Speech by Governor Randal K. Quarles on the economic outlook at the 2021 Milken Institute Global Conference “Charting a New Course,” Beverly Hills, California |

Thank you to the Milken Institute for the opportunity to join you today. This morning I’d like to outline my view of current economic conditions and the economic outlook and then turn to the implications for monetary policy. In particular, with employment still well below its February 2020 peak, I will focus on how the escalation in inflation this year is testing the monetary policy framework adopted by the Federal Open Market Committee (FOMC) in August 2020.1

Outlook for Economic Growth

Recent data suggest that growth in the third quarter is likely to be lower than we had expected, but the foundations remain in place for strong economic growth over the remainder of this year and next. Employment is growing, financial conditions are accommodative, businesses are investing, and households, in the aggregate, have a large stock of savings to draw on for future spending. Weaker growth in payrolls in August and September, along with uneven consumer spending in July and August, appear to reflect ongoing concerns in some parts of the country about the spread of COVID-19, especially in high-contact service industries. Supply bottlenecks and labor shortages that have been more widespread and persistent than many expected are camouflaging continued strong underlying demand for goods, services, and workers. Supply constraints are particularly evident in interest-sensitive parts of the economy, such as residential investment and vehicle sales, limiting the scope for additional monetary accommodation to stimulate activity in those sectors.

I expect that these developments, however, have for the most part simply postponed activity temporarily and that robust growth will return in the coming months. There is evidence in recent weeks that we seem to be moving into a new phase of the economy. Nominal retail sales rose seven-tenths of 1 percent in September on the heels of a nine-tenths increase in August, an indication that consumers kept up their pace of spending. Robust business investment in equipment and intangibles continued in the second quarter, and indicators suggest another gain in the third quarter. Forward indicators of business spending and the need for firms to replenish depleted inventories point to strong investment into next year.

The Labor Market Continues to Strengthen

Without a doubt, the headline job gains in August and September were lower than expected, but, as I will show, based on almost every other major labor market indicator, there is ample evidence that the demand for labor is strong. At last measure, the Labor Department reported that job openings remained near a record high in August, and a record number of workers were voluntarily quitting their jobs, an indicator of their confidence in finding a better one. Other measures of job openings by education level indicate that jobs are plentiful even for less-skilled workers who have been affected the most by the COVID event. Another indicator I’ve been watching closely is the so-called U-6 unemployment rate, which consists of people who are working part time but prefer full-time work and discouraged workers who want a job but have given up looking. U-6 unemployment declined significantly over the past two months to 8.5 percent in September, roughly the same level as in the middle of 2017, when most everyone considered the job market to be quite healthy. In fact—and this will not be news to most of you—shortages of skilled workers in many occupations predated the COVID event and are likely to persist after its effects have faded. Some of this shortage reflects the aging of the workforce, changes in the types of jobs people want to do, and the time it takes to train workers.

Strong demand for labor is outpacing supply, and, naturally, that development is putting upward pressure on wages. Through September, average hourly wages are up 4.6 percent over the past 12 months, the largest and most sustained increase in wages for workers since the 1990s.

I noted the imbalance between the demand and supply for labor, and some of the labor market indicators that are still well short of pre-COVID levels are those related to labor force participation, which has been about unchanged this year on balance. I expect that as conditions normalize, this measure will pick up, but it is unlikely to return to its February 2020 level. One reason is that a disproportionate number of older workers responded to the initial shock of the COVID event by retiring, which may be an area where participation and employment struggle to retrace lost ground. Longer-lasting changes in labor force participation could make wage pressures more persistent and have implications for the assessment of maximum employment.

Tapering Asset Purchases

Since the middle of last year, the Fed has been increasing its holdings of Treasury securities and agency mortgage-backed securities by $120 billion a month to foster smooth market functioning and to support the economy by putting downward pressure on interest rates. Conditions had improved considerably by the time we announced our forward guidance for asset purchases in December, but the unemployment rate remained at 6.7 percent, near-term growth was being constrained by heightened social-distancing restrictions amid surging hospitalizations from COVID-19, and inflation was running significantly below 2 percent. As we sit here today, demand for labor is strong, and unemployment has declined to 4.8 percent. We have exceeded the previous high for real gross domestic product and are close to reaching the pre-COVID trend. Inflation, about which I will say more shortly, is running at more than twice the FOMC’s longer-run goal.

