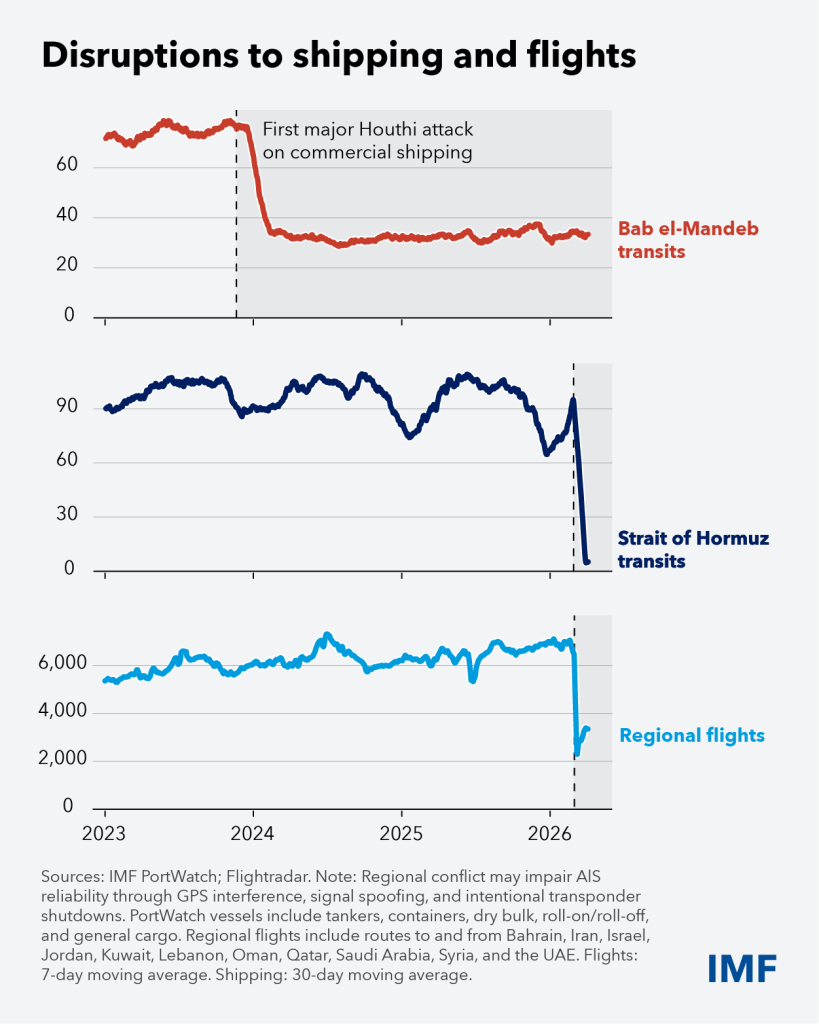

The ongoing conflict in the Middle East is heavily impacting global energy markets, with a knock-on effect on the economy, industry and households. Since the beginning of the conflict in the Middle East, the EU has spent an additional €24 billion on energy imports, mainly fossil fuels. Even if hostilities ceased immediately, disruptions to energy supplies from the Gulf will persist for the foreseeable future. Member States using more renewable and/or nuclear energy, and with more flexible grid systems with sufficient capacity and storage, are generally less impacted by the current energy crisis and sharp price fluctuations. The AccelerateEU Communication therefore underlines the importance of accelerating the transition to homegrown clean energy sources. In this context, the Communication focuses on five sets of measures with both short-term and long-term effects:

Greater EU coordination: The Commission will facilitate coordination in areas such as gas storage filling, oil stock releases, adoption of national emergency measures and ensuring the availability of jet fuel and diesel.

Protecting consumers and industry from price shocks: The Commission will assist Member States in the design of targeted, timely and temporary measures to address the crisis, including a temporary State aid framework to support the most exposed economic sectors.

Accelerating the shift to homegrown clean energy and electrification: The Commission will publish an Electrification Action Plan and set an electrification target, alongside other initiatives to increase the uptake of geothermal, biomethane and hydrogen.

Stepping up our energy system: the Commission calls on Member States to accelerate the negotiation of the European Grids Package for a swift adoption before summer 2026 and will adopt a legal proposal on network charges and taxation

Boosting investment:By mobilising both public and private financing for the transition to clean energy.

What is the Commission proposing to protect households and industry from the effects of the crisis?

Household budgets are increasingly tight as high energy costs, including household bills, are reducing disposable income. The Communication presents measures that Member States can take to protect consumers and industry from sudden high price hikes, thereby limiting the subsequent socio-economic impact.

EU rules and initiatives, including the Citizens Energy Package, already set out actions Member States can take to give consumers immediate relief. They include income support, energy vouchers (including for replacing boilers), social tariffs, reducing excise duties on electricity, and VAT reductions for heat pumps, solar PV panels and related small-scale batteries, and tax incentives for e-vehicles.

The Communication also underlines the need to make it easier for individuals to join energy communities, for households to produce more energy themselves and for consumers to be able to compare and switch energy suppliers. To help the most vulnerable, EU rules already enable Member States to bring in a temporary, or full, ban on disconnecting households from energy grids following payment issues. As the cheapest energy is the energy we do not use, the Communication also focuses on energy savings and energy efficiency.

The Commission will also increase the financial support available to industry for their clean energy transition through the Industrial Decarbonisation Bank, mobilising €100 billion of funding, including an Investment Booster financed by 400 million EU ETS allowances aiming to enhance investment certainty to step up decarbonisation investment by EU energy-intensive industries.

What is the Commission presenting for the transport sector?

