The Federal Reserve Board on Thursday released a discussion paper that examines the pros and cons of a potential U.S. central bank digital currency, or CBDC. It invites comment from the public and is the first step in a discussion of whether and how a CBDC could improve the safe and effective domestic payments system. The paper does not favor any policy outcome.

“We look forward to engaging with the public, elected representatives, and a broad range of stakeholders as we examine the positives and negatives of a central bank digital currency in the United States,” Federal Reserve Chair Jerome H. Powell said.

The paper summarizes the current state of the domestic payments system and discusses the different types of digital payment methods and assets that have emerged in recent years, including stablecoins and other cryptocurrencies. It concludes by examining the potential benefits and risks of a CBDC, and identifies specific policy considerations.

Consumers and businesses have long held and transferred money in digital forms, via bank accounts, online transactions, or payment apps. The forms of money used in those transactions are liabilities of private entities, such as commercial banks. Conversely, a CBDC would be a liability of a central bank, like the Federal Reserve.

While a CBDC could provide a safe, digital payment option for households and businesses as the payments system continues to evolve, and may result in faster payment options between countries, there may also be downsides. They include how to ensure a CBDC would preserve monetary and financial stability as well as complement existing means of payment. Other key policy considerations include how to preserve the privacy of citizens and maintain the ability to combat illicit finance. The paper discusses these and other factors in more detail.

To fully evaluate a potential CBDC, the Board’s paper asks for public comment on more than 20 questions. Comments will be accepted for 120 days and can be submitted here.

Contact:

For media inquiries, please email media@frb.gov or call 202-452-2955

Compliments of the U.S. Federal Reserve Board.

The post Federal Reserve Board releases discussion paper that examines pros and cons of a potential U.S. central bank digital currency (CBDC) first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.

Inflation will remain high at the start of 2022 but will fall later on, especially towards the end of the year, Chief Economist Philip R. Lane tells Verslo žinios. Our current projections foresee inflation below the 2% target in 2023 and 2024.

I just read the news this morning that the latest Purchasing Managers’ Index published this Monday shows that the eurozone economic recovery weakened further in January. This is due to the new restrictions imposed to contain the Omicron variant of the coronavirus (COVID-19). So what is your opinion on the state of the eurozone today, after two years of the pandemic and what are the prospects?

In the near term, there are some risks from the Omicron variant. But I think it’s increasingly clear that the impact is only for a few weeks. So it is not turning out to be a factor that will influence the activity levels for the year, it’s more the activity levels for a few weeks. In that sense, I think there’s less concern about Omicron than we had in December. In terms of the overall pandemic, I think it is fair to say that the recovery so far has been stronger than expected − compared to, for example, early 2020 when the pandemic hit. In the initial months of the pandemic there was a lot of concern. But essentially, when the vaccines have been rolled out during 2021, it turned out that the euro area economy and the world economy has recovered more quickly than expected. And looking to this year, 2022, we expect another strong year of recovery. So essentially, there’s been a strong recovery, supported by a lot of policy measures, both fiscal policy and monetary policy. I think in overall terms the sense is that, between the public health measures and other measures, it’s turning out that we can hope that the euro area can recover quite well from the pandemic.

Let’s go to the start of the pandemic. The euro area economy as a whole shrank more than 6 per cent in 2020. However, Ireland’s economy grew 3.4 per cent. And the Lithuanian economy escaped the recession too. To your mind, why did the Lithuanian economy and the Irish economy manage to decouple from the recessionary trends in the euro area last year?

What I think is that some sectors in the world economy were able to continue during the pandemic. So in those sectors where the pandemic might cause an interruption for a few months, even during 2020 it turned out there was a good recovery. The sectors where Lithuania is a big producer and the sectors where Ireland is a big producer, including a lot of multinational firms, turned out to be quite strong. But I would say both in Ireland and in Lithuania many sectors suffered. The fact that in overall terms, these economies did grow, should not take away from the fact that many service-type industries would have been damaged by the pandemic.

Euro area inflation hit a record high of 5 per cent in December of last year. Are you worried about further rising inflation in the eurozone?

We should think about these years of the pandemic, 2020, 2021 and 2022 as part of a pandemic cycle. In the first year 2020, inflation was relatively low. In the second half of 2021, inflation turned out to be quite high. And then, as we look into this year, 2022, we think inflation will remain high at the start of this year, but will fall later this year, especially towards the end of the year. So it’s a year, essentially, where in the first part of the year, we’ll still see inflation remaining high. But we do expect it to fall quite a bit later this year.

Do you expect inflation to rise further than 5 per cent at the start of the year? And what levels do you expect at the end of the year?

We are clear from our December forecast that we expect inflation − in overall terms for this year − to be around 3.2 per cent in the euro area, and then to be below 2 per cent in 2023 and 2024. Compared with the peak, that’s quite a big decline. We will see exactly the timing of how quickly inflation falls. So rather than focus on month by month, we have a clear vision in terms of the overall direction: that the inflation rate will fall later this year. And in fact, as you know, our current view from December is that inflation will fall below the 2 per cent target in the next couple of years.

What ECB monetary policy adjustments do you expect in the face of rising energy goods and services prices if the rise is higher than your forecasts?

I think we are always clear that we’re guided by our intentions to deliver an inflation rate of 2 per cent over the medium term. So we will adjust all of our policies − whether that’s asset purchases, the targeted lending programme, our interest rates − to deliver that goal. You’ve given me a hypothetical, the hypothetical is: what happens if inflation is above our forecast. So let me in turn make clear that what is very important is whether inflation will essentially settle at around our target of 2 per cent, which would be essentially what we want, or whether there might be signs of inflation being above 2 per cent in a significant way for a significant amount of time. And if we saw the data coming in to suggest that inflation would be too high relative to 2 per cent, then of course we would respond. We also have been clear on our sequence. The first decision under that scenario would be to end net purchasing. And only after ending net asset purchases would we look at the criteria for raising the interest rates. So we will be driven by the data, driven by our assessment. And every month, every quarter, we’re going to learn more about where the data are going.

Is there a risk of inflationary second round effects such as salary growth?

We spend a lot of time looking at the interlinkages. One linkage is that an increase in the cost of living may be a factor in wage negotiations. We think that is clear. The question is how much, because, remember, energy is both a direct cost to the consumer, but also a cost to other firms. Rising energy prices can also mean rising food prices, rising prices of goods and services. We are also examining how much the increase in energy prices might show up in rising goods prices and services prices. So far, we do not see a big response of wages. We do expect a response of wages but what is critical is how big. Because, remember, in the euro area, for inflation to be around 2 per cent and allowing for a typical increase in labour productivity of about 1 per cent, then wages should be growing around 3 per cent a year in the euro area on average to be consistent with the 2 per cent target. We are not, right now, seeing wage increases in that zone. But of course, we will continue to look at this throughout the year.

Some of your colleagues have mentioned another risk. Do you see any pressure to the rise of inflation in the euro area due to the green energy investments?

I think this is a complicated issue. Let me also emphasise that what we have right now is an increase in global energy prices. The euro area imports energy from the rest of the world. So this is a very different scenario from a scenario, which we would expect to occur in the coming years. Which is essentially, if there’s, for example, policies that increase the price of carbon, as part of the transition away from a high-carbon economy. If we see an increase in the price of carbon because of taxes or regulation, driven by domestic policy, those revenues from a carbon tax, for example, can be recycled in the domestic economy and can stimulate the economy. Wheras what we have right now is different. We have an increase in import prices from the rest of the world. And this is reducing living standards, increasing the import bill. It has a negative channel to lower incomes, lower consumption. So I think it’s a very interesting, very important debate about the future of green energy policies. That is playing some role right now. But the main role right now is a global issue, rather than the transition. So we will return to this topic, no doubt.

So overall, what scenarios do you see where interest rates in the eurozone could be lifted?

