Inflation will remain high at the start of 2022 but will fall later on, especially towards the end of the year, Chief Economist Philip R. Lane tells Verslo žinios. Our current projections foresee inflation below the 2% target in 2023 and 2024.

I just read the news this morning that the latest Purchasing Managers’ Index published this Monday shows that the eurozone economic recovery weakened further in January. This is due to the new restrictions imposed to contain the Omicron variant of the coronavirus (COVID-19). So what is your opinion on the state of the eurozone today, after two years of the pandemic and what are the prospects?

In the near term, there are some risks from the Omicron variant. But I think it’s increasingly clear that the impact is only for a few weeks. So it is not turning out to be a factor that will influence the activity levels for the year, it’s more the activity levels for a few weeks. In that sense, I think there’s less concern about Omicron than we had in December. In terms of the overall pandemic, I think it is fair to say that the recovery so far has been stronger than expected − compared to, for example, early 2020 when the pandemic hit. In the initial months of the pandemic there was a lot of concern. But essentially, when the vaccines have been rolled out during 2021, it turned out that the euro area economy and the world economy has recovered more quickly than expected. And looking to this year, 2022, we expect another strong year of recovery. So essentially, there’s been a strong recovery, supported by a lot of policy measures, both fiscal policy and monetary policy. I think in overall terms the sense is that, between the public health measures and other measures, it’s turning out that we can hope that the euro area can recover quite well from the pandemic.

Let’s go to the start of the pandemic. The euro area economy as a whole shrank more than 6 per cent in 2020. However, Ireland’s economy grew 3.4 per cent. And the Lithuanian economy escaped the recession too. To your mind, why did the Lithuanian economy and the Irish economy manage to decouple from the recessionary trends in the euro area last year?

What I think is that some sectors in the world economy were able to continue during the pandemic. So in those sectors where the pandemic might cause an interruption for a few months, even during 2020 it turned out there was a good recovery. The sectors where Lithuania is a big producer and the sectors where Ireland is a big producer, including a lot of multinational firms, turned out to be quite strong. But I would say both in Ireland and in Lithuania many sectors suffered. The fact that in overall terms, these economies did grow, should not take away from the fact that many service-type industries would have been damaged by the pandemic.

Euro area inflation hit a record high of 5 per cent in December of last year. Are you worried about further rising inflation in the eurozone?

We should think about these years of the pandemic, 2020, 2021 and 2022 as part of a pandemic cycle. In the first year 2020, inflation was relatively low. In the second half of 2021, inflation turned out to be quite high. And then, as we look into this year, 2022, we think inflation will remain high at the start of this year, but will fall later this year, especially towards the end of the year. So it’s a year, essentially, where in the first part of the year, we’ll still see inflation remaining high. But we do expect it to fall quite a bit later this year.

Do you expect inflation to rise further than 5 per cent at the start of the year? And what levels do you expect at the end of the year?

