The Transatlantic Business & Investment Council (TBIC) is the official European representative for selected counties, cities and corporations from over 30 U.S. States. It is our mission to promote transatlantic trade and investment. To that end, TBIC bridges the gap between U.S. Economic Development Organizations (EDOs) and European investors looking to enter or expand in the U.S. market.

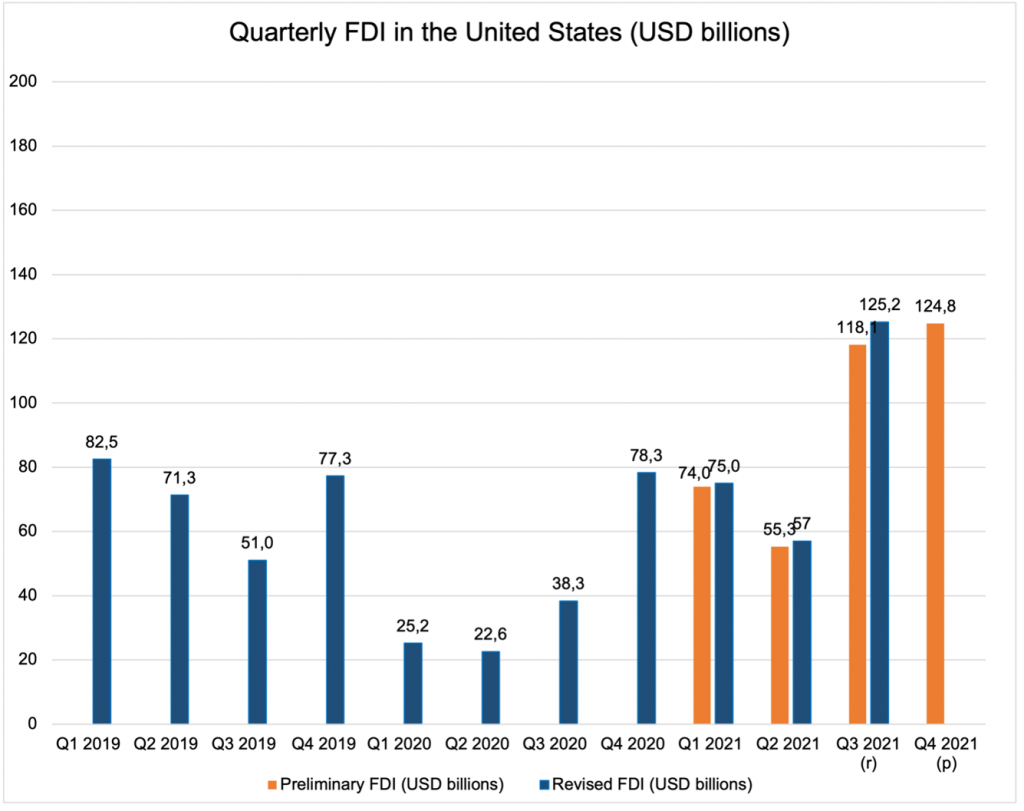

This latest issue of our quarterly features an analysis of the newly published preliminary (p) data for Q4 2021 and partially revised data (r) for Q3 2021, as recently released by the U.S. Bureau of Economic Analysis (BEA). With $124.8 billion worth of investment, the fourth quarter of 2021 finished slightly below Q3 2021, which witnessed the strongest inflows of FDI to the United States since 2018.

Overall FDI inflows to the U.S. in 2021 – $382 billion – more than doubled compared to the total volume of FDI flows recorded in 2020 – $164.4 billion. The 2021 FDI inflows were also 1.4 times higher than in 2019.

The strong rebound for the machinery sector FDI in Q3 2021 abated in Q4 according to the preliminary numbers, as did investment in the food sector. With that said, Q4 2021 saw an estimated $4.1 billion quarterly investment flow, making it the second strongest quarter in over two years for this sector.

This edition also includes a time series focusing on French foreign direct investments to the United States. In addition to the recent French presidential elections between far-right politician Marie Le Pen and center-left incumbent President Emmanuel Macron, France will also host the upcoming U.S.-E.U. Trade and Technology Council meeting on May 15 and 16.

The U.S. is the second largest source of FDI in France while the country is the fifth largest source of FDI in the United States. In the lead up to the election, Le Pen continually supported economic protectionism that would likely have hindered the trade relations between the two countries. As an important source of FDI for the U.S., President Macron’s success in the 2022 presidential elections is an encouraging sign for the continued partnership and mutually beneficial, bilateral trade relations between the two countries.