Let me mention three scenarios. And again, to repeat, we’re examining hypotheticals here. One scenario is in fact that the forces that generated low inflation before the pandemic essentially become visible again after the pandemic. So one scenario is that the world economy will return to quite low inflation rates. A second scenario is that some of these headwinds will not return and, in fact, it may be easier for us to deliver our target of 2 per cent. So that is a kind of middle scenario where inflation will stabilise at 2 per cent. And then the third scenario is, if inflation picks up and there is a risk that inflation will be significantly above 2 per cent. In this third scenario, where inflation is significantly above 2 per cent on a persistent basis, then that will call for a monetary policy tightening. We would have to respond. In the middle scenario where inflation stabilises at 2 per cent, then clearly over time we would normalise monetary policy. The policies we need to fight very low inflation would no longer be needed if inflation were stable around 2 per cent. And in the first scenario where inflation is significantly below 2 per cent, then the policies that we have employed to fight low inflation would still remain relevant. So this is the way I think about the world, but there are three scenarios. One, we remain with a low inflation problem. Two, we stabilise — in a kind of smooth way — inflation around 2 per cent. And three, if inflation turns out to be persistently above 2 per cent, we would have to tighten. And so those are three very different scenarios.

Which of these three scenarios do you see as the most likely scenario in this economic environment?

In the December round of projections, the assessment was that, in fact, we saw inflation returning to below 2 per cent. But we also emphasised that in a world of uncertainty, as we have more data come in, of course the data can change. But in the euro area context, I would say that it’s also possible that we may enter a world where inflation stabilises around 2 per cent. I find it less likely to think about a scenario where inflation is persistently, significantly above 2 per cent, which would require a serious tightening. That scenario, would, I think, in the context of the euro area, be less likely than the other two scenarios.

Higher sovereign borrowing costs after the financial crisis of 2007-09 turned into a eurozone debt crisis in 2010-13 that hit some southern European Member States, also Ireland. Debt levels have significantly risen during the pandemic. Is there any risk of another debt crisis this time provided interest rates will rise?

Let me make two important points here. One, at that time, there was a significant combination which, by and large, countries had of both high private sector debt – many households, many firms were highly indebted – and there was high government debt. That is a major problem. What we’ve seen in this pandemic is: yes, governments have borrowed more, and some types of firms have borrowed more. But households have been saving a lot. In the banking sector, we also have banks which are better able to handle debt, because they have increased their capital positions. So, when you have a situation where, essentially, in the euro area, debt levels have gone up for the sovereign and for some corporates but have gone down for households, and where the banks, that are kind of in the middle of the system, are in better shape, then I think it’s a different scenario to ten years ago. And then the other issue is: we think the trend level of interest rates is lower today than ten years ago. So, when interest rates go up, it’s from a very low level. And that’s important.

Finally, I have one question as to the elephant in the room: the deteriorating geopolitical situation in Ukraine these days due to the possible Russian military offensive. Do you see any side effects to the ECB monetary policy, should the geopolitical situation in Europe deteriorate further?

Geopolitics always matters. I think if you look at the history of the world economy, the European economy, geopolitical events matter a lot via trade, via global prices, via uncertainty. So, of course, we will be looking very closely at such factors. We already talked about the very high energy prices. And of course, there’s a connection between higher energy prices and these tensions. So of course, it’s very directly relevant for us.

Compliments of the European Central Bank.

The post ECB Interview | Inflation expected to decline over 2022 first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.

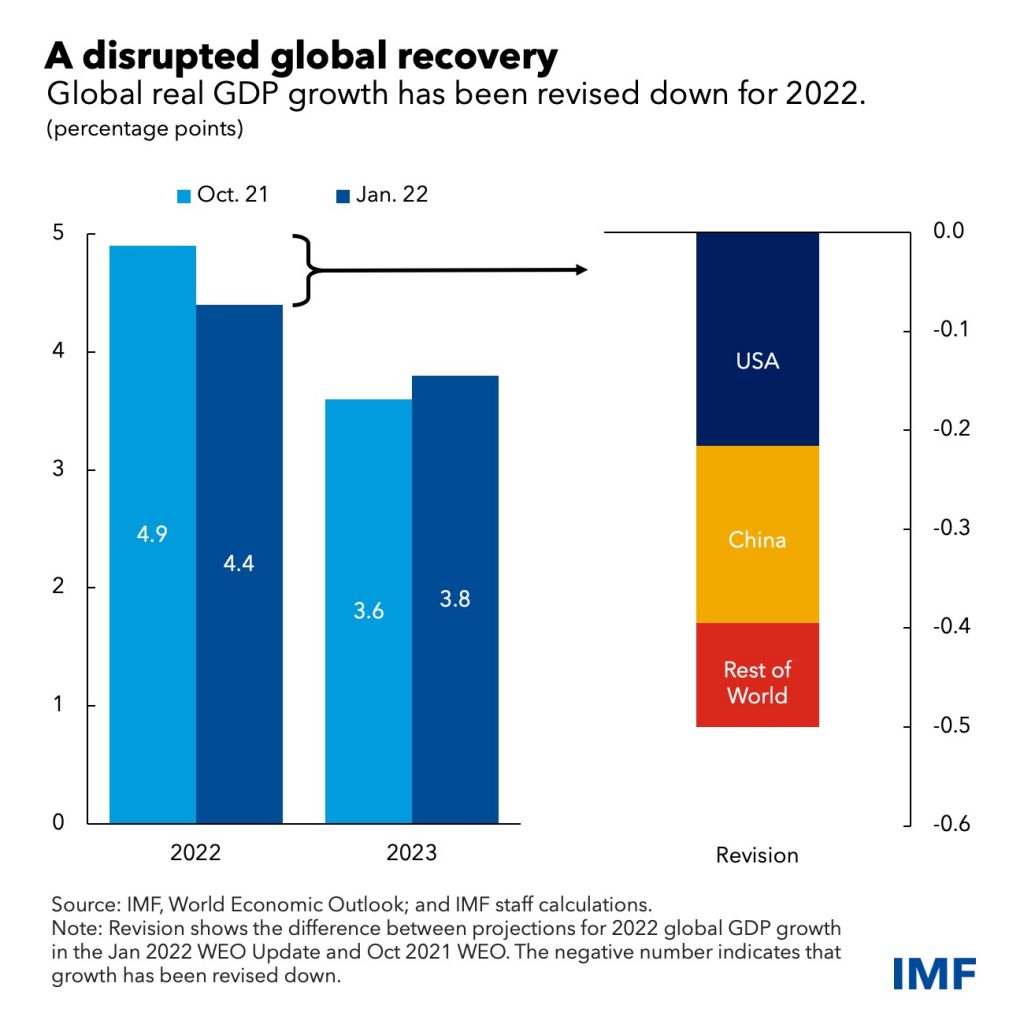

Growth slows as economies grapple with supply disruptions, higher inflation, record debt and persistent uncertainty.

The continuing global recovery faces multiple challenges as the pandemic enters its third year. The rapid spread of the Omicron variant has led to renewed mobility restrictions in many countries and increased labor shortages. Supply disruptions still weigh on activity and are contributing to higher inflation, adding to pressures from strong demand and elevated food and energy prices. Moreover, record debt and rising inflation constrain the ability of many countries to address renewed disruptions.

Some challenges, however, could be shorter lived than others. The new variant appears to be associated with less severe illness than the Delta variant, and the record surge in infections is expected to decline relatively quickly. The IMF’s latest World Economic Outlook therefore anticipates that while Omicron will weigh on activity in the first quarter of 2022, this effect will fade starting in the second quarter.

Other challenges, and policy pivots, are expected to have a greater impact on the outlook. We project global growth this year at 4.4 percent, 0.5 percentage point lower than previously forecast, mainly because of downgrades for the United States and China. In the case of the United States, this reflects lower prospects of legislating the Build Back Better fiscal package, an earlier withdrawal of extraordinary monetary accommodation, and continued supply disruptions. China’s downgrade reflects continued retrenchment of the real estate sector and a weaker-than-expected recovery in private consumption. Supply disruptions have led to markdowns for other countries too, such as Germany. We expect global growth to slow to 3.8 percent in 2023. This is 0.2 percentage point higher than in the October 2021 WEO and largely reflects a pickup after current drags on growth dissipate.

We have revised up our 2022 inflation forecasts for both advanced and emerging market and developing economies, with elevated price pressures expected to persist for longer. Supply-demand imbalances are assumed to decline over 2022 based on industry expectations of improved supply, as demand gradually rebalances from goods to services, and extraordinary policy support is withdrawn. Moreover, energy and food prices are expected to grow at more moderate rates in 2022 according to futures markets. Assuming inflation expectations remain anchored, inflation is therefore expected to subside in 2023.