Measures to ensure that the EU’s transport sector remains competitive and resilient are also included. To ensure sufficient availability of transport fuels and preserve the effective functioning of the single market, the Commission will step up European coordination on the optimisation of fuel distribution across Member States. The Commission will establish a Fuel Observatory, tracking EU production, imports, exports and stock levels of transport fuels. This will enable swift identification of potential shortages and inform targeted measures to maintain a balanced fuel distribution across all regions and airports.

To mitigate the impact of possible fuel shortages on the EU aviation sector, the Commission will provide clarity on existing flexibilities within the EU aviation framework to address the consequences of flight cancellations and other disruptions. The Commission is also committed to further driving the uptake of EU-produced sustainable aviation fuels (SAF) and sustainable maritime fuels (SMF).

More immediate support may be needed due to the pressure on fossil fuel imports and volatile energy prices. Such support should be targeted, timely and temporary and they should be tied to longer-term solutions.

What is the role of the Commission to ease the immediate pressure of fossil fuel imports and support long-term stability?

The Commission is working intensively with Member States, regulators and industry to gather timely information necessary for an effective, coordinated, EU-wide response. Coordination Groups on oil and gas now take place on a weekly basis. Chaired by the Commission, the two fora are well-placed for exchanges of information, for instance, on stocks, refining capacity and alternative import routes, across the EU.

The Commission is collecting national data on available oil stocks and market conditions to provide an EU-wide regional assessment of the situation, as mandated by Energy Ministers at the extraordinary Transport Telecommunications and Energy Council of 31 March. Looking ahead, AccelerateEU foresees closer, and more immediate, coordination of:

Filling of gas storage facilities by Member States and using the flexibility in filling rules.

Oil stock releases to ensure stocks effectively meet EU demand and that Member States’ emergency measures don’t negatively impact the Single Market.

National emergency measures and ensuring the availability of jet fuel and diesel, including oil refinery production capacities, across the EU.

What is the EU doing to protect vulnerable consumers?

High energy prices hit the most vulnerable the hardest. The Citizens Energy Package prioritises energy costs and consumers’ access to energy. It places a strong focus on protecting vulnerable and energy-poor households, with safeguards against disconnections and structural reforms to tackle the root causes of high energy costs.

Electricity taxes and levies make up about 25% of household bills, and the Commission works closely with Member States in reducing them.

In implementing the Citizens Energy Package, the Commission is publishing Recommendations as guidance to further empower and protect consumers, from disconnections for example, and to improve transparency. The aim is to make it easier for consumers to switch to cheaper, more sustainable, contracts that are best suited to them. More flexible contracts can lower costs and reduce exposure to price volatility, especially when combined with energy efficient improvements or pooling energy in energy communities.

EU funds have an important role to play in advancing the clean energy transition. Member States can already use Cohesion Funds for decarbonisation, energy efficiency, and other clean energy projects. Support is also available from EU sources such as the Social Climate Fund to support vulnerable households. In parallel, the Commission looking into additional support for Member States, not least by making maximum use of the current EU budget.

What is the EU doing to protect the industry?

The measures proposed in Accelerate EU aim at bringing immediate relief to both consumers and industry and to have lasting benefits. For instance, the Commission encourages Member States to explore the use of revenues from the ETS for targeted measures that accelerate investments in electrification (e.g. in transport or electrification of heating), industrial decarbonisation and to investments that help reduce electricity prices including through increased renewable electricity capacity. The Commission will also give Member States more space to develop and implement targeted temporary emergency measures to support the most exposed sectors by adopting a State aid temporary framework.

What measures is the EU taking to promote electrification and increase the use of homegrown clean energy sources?

The EU is taking a number of measures in different areas. For instance:

Grids Package: Grids are needed to let power flow at the lowest price from where it is produced to where it is consumed. Investing in the EU grid infrastructure is a crucial step towards further electrification and the increase of homegrown clean energy sources. Grids are the backbone of Europe’s energy system and a prerequisite for a well-functioning, integrated electricity system that delivers clean, reliable, affordable electricity to industry and households. The European Grids Package, proposed by the Commission in December 2025, addresses structural issues by introducing more effective cross-border and cross-sectoral energy infrastructure planning through better coordination at EU level. It also strives to upgrade and digitalise existing infrastructure and to ensure it is used in the most efficient way. The Commission proposal also aims at streamlining permit-granting procedures for both grids, renewable energy and flexibility assets to speed up implementation of projects. The Commission calls on and will support the co-legislators to conclude negotiations on the grids package before the summer

Electrification target: Amongst others, the Commission will set an electrification target and publish an electrification action plan to accelerate the electrification needed to complete the shift to an energy system based on clean and homegrown energy and move away from our dangerous dependency on fossil fuels.

How will public and private investments boost resilience to future energy crises?

It is vital to speed up investment in the clean energy transition now, not least to break EU dependence on fossil fuels and make the EU resilient to future energy crises. Member States that have already invested in the clean energy transition are reaping the benefits, with electricity prices generally below the EU average.

The EU already provides significant funding, including €219 billion under the Recovery and Resilience Facility (RRF).

Member States can already use Cohesion Funds for decarbonisation and energy efficiency, as well as instruments like the Social Climate Fund to support vulnerable households. The Commission will work with Member States to maximise the use of available EU funding and reallocate EU funds where feasible and in line with Member States’ preferences to energy-related investments, including by expanding measures to reduce energy demand and accelerated the deployment of clean technologies such as heat pumps, solar, wind and batteries.

Public funding alone will not be sufficient. To mobilise private capital, the Commission adopted a Clean Energy Investment Strategy in March 2026 and will convene a Clean Energy Investment Summit bringing together the financial services industry, institutional investors, including insurers and pension funds, project developers and public financiers to scale up financing for high-impact solutions such as batteries, charging infrastructure and electrification.

Compliments of the European Commission The post European Commission | Questions and answers on AccelerateEU Communication first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.