In this analysis, the TBIC corroborates relevant country data with its own experience of working at the frontier of transatlantic investments: the TBIC regularly visits key markets in Europe that have become drivers of FDI in the United States as part of delegation trips offered exclusively to our members. These trips feature meetings with decision-makers from companies looking to invest in the United States as well as key multipliers from diplomatic missions and industry associations. After more than a year of online events, the TBIC switched back to the in-person format in September 2021. Regulations across both the U.S. and E.U. have been lifted and we are thrilled to once again be able to welcome our U.S. members to Europe and facilitate meaningful and fruitful connections with prospective European investors.

In addition to our FDI analysis, this edition features our latest spotlight article both on how the aviation and aerospace industry faired through the pandemic, but additionally provides an in-depth outlook on developments and trends we can expect in the months and years ahead.

Find a PDF version of this document here.

Foreign Direct Investment in the United States: Key Figures

In the recently published data of the U.S. Bureau of Economic Analysis (BEA), the quarterly FDI inflows for the third quarter of 2021 were revised upward from $118.1 to $125.2 billion.

Meanwhile, the preliminary data for the fourth quarter of 2021 projects a volume of inwards investment of $124.8 billion, the second highest quarterly volume since the outbreak of the COVID-19 pandemic. On a year-to-year basis, FDI inflows in Q4 2021 were more than 60 percent higher than in Q4 2020.

According to UNCTAD’s January 2022 Investment Trends Monitor, FDI inflows to the United States increased by 114 percent in 2021. UNCTAD furthermore assessed there was a boom in cross-border M&As, whose value almost tripled to $285 billion in the U.S. in 2021. BEA data shows FDI inflows to the U.S. in 2021 – $382 billion – more than doubled compared to the total volume of FDI flows recorded in 2020 – $164.4 billion. The 2021 FDI inflows were also 1.4 times higher than in 2019.

Source: Bureau of Economic Analysis (BEA), U.S. International Transactions, Fourth Quarter 2021, March 2022

U.S. FDI Inflows by Key Industry Sector

The newly released BEA preliminary data for Q4 shows a downward trend in net FDI flows in the food and machinery sectors compared to Q3. In Q4, investment flows in the food sector decreased by $0.8 to 2 billion while investment flows in the machinery sector declined by $1.3 billion. Transportation equipment investments bucked this trend and increased by an estimated $0.6 billion.

Investments in the transportation equipment sector outperformed those in the machinery and food sectors. Including Q4’s preliminary data, transport equipment sector investments totaled $12.7 billion in 2021 compared to $10.9 billion in the machinery and $6.3 billion in the food sector.

The strong rebound for the machinery sector FDI in Q3 2021 abated in Q4. However, with an estimated $4.1 billion quarterly investment flow, Q4 remained the second strongest quarter in over two years for this sector.

Similarly, investments in the food industry also contracted during the fourth quarter of 2021, with a financial flow estimated at $2 billion. Accordingly, Q4 2021 is expected to be the third strongest quarter for FDI to the food sector since the onset of the pandemic.

Source: Bureau of Economic Analysis (BEA), Foreign Direct Investment in the United States: Country and Industry Detail for Financial Transactions, March 2022.

U.S. FDI Inflows by Key European Source Countries

Quarterly inflows from Germany, the United Kingdom and Switzerland for Q3 2021 were revised by the BEA. German and British FDI inflows were corrected upwards from $10.4 to 11.7 billion for the former and from $ 5.2 to 10.7 billion for the latter. Meanwhile, Swiss FDI was readjusted downwards, from $3.2 to minus 27 million.

German FDI is expected to reach $7.4 billion in the fourth quarter of 2021, the same value as in Q4 2020. FDI inflows from Europe’s largest economy have thus proven relatively stable over the course of 2021 as compared to the other two countries under analysis.

FDI from the United Kingdom recovered somewhat after it dropped to $2 billion in Q2 2021 and after two quarters marked by exceptionally high investments. In Q3 2021, FDI flows from the United Kingdom’s rose to $10.7 billion, while in Q4 FDI flows are estimated to total $5.3 billion. Meanwhile, Swiss FDI increased from minus $27 million to 3.6 billion between the third and fourth quarter of 2021.

Taken together, the quarterly investment flows show the United Kingdom ranked first among the three countries with a total investment of 52.4 billion in 2021, which is to be expected given its outsized role in international finance. Germany ranked second with $50 billion in annual investment flows followed by Switzerland with $7.9 billion.

Source: Bureau of Economic Analysis (BEA), Foreign Direct Investment in the United States: Country and Industry Detail for Financial Transactions, March 2022.

Historical Series 2: French FDI Inflows to the U.S.

The graph below features our third time series, dedicated to the development of French foreign direct investments to the United States. FDI inflows from France to the U.S. continue to play an important role for the U.S. economy. In 2020, France was the fifth largest investor in the United States and the largest foreign investor in R&D in computer and electronic products. After a decline in 2018, French FDI inflows to the U.S. are again on an upward trajectory, particularly in Q3 and Q4 of last year. As of 2019, French FDI was supporting 765,100 jobs in the United States. One third of all French subsidiaries in the U.S. are in the manufacturing sector, offering employment to 227,600 Americans.