Even as recoveries continue, the troubling divergence in prospects across countries persists. While advanced economies are projected to return to pre-pandemic trend this year, several emerging markets and developing economies are projected to have sizeable output losses into the medium-term. The number of people living in extreme poverty is estimated to have been around 70 million higher than pre-pandemic trends in 2021, setting back the progress in poverty reduction by several years.

The forecast is subject to high uncertainty and risks overall are to the downside. The emergence of deadlier variants could prolong the crisis. China’s zero-COVID strategy could exacerbate global supply disruptions, and if financial stress in the country’s real estate sector spreads to the broader economy the ramifications would be felt widely. Higher inflation surprises in the United States could elicit aggressive monetary tightening by the Federal Reserve and sharply tighten global financial conditions. Rising geopolitical tensions and social unrest also pose risks to the outlook.

‘To address many of the difficulties facing the world economy, it is vital to break the hold of the pandemic.’

Global Efforts

To address many of the difficulties facing the world economy, it is vital to break the hold of the pandemic. This will require a global effort to ensure widespread vaccination, testing, and access to therapeutics, including the newly developed anti-viral medications. As of now, only 4 percent of the population of low-income countries are fully vaccinated versus 70 percent in high-income countries. In addition to ensuring predictable supply of vaccines for low-income developing countries, assistance should be provided to boost absorptive capacity and improve health infrastructure. It is urgent to close the $23.4 billion financing gap for the Access to COVID-19 Tools (ACT) Accelerator and to incentivize technological transfers to help speed up diversification of global production of critical medical tools, especially in Africa.

At the national level, policies should remain tailored to country specific circumstances including the extent of recovery, of underlying inflationary pressures, and available policy space. Both fiscal and monetary policies will need to work in tandem to achieve economic goals. Given the high level of uncertainty, policies must also remain agile and adapt to incoming economic data.

With policy space diminished in many economies, and strong recoveries underway in others, fiscal deficits in most countries are projected to shrink this year. The fiscal priority should continue to be the health sector, and transfers, where needed, should be effectively targeted to the worst affected. All initiatives will need to be embedded in medium-term fiscal frameworks that lay out a credible path for ensuring public debt remains sustainable.

Monetary policy is at a critical juncture in most countries. Where inflation is broad based alongside a strong recovery, like in the United States, or high inflation runs the risk of becoming entrenched, as in some emerging market and developing economies and advanced economies, extraordinary monetary policy support should be withdrawn. Several central banks have already begun raising interest rates to get ahead of price pressures. It is key to communicate well the policy transition towards a tightening stance to ensure orderly market reaction. Where core inflationary pressures remain subdued, and recoveries incomplete, monetary policy can remain accommodative.

As the monetary policy stance tightens more broadly this year, economies will need to adapt to a global environment of higher interest rates. Emerging market and developing economies with large foreign currency borrowing and external financing needs should prepare for possible turbulence in financial markets by extending debt maturities as feasible and containing currency mismatches. Exchange rate flexibility can help with needed macroeconomic adjustment. In some cases, foreign exchange intervention and temporary capital flow management measures may be needed to provide monetary policy with the space to focus on domestic conditions.

With interest rates rising, low-income countries, of which 60 percent are already in or at high risk of debt distress, will find it increasingly difficult to service their debts. The G20 Common Framework needs to be revamped to deliver more quickly on debt restructuring, and G20 creditors and private creditors should suspend debt service while the restructurings are being negotiated.

At the start of the third year of the pandemic, the global death toll has risen to 5.5 million deaths and the accompanying economic losses are expected to be close to $13.8 trillion through 2024 relative to pre-pandemic forecasts. These numbers would have been much worse had it not been for the extraordinary work of scientists, of the medical community, and the swift and aggressive policy responses across the world.

However, much work remains to ensure the losses are contained and to reduce wide disparities in recovery prospects across countries. Policy initiatives are needed to reverse the large learning losses suffered by children, especially in developing countries. On average, students in middle-income and low-income countries had 93 more days of nation-wide school closures than those in high income countries. On climate, a bigger push is needed to get to net-zero carbon emissions by 2050, with carbon pricing mechanisms, green infrastructure investment, research subsidies, and financing initiatives so that all countries can invest in climate change mitigation and adaptation measures.

The last two years reaffirm that this crisis and the ongoing recovery is like no other. Policymakers must vigilantly monitor a broad swath of incoming economic data, prepare for contingencies, and be ready to communicate and execute policy changes at short notice. In parallel, bold, and effective international cooperation should ensure that this is the year the world escapes the grip of the pandemic.

Author:

Gita Gopinath is the First Deputy Managing Director of the IMF.

Compliments of the IMF.

The post IMF | A Disrupted Global Recovery first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.

The Council approved conclusions today endorsing the new priorities for the 2022-2024 period under the UN-EU strategic partnership on peace operations and crisis management.

The Council reiterates the firm commitment made by the EU and its member states to uphold the multilateral rules-based global order with the United Nations at its core, and it commends the achievements and recognises the mutually beneficial nature of the longstanding UN-EU cooperation on peacekeeping and civilian, police and military crisis management.

The Council welcomes the extended scope of the priorities, which aim to respond more effectively to the evolving threat landscape and cross-cutting challenges such as climate change, disruptive technologies and misinformation, and the consequences of the global COVID-19 pandemic. Additionally, the Council welcomes the inclusion of the matter of children and armed conflict as a cross-cutting priority, as well as the increased attention to the Youth, Peace and Security agenda and the enhanced joint UN-EU efforts on the Women, Peace and Security agenda and gender equality.

The conclusions stress that partnering with the UN helps the EU play its role as a security provider and a global peace and security actor in support of effective multilateralism.

The EU provides the UN with political support as well as expertise, financial backing and political leverage to deliver on UN mandates. Close cooperation helps UN and EU missions and operations act more effectively to ensure they have an impact on the ground. It has a multiplier effect and enables the EU to deliver on its integrated approach.

Council Conclusions on taking the UN-EU strategic partnership on peace operations and crisis management to the next level: Priorities 2022-2024

Reinforcing the EU-UN Strategic Partnership on crisis management, EEAS website

The European Union at the United Nations – Factsheet

Compliments of the Council of the EU.

The post UN-EU strategic partnership on peace operations and crisis management: EU Council conclusions on priorities for 2022-2024 first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.

The European Commission has today disbursed €271 million to Finland in pre-financing, equivalent to 13% of the country’s financial allocation under the Recovery and Resilience Facility (RRF). The pre-financing payment will help kick-start the implementation of the crucial investment and reform measures outlined in Finland’s recovery and resilience plan.

The Commission will authorise further disbursements based on the implementation of the investments and reforms outlined in Finland’s recovery and resilience plan. The country is set to receive €2.1 billion in total, fully consisting of grants, over the lifetime of its plan.

Since June 2021, the Commission has raised €71 billion for NextGenerationEU via long-term EU Bonds – €12 billion of which through the first-ever NextGenerationEU green bond issuance. On 14 December, the Commission published its funding plan for the first semester of 2022. The plan foresees the issuance of €50 billion of long-term EU Bonds between January and June 2022, to be complemented by short-term EU-Bills. In addition, the Commission currently has around €20.5 billion in EU-Bills outstanding.

The RRF is at the heart of NextGenerationEU which will provide €800 billion (in current prices) to support investments and reforms across Member States. Finland’s plan is part of the unprecedented EU response to emerge stronger from the COVID-19 crisis, fostering the green and digital transitions and strengthening resilience and cohesion in our societies.

Supporting transformative investments and reform projects

The RRF in Finland finances investments and reforms that are expected to have a deeply transformative effect on Finland’s economy and society. Here are some of these projects:

Securing the green transition: Finland’s plan supports the green transition through investments of €319 million in decarbonisation of the energy sector, namely in energy transmission and distribution and in new energy technologies. €156 million will be invested in low-carbon hydrogen along the hydrogen value chain as well as in carbon capture, storage and recovery. The objective of the investments is to contribute to Finland’s goal to achieve carbon neutrality by 2035 by stimulating the introduction of new clean technologies for energy production and use.

Supporting the digital transition: The plan supports the digital transition with investments and reforms amounting to €50 million in high-speed broadband infrastructure across Finland. It increases the quality and availability of communication connections in areas where such connections are not provided based on market mechanisms alone. Digital innovations for social welfare and health care servicesare supported with €100 million.