Taking all of the evidence into account, I think it is clear that we have met the test of substantial further progress toward both our employment and our inflation mandates, and I would support a decision at our November meeting to start reducing these purchases and complete that process by the middle of next year. Bear in mind that asset purchases are pressing down on the accelerator, adding each month to the amount of accommodation the Fed is providing to the economy through downward pressure on longer-term interest rates. Reducing purchases and ending them on this schedule is not monetary tightening, but a gradual reduction in the pace at which we are adding accommodation.

Monetary Policy When the Goals Are Not Complementary

A move to reduce the pace of asset purchases soon also is entirely consistent with the FOMC’s plan to pursue our longer-run maximum-employment and price-stability goals, and our new monetary policy strategy, which we refer to as our framework. The forward guidance that we put in place for asset purchases was an operationalization of the new framework. Last December, with inflation running well below 2 percent and unemployment still elevated, we committed to continue purchasing assets at least at the current pace until we had made substantial further progress toward our goals. In most situations, those goals are complementary. That is, high unemployment usually coincides with subdued inflationary pressures. Therefore, at the time, we did not foresee those goals coming into conflict.

But we are facing a situation now where inflation is high even though employment has yet to fully recover from the COVID event. In that case, according to the FOMC’s monetary policy framework, when objectives are not complementary, the Committee “takes into account the employment shortfalls and inflation deviations and the potentially different time horizons over which employment and inflation are projected to return to levels judged consistent with its mandate.”2

Applying those principles throughout 2021, we have been very patient and focused on the need for the labor market to recover as quickly as practicable from the severe damage experienced during the darkest days of the COVID event. We are remaining patient because, despite some periods of rapid progress, the recovery in jobs has been uneven and is still incomplete.

Early on, patience was easy: In December of last year, my FOMC colleagues and I were expecting much lower inflation—the median projection for 2021 by FOMC participants was 1.8 percent. The FOMC’s preferred inflation gauge did not crack 2 percent until March 2021. But, by June, prices had risen 4 percent over the previous 12 months, ticked up to 4.2 percent in July, and increased further to 4.3 percent in August. The median of the most recent projections by FOMC participants traces a path in which inflation ends the year just a touch lower than the current level. Nonetheless, I do not see the FOMC as behind the curve, for three reasons: Most of the biggest drivers of the very high current inflation rates will ease in coming quarters, some measures of underlying inflation pressures are less worrisome, and longer-term inflation expectations are anchored, at least for now.