Many well-known French companies like oil and gas giant Total Groupe, luxury goods conglomerate Louis Vuitton Moet Hennesy, tire manufacturer Michelin, and airline manufacturer Airbus have a strong footprint in the U.S. In addition, French FDI is a major driver of innovation. France is the fourth largest country of ownership for patents granted by the U.S. Patent and Trademark Office according to the French Treasury in the United States.

Aware of the many opportunities that this fast-growing source of FDI has to offer, the TBIC regularly visits leading companies and business executives in Austria to assist them in their expansion to the U.S. market.

Source: Bureau of Economic Analysis (BEA), Foreign Direct Investment in the United States: Country and Industry Detail for Financial Transactions, March 2022.

TBIC Spotlight Article: Trends in the Aviation and Aerospace Sector

With the world slowly reopening after nearly two years, many are taking stock of all that has changed during that time. While all industries have certainly been altered by the pandemic, aviation and aerospace were particularly impacted as the global ebb and flow of people and goods came to a halt with the raising of borders and restrictions in 2020. In this edition of our newsletter, we wanted to give our members a retrospective look at some of the most important developments the industry, as well as offer an outlook on the bright future of aviation and aerospace technologies.

The pandemic undeniably required airlines to adjust their business models. According to a 2021 report by the Aerospace and Defense Industries Association of Europe, flights were reduced by almost 90% at the peak of the crisis. While this did have knock-on effects throughout the industry, the pandemic also revealed new opportunities. As lockdowns and quarantine restrictions pushed online shopping to new heights, coupled with severe delays at ports across the US, air freight cargo represented a way to help buoy airline companies as they weathered the pandemic restrictions. 2022 is expected to be a record breaker with air cargo revenue expected to reach $175 billion USD.

In addition to this, the longer-term nature of aerospace and defense contracts helped to buffer some of the impact of the pandemic. In a 2021 survey by McKinsey, 52% of European aerospace and defense respondents anticipated increases in investment for 2021 and beyond. In the United States, government contracts from the Pentagon, helped to further provide steady revenue streams for airlines.

Assistance from the government has been essential to helping keep aviation and aerospace manufacturing jobs afloat. In February 2022, the U.S. Department of Transportation announced that in its third round of Covid-19 relief funding, it was offering an additional $69 Million USD to aviation manufacturing and repair businesses. This brings the total amount of funding to nearly $673 million USD, helping support 31,000 jobs in 43 states.

This year, global aviation is at long last bouncing back. A recent survey found that 47% of respondents anticipate an increase in sector as a whole in 2022. Intra-regional flights are already expected to reach near pre-pandemic levels this year, with inter-regional flights between North America, Asia, and Europe following suit in 2023.

Source: McKinsey analysis of global airline demand; PaxIS

The aviation and aerospace industry is not just returning to old ways, however. The sector, as many others, has been reshaped by the events of the last two years. Customers’ concerns and governmental regulations have pushed for sustainability and carbon-neutrality. The design of planes and propulsion systems are changing to reduce CO2emissions in the fight against climate change. In Europe, Destination 50 is the aviation industry’s path to net zero emissions. Similarly, at the end of last year, the Biden Administration and the Department of Transportation announced their own goal if achieving net zero emissions from the United States’ aviation industry by 2050.

Achieving these goals requires investment into new and novel technologies. In both Europe and the U.S., sustainable aviation fuels (SAFs) are the clear front-runner in the short- and medium-term to cut emissions in the industry. Earlier this year, Airbus announced their intent to develop the first zero-emission commercial airplane by 2035.

The future of aviation, however, will reconfigure how we conceptualize mobility. The advance air mobility (AAM) market is expected to reach between $300 billion to $500 billion USD by 2040 – the U.S. market alone is expected to reach $115 billion by 2035. This influx of investment not only represents new technologies, but also a diversification in who’s investing. Beyond venture capital, AAM has investments special purpose acquisition companies (SPACs), as well as established aviation and aerospace companies internally investing in R&D.

Aviation and aerospace may have taken a hit during the pandemic, but the outlook going forward is positive. With events like the ILA Airshow in Berlin and the Farnborough Airshow just outside London, these big-name, in-person events are companies and investors chance to highlight their return to the market and showcase the future of aviation and aerospace.

Author:

Matthias Beier, President & CEO, TBIC

Compliments of the Transatlantic Business & Investment Council (TBIC) – a partner of the EACCNY.

The post TBIC | Transatlantic Foreign Direct Investment Analysis and Trends, 2nd Quarter 2022 first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.