Reinforcing economic and social resilience: The plan reinforces economic and social resilience by allocating €90 millionto the reform of the Public Employment Services to increase the employment rate. The plan invests €260 million in streamlining healthcare service processes and providing faster and more equal access to social and health services as well as to promote prevention and early identification of health issues.

Members of the College said:

President of the European Commission, Ursula von der Leyen, said: “This first disbursement under NextGenerationEU is great news for Finland and the Finnish people. This is European solidarity at its best, part of the €2.1 billion Finland will receive for its digital transition and helping the country to further prosper and grow while respecting the boundaries of our planet. Therefore the EU supports Finland’s investments in clean energy and decarbonising industry. We will stand by Finland in the years ahead to ensure that the plan delivers on its full potential.”

Johannes Hahn, Commissioner for Budget and Administration, said: “Our NextGenerationEU funds raised on the financial market continue to support the digital and green transition in EU Member States, as just now with the disbursement of the pre-financement to Finland. I am sure that the Finnish citizens, businesses and the society as a whole will profit from the transformative investments and projects.”

Paolo Gentiloni, Commissioner for Economy, said: “Today Finland receives €271 million in pre-financing for its recovery and resilience plan. The Finnish plan is strongly focused on the green transition, with no less than 50% of its total allocation set to support climate objectives. This will help to speed the country towards its ambitious target of carbon neutrality by 2035. The plan also contains an array of measures to boost Finland’s already strong digital competitiveness. I particularly welcome the Finnish plan’s strong social elements, with measures to raise the employment rate, tackle youth unemployment and facilitate access to social and healthcare services.”

Compliments of the European Commission.

The post NextGenerationEU: European Commission disburses €271 million in pre-financing to Finland first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.

Today, the EU is requesting consultations with Russia at the World Trade Organization (WTO) concerning export restrictions placed by Russia on wood products. The export restrictions consist of significantly increased export duties on certain wood products and a drastic reduction in the number of border crossing points through which exports of wood products can take place.

The Russian restrictions are highly detrimental to the EU wood processing industry, which relies on exports from Russia, and create significant uncertainty on the global wood market. The EU has repeatedly engaged with Russia since Moscow announced these measures in October 2020, without success. They entered into force in January 2022.

Specifically, the EU is challenging:

The increase of export duties on certain wood products:

At the WTO, Russia committed to applying export duties at rates of maximum 13% or 15% for certain quantities of exports. By withdrawing these tariff-rate quotas, Russia now applies export duties at a much higher rate of 80%, and thereby does not respect its commitments under WTO law.

The reduction of the number of border-crossing points for Russian exports of wood products into the EU:

Russia has reduced the number of border crossing points handling wood exports to the EU, from more than 30 to only one (Luttya, in Finland). By prohibiting the use of existing border crossing points that are technically capable of handling such exports, Russia is violating a WTO principle forbidding such restrictions.

Next steps

The dispute settlement consultations that the EU has requested are the first step in WTO dispute settlement proceedings.

If they do not lead to a satisfactory solution, the EU can request that the WTO set up a panel to rule on the matter.

For more information

WTO Dispute Settlement in a Nutshell

Compliments of the European Commission.

The post EU challenges Russian export restrictions on wood at WTO first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.

On the 22th of December, the European Commission (hereinafter: ‘EC’) has presented an initiative to combat the misuse of shell entities for improper tax purposes (‘ATAD 3’). This proposal will ensure that shell companies in the EU with no- or minimal economic activity are unable to benefit from any tax advantages, consequently discouraging their use. Furthermore, the Commission Ter Haar published a report on ‘doorstroomvennootschappen’ in the Netherlands last October.

Shell companies can be used for aggressive tax planning or tax evasion purposes. Businesses can direct financial ‘flows’ through these shell entities towards tax friendly jurisdictions. Similar with this, some individuals can use shell entities to shield assets – more specific real estate – from taxes, either in their respective home country or in the country where the property is located. The main purpose of this proposal is therefore to address the abusive use of so-called shell companies, being referred to as legal entities with no, or only minimal, substance and economic activity.

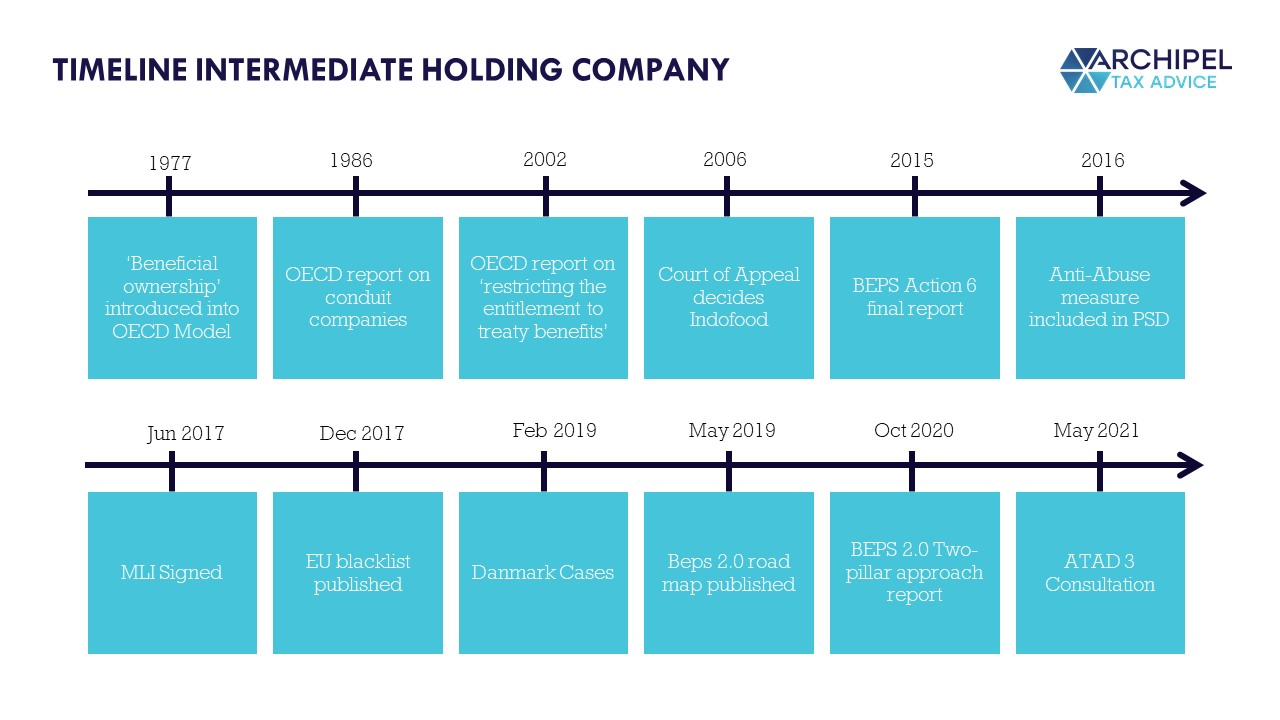

History intermediary holding companies

International groups often use intermediate holding companies to hold shares in subsidiaries organized on a regional or divisional basis. Furthermore, holding companies are often used as the vehicle for investing in portfolio companies in a private equity context. In past times, it was not particularly controversial that holding companies were entitled to the potential benefits of tax treaties and potential directives in their country of residence. This would frequently restrict the right of investee jurisdictions to tax dividends and gains derived by the holding company from its local subsidiaries. As shown in the timeline underneath, the perception and position of these companies has changed, with an accumulation of measures that potentially restrict the access to the benefits and directives.

This all started with the introduction of the term “beneficial ownership” into the OECD’s Model Tax Convention in 1977. The question was asked: who does actually benefit from this/these payment(s)? Whilst being slightly controversial in the 70’s, the term now appears in most tax treaties and intents to prevent treaty shopping by ensuring that the benefits of the dividends, royalties and interest articles are only accessible to residents of the contracting state that are the beneficial owners of the payment. After this, the OECD’s report on the use of conduit companies in 1986 ruled conduit companies out of the beneficial ownership regard. Nevertheless, there was no generally agreed definition of the term ‘beneficial ownership’ in tax treaties and the interpretation would follow the domestic law of the contracting states. The first hint of an international fiscal meaning of this term stems from the Indofood case (Indofood International Finance Ltd. V JP Morgan Chase Bank NA, 2006). To prevent falling foul of the beneficial ownership test, certain groups reviewed their holding structure(s) and looked to eliminate fully back-to-back financing arrangements. Furthermore, some structures which involved payment chains were set up with an “equity gap”. These structures reflected a widespread view that beneficial ownership was an objective test that was indifferent to the motives behind these holding company arrangements.