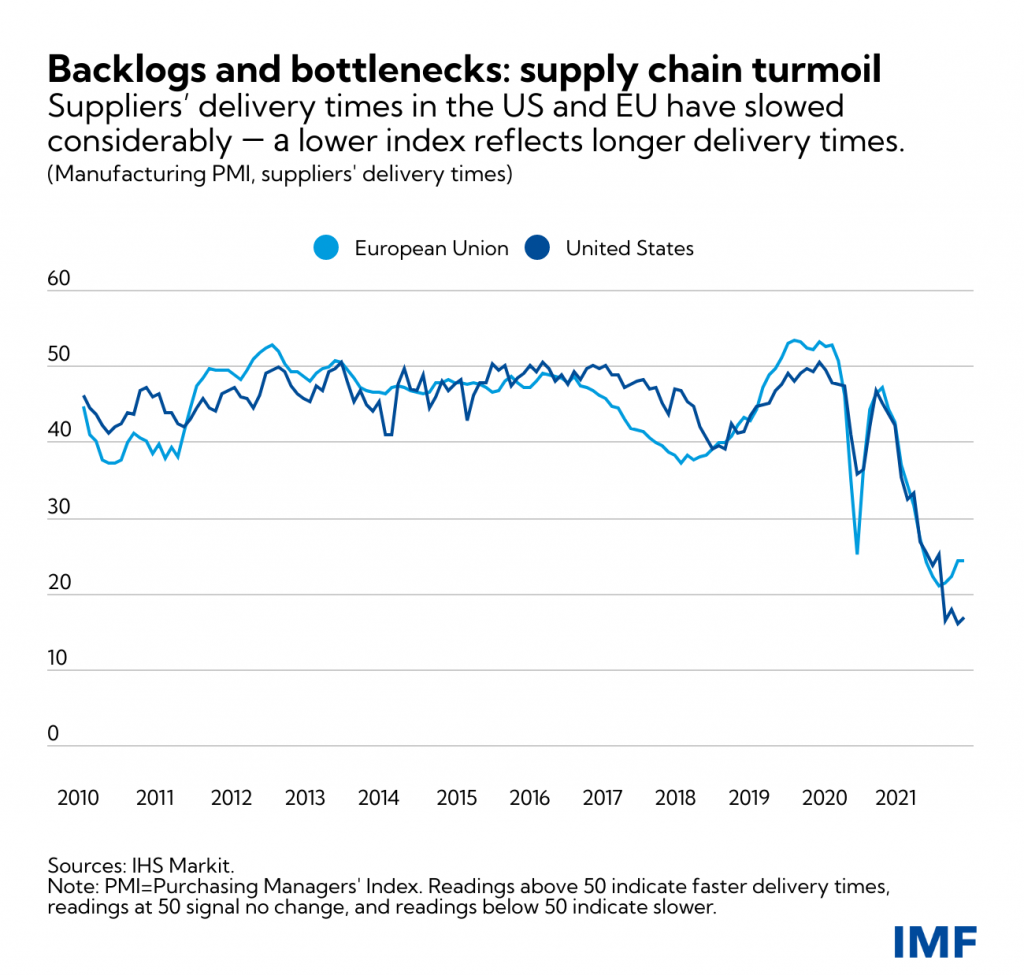

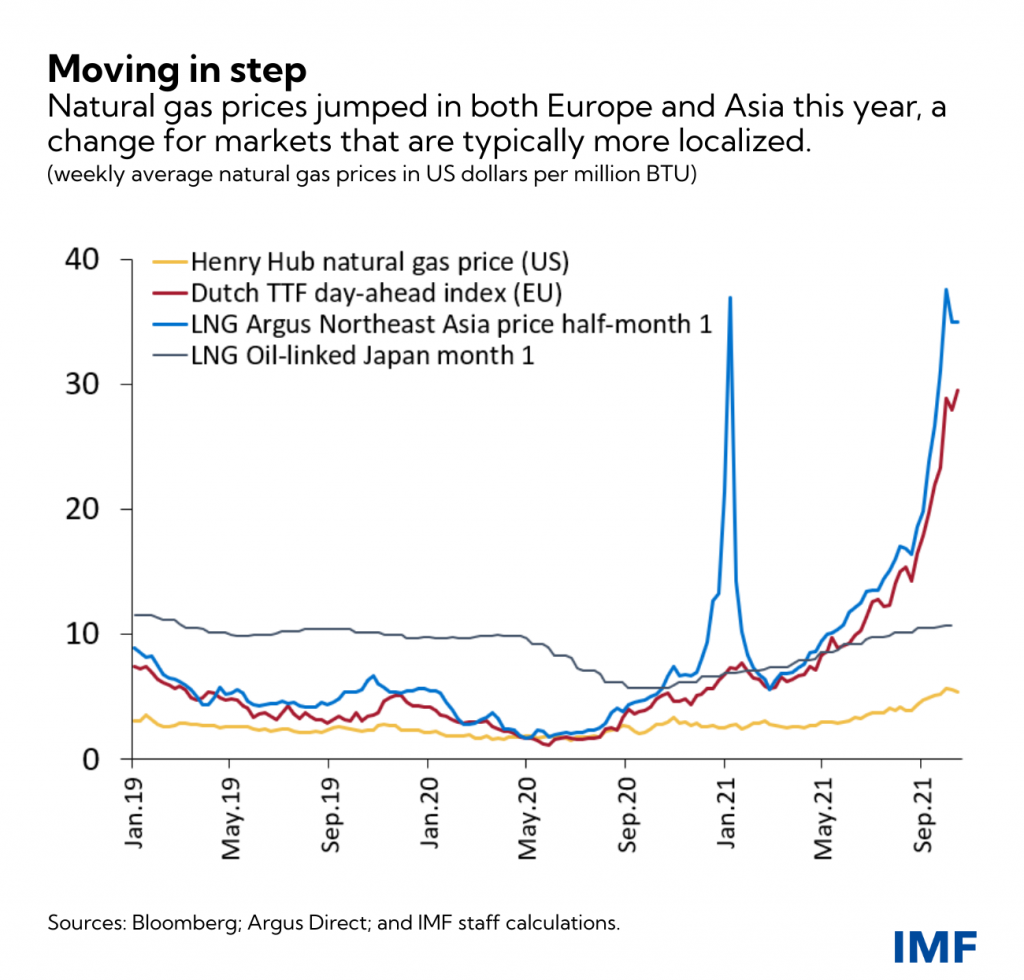

First, let me address the big drivers of this year’s price increases. The inflation we have experienced so far has been very unusual and largely related to supply constraints associated both with production and distribution problems related to COVID and with a demand shock arising from the unprecedented and rapid reopening of the economy. We all saw the remarkable price increases and shortages in the used car market. There have been a few other very specific and identifiable supply problems that have driven some other prices to very high levels—the semiconductor shortages that led to auto production slowdowns, for example, and, in some cases, labor shortages or restrictions related to the COVID event were associated with trade disruptions.