Whilst having a long history, reverting back to said changes in the OECD model treaty in the 70’s, the real challenge to the treaty status of holding companies began in 2015, when the Base Erosion and Profit Shifting project (‘BEPS’) recommended measures to restrict inappropriate usage of tax treaties. The bar is consequently set higher and higher for the criteria that holding companies need to meet in order to benefit from relief from withholding taxes and exemptions to non-resident capital gains tax. The high apex for this approach is the just published proposal to end the misuse of shell entities. Some of the statements suggest that it may never be appropriate for an intermediate holding company (using the term ‘shell entity’) to benefit from reductions in withholding taxes under tax treaties and EU directives.

Click on the image for a bigger version

The Dutch government already set up a commission that investigated the use of the so-called shell companies and their potential misuse of the Dutch tax system. This report was published last October.

Dutch investigation on shell companies (Commission Ter Haar)

‘Doorstroomvennootschappen’ (as they’re often referred to in Dutch) provide little benefit to the Dutch economy, disadvantage developing countries disproportionately through loss of tax revenue for developing countries in particular, and the phenomenon damages the reputation of the Netherlands. These are the main conclusions of the Committee on Flow-through Companies, chaired by Mr. Ter Haar, which presented its final report recently.

The committee describes the relevant components of the Dutch tax system that, at least until recently, have made the Netherlands attractive to flow-through companies. These include the participation exemption, the extensive treaty network, the absence of a withholding tax on interest and royalties and the ruling practice. The report describes examples of unintended use of each of these aspects of the Dutch tax system. In combination with the well-organized financial advice and services sector, this has led, according to the Committee, to a sizeable financial flow. The Committee believes that the measures already taken are expected to put an end to (part of) the tax-driven flow of interest and royalties. This does not mean that the Netherlands should be expected to lose its position as a country of establishment for empty holding companies, even though the Dutch tax system is no longer unique compared to other countries. According to the Committee there will still be a large group of (almost) empty conduits that make use of the Dutch tax infrastructure, whose contribution to the economy is small. The Committee therefore recommends further steps, but at the same time sees that far-reaching unilateral measures do not immediately offer a solution. In the first place, the Committee recommends a proactive attitude and a pioneering role with respect to international and European initiatives. These include the revision of the international tax system within the Inclusive Framework of the OECD and the announced EU Directive proposal on flow-through companies. According to the committee, the Netherlands should advocate measures that involve both the targeted exchange of information and to limit the benefits of the Interest and Royalties Directive and the Parent-Subsidiary Directive.

Click on the image for a bigger version

The advantage of this structure is that the dividends, by making use of the Dutch treaty network, without or with reduced withholding of local tax, arrive at the company in the country of residence (Country A), without or with reduced withholding of local tax, compared to the situation where the payment is made directly to the country of residence (Country A) by the source country (Country C). This is just one example of a (flow-through) structure in which the Dutch treaty network plays a role, in combination with the participation exemption and the dividend withholding tax exemption in treaty situations.

Because the Netherlands has long had a large bilateral tax treaty network, the Netherlands is an attractive country for ‘treaty shopping’. When the tax treaties are concluded, it is assumed that it is up to the source country to prevent the reduced rate of withholding tax, which is wrongly applied mostly.

Unilateral measures cannot prevent other countries from playing the role as flow through country. To avoid international tax avoidance through ‘empty entities’, international agreements are therefore necessary. The committee lastly advises also a constructive attitude by the Netherlands to the ongoing initiatives of the European Commission.

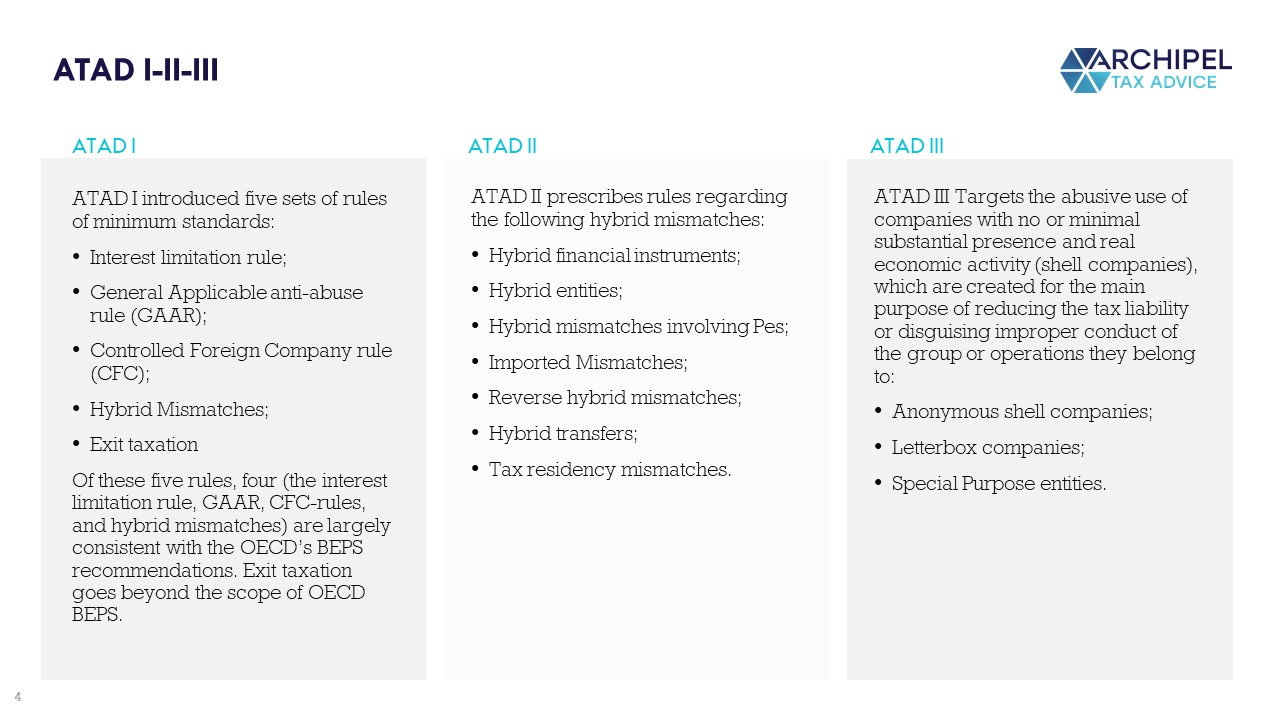

ATAD 1-2

The public perception of tax evasion has shifted in recent years, by taking a drastic turn. In particular, the credit crisis of 2008 has changed the social acceptance of tax avoidance by multinationals in particular. With government deficits and rising government debt, it was considered unfair that a number of multinationals paid (relatively) little tax on their world profits.

This all accumulated into a public hearing of officials of Amazon, Google and Starbucks organized by the Public Accounts Committee in the UK in 2012. The committee chair Ms. Hodge said (the later iconic words):

“We’re not accusing you of being illegal, we’re accusing you of being immoral”.

This all led to the BEPS-project and consequently ATAD. There have been 2 Anti-Tax-Avoidance-Directives already put into effect. ATAD 1 introduced 5 sets of minimum standards (interest limitation rule, GAAR, CFC rules, hybrid mismatches and exit taxation). In the second ATAD, subsequent rules relating to hybrid mismatches were finalized on 29 may 2017 when the ECOFIN accepted this directive. ATAD is based on Article 115 of the Treaty on the Functioning of the EU (‘TFEU’).

ATAD 3

Shell Companies

The definition of the widespread term ‘shell’, often interchangeably with terms such as ‘letterbox’, ‘mailbox’, ‘special purpose entity’, special purpose vehicle’ and similar, is defined differently in different contexts. For the purpose of ATAD 3, shell companies refer to three types of shell companies:

Anonymous shell companies

Letterbox companies

Special purpose entities

The main common feature of the above three types is the absence of real economic activity in the Member State of

registration, which usually means that these companies have no (or few) employees, and/or no (or little)

production, and/or no (or little) physical present in the Member State of registration

What will change?

The proposed rules will establish transparency standards around the use of shell entities, so that their abuse can be detected more easily by tax authorities. Using a number of objective indicators related to income, staff and premises, the proposal will help national tax authorities detect entities that exist merely on paper.

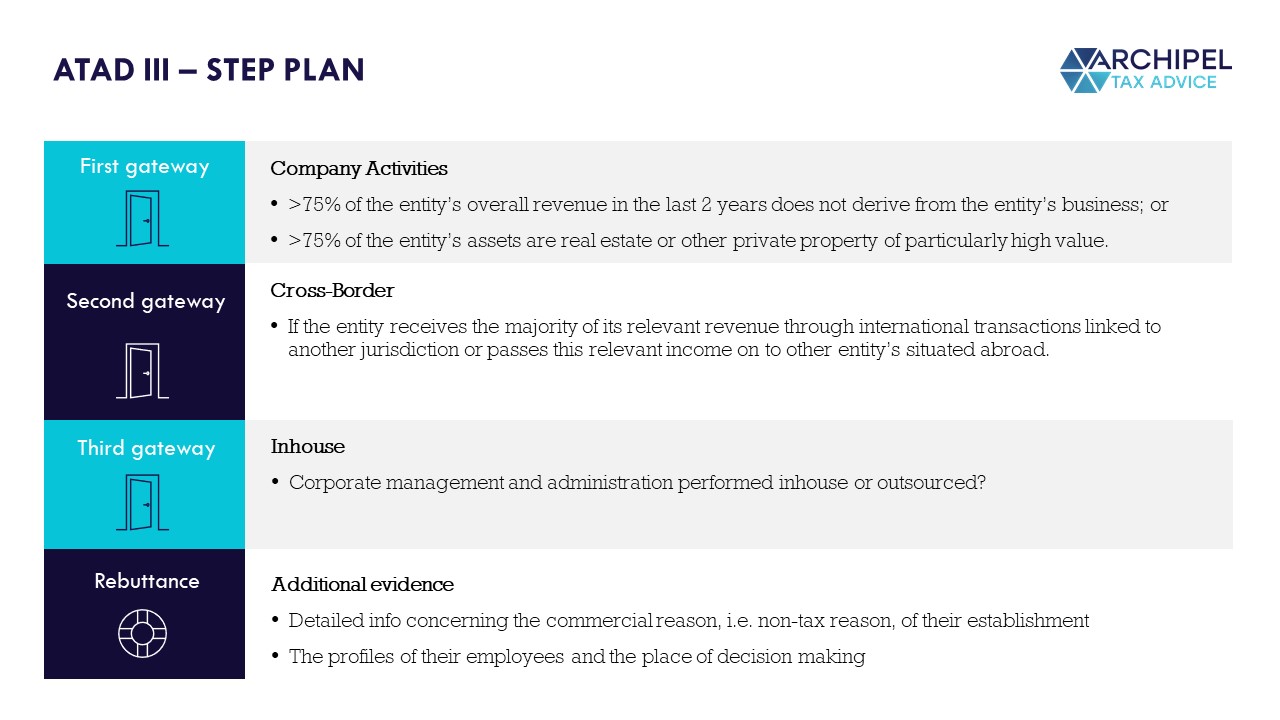

The proposal introduces a filtering system for the entities in scope, which have to comply with a number of indicators. These different levels constitute a type of gateway. This proposal sets out three gateways. If an entity crosses all three gateways, it will be required to annually report more information to the tax authorities through its tax return.

Click on the image for a bigger version

Gateways

First gateway

The first level looks at the activities of the companies based on the income they receive. This gateway is met if >75% of an entity’s overall revenue in the last two tax years does not derive from the entity’s business activity or if more than 75% of its assets are real estate or other private property of particularly high value.

Second gateway

The second level requires a cross-border element. If the entity receives the majority of its relevant revenue through international transactions linked to another jurisdiction or passes this relevant income on to other entity’s situated abroad, the entity passed to the next and last gateway.

Third gateway

The third, and last, level focuses on whether corporate management and administration services are performed in-house or are outsourced.

Crossed all gateways?

An entity crossing all levels will be obliged to report information in its tax return related to the premises of the entity, its bank accounts, the tax residency of its directors and employees etc. These are the so-called substance requirements. All declarations should be accompanied by supporting evidence. If one of the substance requirements isn’t met, the entity will be presumed to be a ‘shell company’.

When will the proposal come into force?

Once adopted by the Member States, the Directive should come into effect on 1 January 2024.

Rebuttal arrangement?

If the substance criteria are not met, entities still have the opportunity to rebut the presumption of being a shell. Additional evidence needs to be presented, such as detailed information about the commercial, non-tax reason of their establishment, the profiles of their employees and the fact that decision-making takes place in the Member State of their tax residence.

Click on the image for a bigger version

Tax Consequences

If an entity is deemed to be a shell company, the benefits and reliefs of the tax treaty network of its Member state are not applicable. Furthermore, the company will not be able to qualify for the treatment under the Parent-Subsidiary and Interest and Royalty Directives. To support the implementation of these consequences, the Member State of residence of the company will either deny the shell company a tax residence certificate or the certificate will specify that the company is a shell.

Furthermore, payments to third countries will not be treated as flowing through the shell entity, and will be subject to withholding tax at the level of the entity that paid to the shell. According with this, inbound payments will be taxed in the state of the shell’s shareholder. Relevant consequences will apply to shell companies owning real estate assets for the private us of wealthy individuals and which as a result have no income flows. Such real estate assets will be taxed by the state in which the asset is located as if it were owned directly by the individual.

Click on the image for a bigger version

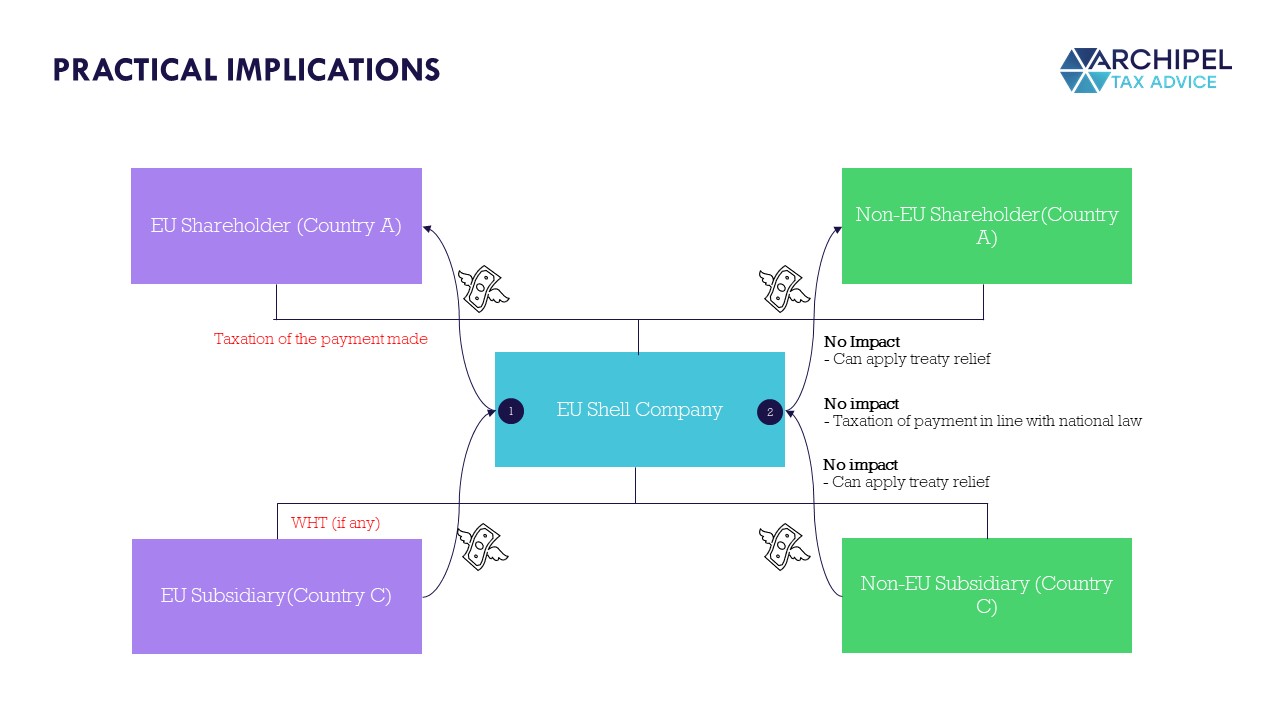

Scenario 1 EU source jurisdiction of the payer – EU shell jurisdiction – EU shareholder jurisdiction

In this case, all three jurisdictions fall in the scope of the Directive and are consequently bound by ATAD3:

EU subsidiary: this entity will not have a right to tax the payment, but may apply domestic tax on the outbound payment to the extent it cannot identify whether the undertaking’s shareholder is in the EU.