Second, if we recognize that much of the excessive inflation we are seeing this year is directly attributable to disruptions that, like the COVID event, will end, then monetary policy often can look through those types of disruptions to consider what inflation will be in the future when this episode passes. To get a fix on where inflation is headed, it is helpful to consider measures of inflation that try to filter out the most unusual and presumably transitory price increases that may be driving headline inflation. The Federal Reserve Bank of Dallas’s trimmed mean measure of inflation systematically removes prices that are increasing or decreasing at abnormally large rates, in order to get some perspective on underlying inflation pressures. For the 12 months through August, the Dallas trimmed mean inflation was an even 2 percent. Of course, while this metric may provide a better indicator of future PCE (personal consumption expenditures) inflation, I do not mean to suggest that this is necessarily a better reading on current inflation—consumers and businesses have to pay for the goods whose prices have risen sharply, and those increases are being felt.

That brings us to the third reason that I do not think the FOMC is behind the curve: anchored inflation expectations. We monitor longer-term expectations of future inflation because we believe they influence changes in actual inflation over the medium term. In fact, our new framework recognizes that stable, well-anchored inflation expectations help return inflation to 2 percent when it is running high, as it is now, as well as when it has fallen somewhat below that goal, as it often does during a recession.

So far, market-based measures of longer-term inflation expectations, as well as surveys of professional forecasters, have increased only moderately this year, moves that more or less reversed declines in those expectations over the previous half-dozen years. Measuring expectations is an inexact science, but smoothing through the ups and downs in expectations in recent years leaves these indicators within a range that has been consistent with inflation near our 2 percent goal.

How Long is Too Long?

Going forward, the question is not only whether inflation will fall in the coming months, but also how far it will fall and if it will fall soon enough to avoid spurring a concerning rise in longer-term inflation expectations. I agree with my FOMC colleagues and most private forecasters that inflation likely will decline considerably next year from its currently very elevated rate. For instance, most of the September Summary of Economic Projections forecasts for PCE inflation in 2022 were between 1.9 and 2.3 percent, with a minimum of 1.7 percent and a maximum of 3.0 percent.3 But I see significant upside risks to my current inflation outlook. Supply constraints in production and distribution already have become more widespread and have lasted longer than most forecasters anticipated. As noted earlier, labor supply constraints are making it difficult for businesses to keep up with demand. This dynamic will continue to support robust wage growth, putting further upward pressure on prices. Moreover, there is evidence in the past couple of months that a broader range of prices are beginning to increase at moderate rates, and I am closely watching those developments.

The fundamental dilemma that we face at the Fed right now is this: Demand, augmented by unprecedented fiscal stimulus, has been outstripping a temporarily disrupted supply, leading to high inflation. But the fundamental productive capacity of our economy as it existed just before COVID—and, thus, the ability to satisfy that demand without inflation—remains largely as it was, and the factors that are disrupting it appear to be transitory. Looked at purely in that light, constraining demand now, to bring it into line with a transiently interrupted supply, would be premature. Given the lags with which monetary policy acts, we could easily find that demand is damping just as supply is increasing, leading us to undershoot our inflation target—and, in the worst case, we could depress the incentives for supply to return, leading to an extended period of sluggish activity and unnecessarily low employment.

But “transitory” does not necessarily mean “short lived.” Indeed, we are discovering that it’s going to take more time than we had thought for supply to return to normal, and with demand already high during that time, I am monitoring the extent to which it could be further boosted by the additional fiscal programs currently under discussion. If those dynamics should lead this “transitory” inflation to continue too long, it could affect the planning of households and businesses and unanchor their inflation expectations. This could spark a wage-price spiral that would not settle down even when the logistical bottlenecks and supply chain kinks have eased. So the central question we have to answer is “How long is too long?”