EU shell: this entity will continue to be a resident for tax purposes in the respective Member State and will have to fulfil relevant obligations as per national law, including by reporting the payment received; it may be able to provide evidence of the tax applied on the payment.

EU shareholder: this entity will include the payment received by the shell undertaking in its taxable income, as per the national law and may be able to claim relief for any tax paid at the source, including by virtue of EU directives. It will also take into account and deduct any tax paid by the shell.

Scenario 2 Non-EU source jurisdiction of the payer – EU shell jurisdiction – Non-EU shareholder jurisdiction

Third country subsidiary: may apply domestic tax on the outbound payment or can decide to apply tax according to the tax treaty in effect with the third jurisdiction of the shareholder if it wishes to look through the EU shell entity as well.

EU shell: will continue to be a resident for tax purposes in a Member State and fulfil relevant obligations as per national law, including by reporting the payment received; it may be able to provide evidence of the tax applied on the payment.

Third country shareholder: while the third country shareholder jurisdiction is not compelled to apply any consequences, it may consider applying a treaty in force with the source jurisdiction in order to provide relief.

Click on the image for a bigger version

Scenario 3 Non-EU source jurisdiction of the payer – EU shell jurisdiction – EU-shareholder jurisdiction

In this case the source jurisdiction is not bound by ATAD 3, while the jurisdictions of the shell and the shareholder fall in scope.

Third country source jurisdiction: this entity may apply domestic tax on the outbound payment or may decide to apply the treaty in effect with the EU shareholder jurisdiction.

EU shell: this entity will continue to be resident for tax purposes in the respective Member State and will have to fulfil relevant obligations as per national law, including by reporting the payment received; it may be able to provide evidence of the tax applied on the payment.

EU shareholder: this entity shall include the payment received by the shell undertaking in its taxable income, as per the national law and may be able to claim relief for any tax paid at source, in accordance with the applicable treaty with third country source jurisdiction. It will also take into account and deduct any tax paid by the shell.

Scenario 4 EU source jurisdiction of the payer – EU shell jurisdiction – third country shareholder jurisdiction

In this case only the source and the shell jurisdiction are bound by ATAD3 while the shareholder jurisdiction is not.

EU subsidiary: this entity will tax the outbound payment according to the treaty in effect with the third country jurisdiction of the shareholder or in the absence of such a treaty in accordance with its national law.

EU shell: will continue to be resident for tax purposes in a Member State and will have to fulfil relevant obligations as per national law, including by reporting the payment received; it may be able to provide evidence of the tax applied on the payment.

Third country shareholder: while the third country jurisdiction of the shareholder is not compelled to apply any consequences, it may be asked to apply a tax treaty in force with the source Member State in order to provide relief.

Scenarios where shell entity’s are resident outside the EU fall outside the scope of ATAD3.

What to do?

First of all, monitoring the developments in the BEPS 2.0 and ATAD 3 proposals is advised. Also, looking at whether there are operating entities withing the group in low tax jurisdictions, entities with primarily passive income, and companies where the local substance may fall short on the types of criteria suggested by the EC. When the key risks are identified, choices may include removing problematic holding companies, using different jurisdictions, or taking steps to bolster local substance. International groups should take the appropriate measures in time to get ahead of these changes.

Do you have questions regarding the implications of ATAD 3 for your company or do you need certainty in advance? Feel free to call us! This is really dynamic work, which also gives you insight into your compliance with the changing international rules. We are happy to help.

Today, the OECD releases the 2022 edition of the OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations.

The OECD Transfer Pricing Guidelines provide guidance on the application of the “arm’s length principle”, which represents the international consensus on the valuation, for income tax purposes, of cross-border transactions between associated enterprises. In today’s economy where multinational enterprises play an increasingly prominent role, transfer pricing continues to be high on the agenda of tax administrations and taxpayers alike. Governments need to ensure that the taxable profits of MNEs are not artificially shifted out of their jurisdiction and that the tax base reported by MNEs in their country reflects the economic activity undertaken therein and taxpayers need clear guidance on the proper application of the arm’s length principle.

This latest edition consolidates into a single publication the changes to the 2017 edition of the Transfer Pricing Guidelines resulting from:

The report Revised Guidance on the Transactional Profit Split Method, approved by the OECD/G20 Inclusive Framework on BEPS on 4 June 2018, and which replaced the guidance in Chapter II, Section C (paragraphs 2.114-2.151) found in the 2017 Transfer Pricing Guidelines and Annexes II and III to Chapter II;

The report Guidance for Tax Administrations on the Application of the Approach to Hard-to-Value Intangibles, approved by the OECD/G20 Inclusive Framework on BEPS on 4 June 2018, which has been incorporated as Annex II to Chapter VI;

The report Transfer Pricing Guidance on Financial Transactions, adopted by the OECD/G20 Inclusive Framework on BEPS on 20 January 2020, which has been incorporated into Chapter I (new Section D.1.2.2) and in a new Chapter X;

The consistency changes to the rest of the OECD Transfer Pricing Guidelines needed to produce this consolidated version of the Transfer Pricing Guidelines, which were approved by the OECD/G20 Inclusive Framework on BEPS on 7 January 2022.

For more information on the OECD Transfer Pricing Guidelines, visit https://oe.cd/tpg2022

Contacts:

Pascal Saint-Amans, Director of the OECD Centre for Tax Policy and Administration (CTPA) | Pascal.Saint-Amans@oecd.org

Manuel de los Santos, Acting Head of CTPA’s Transfer Pricing Unit | Manuel.DELOSSANTOS@oecd.org

Compliments of the OECD.

The post OECD releases latest edition of the Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.

A proposed $50-billion trust fund could help low-income and vulnerable middle-income countries build resilience to balance of payments shocks and ensure a sustainable recovery.

Even as countries continue to battle COVID-19, it is crucial not to overlook the longer-term challenge of transforming economies to become more resilient to shocks and achieve sustainable and inclusive growth. The pandemic has taught us that not addressing these long-term challenges in a timely manner can have significant economic consequences, with the potential for future balance of payments problems. Climate change is another long-term challenge that threatens macroeconomic stability and growth in many countries through natural disasters and disruptions to industries, job markets, and trade flows, among others.

‘It is the shared responsibility of individual countries and the international community to overcome these global public policy challenges.’

These are global public policy challenges, and it is the shared responsibility of individual countries and the international community to take timely actions. In a previous blog, we explained how the IMF is considering options for channeling some of the $650 billion SDRs issued in August 2021 from countries with strong external financial positions to vulnerable countries through a Resilience and Sustainability Trust, or RST. The RST’s central objective is to provide affordable long-term financing to support countries as they tackle structural challenges.

As we’ve continued to work toward developing the RST, our current thinking on the key design features—which we outline further below—aim to balance the needs of potential contributors and borrowing countries. With broad support from the membership and international partners, we hope that the Trust can be approved by the IMF Executive Board before the upcoming Spring Meetings and for it to become fully operational before the year’s end.

Key design features

Eligibility

About three quarters of the IMF’s membership could be eligible for RST financing. This would include all low-income countries, all developing and vulnerable small states, and all middle-income countries with per capita GNI below 10 times the 2020 IDA operational cutoff , or about $12,000.

Qualifying reforms

RST support aims to address macro-critical longer-term structural challenges that entail significant macroeconomic risks to member countries’ resilience and sustainability, including climate change, pandemic preparedness, and digitalization. That said, not all long-term structural challenges lend themselves to IMF lending. The ability to support reforms in a particular area would depend on the availability of and access to strong diagnostics, the ability to identify policy priorities, and develop the appropriate reform targets. Country ownership and strong commitment of the authorities to do the necessary reforms will be critical to catalyze the much-needed finance from multilateral development banks and the private sector. It is also critical to work in close coordination with other relevant institutions in order to leverage expertise and knowledge. The IMF and World Bank staff have worked closely to develop a coordination framework on RST operations on climate risks, building on earlier experience in supporting countries with structural reforms. Similar frameworks with relevant institutions will be developed in the coming months in this and other reform areas.

Qualification

To qualify for RST support, an eligible member would need: a package of high-quality policy measures consistent with the RST’s purpose; a concurrent financing or non-financing IMF-supported program with appropriate macroeconomic policies to mitigate risks for borrowers and creditors; and sustainable debt and adequate capacity to repay the Fund.

Financing terms

Like the IMF’s highly concessional and currently zero interest rate Trust for low-income countries (PRGT), the RST would be established under the IMF’s power to administer contributor resources, which allows for more flexible terms, notably on maturities, than the terms that apply to the IMF’s general resources. Consistent with the longer-term nature of balance of payments risks the RST seeks to address, its loans would have much longer maturities than traditional IMF financing. Specifically, staff has proposed a 20-year maturity and a 10-year grace period. A tiered interest structure would differentiate financing terms across country groups, with a high degree of concessionality for lower-income members.

Access to financing

Access to RST financing would be determined case by case, based on the strength of reforms and debt sustainability considerations, and is expected to be capped at 150 percent of IMF quota or SDR 1 billion, whichever is smaller. RST lending would be part of a broader financing strategy members would pursue to address longer-term balance of payments risks, involving a mix of multilateral, bilateral official, and private financing.

Financial architecture

Like the PRGT, the RST’s resources would be mobilized on a voluntary basis from members who wish to channel their SDRs or currencies for the benefit of poorer or vulnerable countries . The financial architecture of the RST is designed to ensure that substantial resources for low-cost long-maturity loans can be mobilized while ensuring the safety and liquidity of contributors’ claims on the Trust based on a multilayered risk management framework that maintains the reserve asset nature of channeled SDRs. To meet the projected demand, the RST would need to mobilize initially around $50 billion in total resources. A smooth functioning SDR trading market would underpin successful RST operations.

Collaboration essential for success

Mitigating economic risks from long-term structural challenges requires a consistent and deliberate approach, with strong commitment from policymakers to undertake sometimes difficult reforms. And where such commitment is evident, the international community can help with affordable financing, capacity building, and policy advice. The RST will support such a collaborative effort. We will build on our experience of working with the World Bank and other international institutions and regional development banks, complementing their lending to provide the best support to member countries.

The success of the new Trust will depend equally on economically stronger IMF members providing meaningful resources to help countries improve long-term resilience and sustainability; borrowers willing to go the extra mile to achieve the macroeconomic environment and reform framework conducive to improving balance of payments stability; other international financial institutions supporting with their expertise, knowledge, and financing where feasible. These actions would also help mobilize private sector investment.

Faced with a range of long-term structural challenges that require global action, it has never been more important to support all countries tackle these challenges at an early stage and achieve sustainable growth. The RST could help achieve this goal.

Authors:

Ceyla Pazarbasioglu is Director of the Strategy, Policy, and Review Department (SPR) of the IMF

Uma Ramakrishnan is currently Deputy Director of the IMF’s Strategy, Policy and Review Department

Compliments of the IMF.

The post IMF | A New Trust to Help Countries Build Resilience and Sustainability first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.

Today, European society needs the contribution of universities and other higher education institutions more than ever. Europe is facing major challenges such as climate change, the digital transformation and aging population, at a time when it is hit by the biggest global health crisis in a century and its economic fall-out. Universities, and the entire higher education sector, have a unique position at the crossroads of education, research and innovation, in shaping sustainable and resilient economies, and in making the European Union greener, more inclusive and more digital.

The two new initiatives adopted today, a European strategy for universities and a Commission proposal for a Council Recommendation on building bridges for effective European higher education cooperation, will support universities in this endeavour.

Margaritis Schinas, Vice-President for Promoting the European Way of Life, said: “European Universities of excellence and inclusiveness are both a condition and a foundation for our European Way of Life. They support open, democratic and fair societies as well as sustained growth, entrepreneurship, integration and employment. With our proposals today, we seek to take transnational cooperation in Higher Education to a new level. Shared values, more mobility, broader scope and synergies to build a genuinely European dimension in our Higher Education.”

Commissioner for Innovation, Research, Culture, Education and Youth, Mariya Gabriel, said: “Today’s proposals will benefit the entire higher education sector, first and foremost our students. They need modern transnational campuses with easy access to mobility abroad to allow for a truly European study path and experience. We stand ready to join forces with the Member States and higher education institutions across Europe. Together we can bring closer education, research and innovation in service to society. The European Universities alliances are paving the way; by mid-2024 the European budget will support up to 60 European Universities Alliances with more than 500 universities across Europe.”

The European strategy for universities

Europe is home to close to 5,000 higher education institutions, 17.5 million tertiary education students, 1.35 million people teaching in tertiary education and 1.17 million researchers. This strategy intends to support and enable all universities in Europe to adapt to changing conditions, to thrive and to contribute to Europe’s resilience and recovery. It proposes a set of important actions, to support Europe’s universities towards achieving four objectives:

Strengthen the European dimension of higher education and research;

Consolidate universities as lighthouses of our European way of life with supporting actions focusing on academic and research careers, quality and relevance for future-proof skills, diversity, inclusion, democratic practices, fundamental rights and academic values;

Empower universities as key actors of change in the twin green and digital transition;

Reinforce universities as drivers of EU’s global role and leadership.

Building bridges for effective European higher education cooperation

The Commission proposal for a Council Recommendation aims to enable European higher education institutions to cooperate closer and deeper, to facilitate the implementation of joint transnational educational programmes and activities, pooling capacity and resources, or awarding joint degrees. It is an invitation to Member States to take action and create appropriate conditions at national level for enabling such closer and sustainable transnational cooperation, more effective implementation of joint educational and research activities and the European Higher Education Area (Bologna) tools. It will facilitate the flow of knowledge and build a stronger link between education, research and innovative industrial communities. The objective is notably to support the provision of high-quality life-long learning opportunities for everyone with a focus on the most needed skills and competences to face today’s economic and societal demands.

Making it happen: four flagship initiatives

The European dimension in higher education and research will be boosted by four flagships initiatives by mid-2024:

Expand to 60 European Universities with more than 500 higher education institutions by mid-2024, with an Erasmus+ indicative budget totalling €1.1 billion for 2021-2027. The aim is to develop and share a common long-term structural, sustainable and systemic cooperation on education, research and innovation, creating European inter-university campuses where students, staff and researchers from all parts of Europe can enjoy seamless mobility and create new knowledge together, across countries and disciplines.

Work towards a legal statute for alliances of higher education institutions to allow them to pool resources, capacities and their strengths, with an Erasmus+ pilot as of 2022.

Work towards a joint European degree to recognise the value of transnational experiences in the higher education qualification the students obtain and cut the red tape for delivering joint programmes.

Scale-up the European Student Card initiative by deploying a unique European Student Identifier available to all mobile students in 2022 and to all students in universities in Europe by mid-2024, to facilitate mobility at all levels.

Next Steps

Coordination of efforts between the EU, Member States, regions, civil society and the higher education sector is key to make the European strategy for universities a reality. The Commission invites the Council, Member States and universities to discuss on this policy agenda and work jointly towards future-proof universities.

The Commission proposal for a Council recommendation on building bridges for effective European higher education cooperation will be discussed with Member States. Once adopted by the Council, the Commission will support Member States and relevant partners in implementing this Council Recommendation.

Background

The Commission announced its intention to initiate the co-creation of a transformation agenda for higher education in its Communication on Achieving the European Education Area by 2025 and its Communication on a new European Research Area. The Council Conclusions on the New European Research Area, adopted on 1 December 2020, stress “that stronger synergies and interconnections between the ERA, the EHEA and the higher education related elements of the European Education Area (EEA), are to be developed”. In its Resolution of 26 February 2021 on ‘a strategic framework for European cooperation in education and training towards the European Education Area and beyond (2021-2030)’, the Council has identified the establishment of an agenda for higher education transformation as a concrete action in the priority area of higher education.

The ERA Policy Agenda annexed to the Council Conclusions on the Future Governance of the European Research Area, adopted on 26 November 2021, support actions relevant for universities including a dedicated action on empowering higher education institutions to develop in line with the European Research Area and in synergy with the European Education Area.

Compliments of the European Commission.

The post Higher education: making EU’s universities ready for the future through deeper transnational cooperation first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.