I am among those who see a good chance that inflation will remain above 2 percent next year, but I am not quite ready to conclude that this “transitory” period is already “too long.” We haven’t yet met the more stringent tests for liftoff that we have laid out in forward guidance about the federal funds rate. Let me quote from the latest FOMC statement: Raising rates will not be appropriate “until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.”4 Importantly, the level of uncertainty around the paths for inflation and employment are higher than normal as we navigate the unprecedented reopening of the world economy. Therefore, we will remain outcome based, waiting to see further improvements in employment and the evolution of inflation pressures in coming months. And, if the broadly held expectation that inflation will recede next year turns out to be wrong or if inflation expectations show signs of becoming unanchored to the upside, I am confident that the monetary policy tools at our disposal can bring inflation down toward our 2 percent goal.

How High Is Too High?

I said just now that the central question is “How long is too long?” I am also keenly aware, however, that inflation of 4 percent or more certainly cannot be characterized as only “moderately” above 2 percent, and thus we also have to deal with the question of “How high is too high?” Moreover, the two questions are obviously related: we can tolerate inflation of 2.5 percent as supply returns to normal without dramatically affecting inflation expectations, for a much longer period than we can tolerate inflation of 4.5 percent. So, how high is too high? I cannot speak for my FOMC colleagues on this issue, but I will conclude with some thoughts of my own.

In 2012, the FOMC formally adopted a longer-run inflation target of 2 percent, and since then, that target has been reaffirmed annually by the Committee including in our new framework adopted in August 2020.5 The key innovations in the new framework relative to the previous incarnation are designed primarily to address the risk that inflation and inflation expectations could settle below our 2 percent target. That risk emanates from the understanding that several longer-run changes in the U.S. economy may have conspired to reduce the level of the equilibrium federal funds rate—the level at which it is neither slowing nor speeding up economic activity. In turn, a lower average level of interest rates would make it more difficult, on balance, for the Federal Reserve to respond to negative shocks to the economy with sizable cuts to interest rates. The inability to cut interest rates sufficiently can then reinforce downward pressures on inflation such that it begins to run persistently below the FOMC’s 2 percent goal and causes inflation expectations to fall with it.

As is well known by now, those revisions to the Fed’s monetary policy framework put new emphasis on reaching maximum employment and introduced new flexibility in how to account for progress toward our price-stability goal by seeking inflation that averages 2 percent over time to ensure longer-term inflation expectations remain anchored at this level. This revision implies that monetary policy will provide more support for economic activity over a typical business cycle than had been the case, in order to prevent longer-term inflation expectations—and, ultimately, inflation itself—from settling below 2 percent.

In this low interest rate environment, some researchers have suggested going further than our current framework does in allowing inflation to run moderately above 2 percent for some time following periods where it has run persistently lower than 2 percent, and actually raising the inflation target to 2.5 percent or 3 percent or even 4 percent.6 At the outset of our recently completed review, we reaffirmed that inflation at a rate of 2 percent is most consistent over the longer run with our congressional mandate for price stability.7 I believe that any future discussion of a higher target would need to address whether it remained consistent with that congressional mandate. I would also emphasize that at this point, the public is very accustomed to a world of inflation near 2 percent, which has allowed households and businesses to operate with considerable certainty. Research shows that such certainty is valuable for households and businesses to make sound financial decisions and to avoid economic distortions that could hinder economic growth.8

My strong support for our consensus framework is predicated not only upon its new features designed to address inflation that falls too low, but also its commitment to prevent longer-term inflation expectations from rising materially above a level consistent with our 2 percent goal. In this sense, the current elevated rates of inflation are not challenging our new framework any more than they would have challenged our previous framework or, for that matter, most reasonable frameworks for conducting monetary policy. As I said earlier, when our price-stability and employment goals are not complementary, the framework calls for policy to depend on the remaining shortfall from our maximum-employment goal, on the extent to which inflation continues to exceed 2 percent, and on the amount of time we expect it will take for employment and inflation to meet our goals.

I remain quite optimistic about the capacity and willingness of consumers and businesses to power a robust expansion as we put the COVID event behind us, even with the headwinds coming from the supply side. But that forecast for growth and uncertainty about the resolution of supply constraints mean that there are upside risks to inflation next year. So my focus is beginning to turn more fully from the rapidly improving labor market to whether inflation begins its descent toward levels that are more consistent with our price-stability mandate, as most forecasters and most of my colleagues on the FOMC expect over the next year. I would also be quite wary of further increases in inflation expectations in this environment. If inflation does remain more than moderately above 2 percent, be assured that the FOMC has the framework and the tools to address it.

Compliments of the U.S. Federal Reserve.

The post U.S FED | How Long is Too Long? How High is Too High?: Managing Recent Inflation Developments within the FOMC’s Monetary Policy Framework first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.