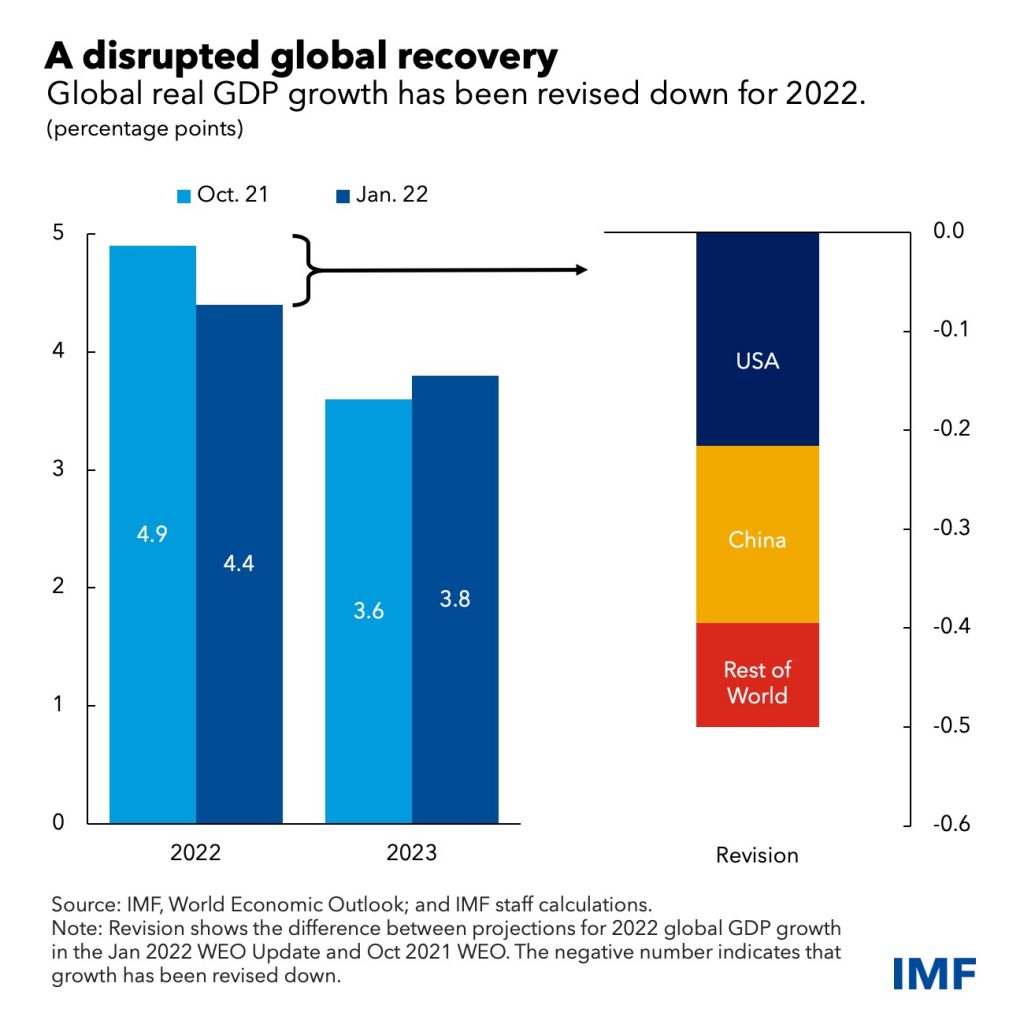

We are clear from our December forecast that we expect inflation − in overall terms for this year − to be around 3.2 per cent in the euro area, and then to be below 2 per cent in 2023 and 2024. Compared with the peak, that’s quite a big decline. We will see exactly the timing of how quickly inflation falls. So rather than focus on month by month, we have a clear vision in terms of the overall direction: that the inflation rate will fall later this year. And in fact, as you know, our current view from December is that inflation will fall below the 2 per cent target in the next couple of years.

What ECB monetary policy adjustments do you expect in the face of rising energy goods and services prices if the rise is higher than your forecasts?

I think we are always clear that we’re guided by our intentions to deliver an inflation rate of 2 per cent over the medium term. So we will adjust all of our policies − whether that’s asset purchases, the targeted lending programme, our interest rates − to deliver that goal. You’ve given me a hypothetical, the hypothetical is: what happens if inflation is above our forecast. So let me in turn make clear that what is very important is whether inflation will essentially settle at around our target of 2 per cent, which would be essentially what we want, or whether there might be signs of inflation being above 2 per cent in a significant way for a significant amount of time. And if we saw the data coming in to suggest that inflation would be too high relative to 2 per cent, then of course we would respond. We also have been clear on our sequence. The first decision under that scenario would be to end net purchasing. And only after ending net asset purchases would we look at the criteria for raising the interest rates. So we will be driven by the data, driven by our assessment. And every month, every quarter, we’re going to learn more about where the data are going.

Is there a risk of inflationary second round effects such as salary growth?

We spend a lot of time looking at the interlinkages. One linkage is that an increase in the cost of living may be a factor in wage negotiations. We think that is clear. The question is how much, because, remember, energy is both a direct cost to the consumer, but also a cost to other firms. Rising energy prices can also mean rising food prices, rising prices of goods and services. We are also examining how much the increase in energy prices might show up in rising goods prices and services prices. So far, we do not see a big response of wages. We do expect a response of wages but what is critical is how big. Because, remember, in the euro area, for inflation to be around 2 per cent and allowing for a typical increase in labour productivity of about 1 per cent, then wages should be growing around 3 per cent a year in the euro area on average to be consistent with the 2 per cent target. We are not, right now, seeing wage increases in that zone. But of course, we will continue to look at this throughout the year.

Some of your colleagues have mentioned another risk. Do you see any pressure to the rise of inflation in the euro area due to the green energy investments?

I think this is a complicated issue. Let me also emphasise that what we have right now is an increase in global energy prices. The euro area imports energy from the rest of the world. So this is a very different scenario from a scenario, which we would expect to occur in the coming years. Which is essentially, if there’s, for example, policies that increase the price of carbon, as part of the transition away from a high-carbon economy. If we see an increase in the price of carbon because of taxes or regulation, driven by domestic policy, those revenues from a carbon tax, for example, can be recycled in the domestic economy and can stimulate the economy. Wheras what we have right now is different. We have an increase in import prices from the rest of the world. And this is reducing living standards, increasing the import bill. It has a negative channel to lower incomes, lower consumption. So I think it’s a very interesting, very important debate about the future of green energy policies. That is playing some role right now. But the main role right now is a global issue, rather than the transition. So we will return to this topic, no doubt.

So overall, what scenarios do you see where interest rates in the eurozone could be lifted?

Let me mention three scenarios. And again, to repeat, we’re examining hypotheticals here. One scenario is in fact that the forces that generated low inflation before the pandemic essentially become visible again after the pandemic. So one scenario is that the world economy will return to quite low inflation rates. A second scenario is that some of these headwinds will not return and, in fact, it may be easier for us to deliver our target of 2 per cent. So that is a kind of middle scenario where inflation will stabilise at 2 per cent. And then the third scenario is, if inflation picks up and there is a risk that inflation will be significantly above 2 per cent. In this third scenario, where inflation is significantly above 2 per cent on a persistent basis, then that will call for a monetary policy tightening. We would have to respond. In the middle scenario where inflation stabilises at 2 per cent, then clearly over time we would normalise monetary policy. The policies we need to fight very low inflation would no longer be needed if inflation were stable around 2 per cent. And in the first scenario where inflation is significantly below 2 per cent, then the policies that we have employed to fight low inflation would still remain relevant. So this is the way I think about the world, but there are three scenarios. One, we remain with a low inflation problem. Two, we stabilise — in a kind of smooth way — inflation around 2 per cent. And three, if inflation turns out to be persistently above 2 per cent, we would have to tighten. And so those are three very different scenarios.

Which of these three scenarios do you see as the most likely scenario in this economic environment?

In the December round of projections, the assessment was that, in fact, we saw inflation returning to below 2 per cent. But we also emphasised that in a world of uncertainty, as we have more data come in, of course the data can change. But in the euro area context, I would say that it’s also possible that we may enter a world where inflation stabilises around 2 per cent. I find it less likely to think about a scenario where inflation is persistently, significantly above 2 per cent, which would require a serious tightening. That scenario, would, I think, in the context of the euro area, be less likely than the other two scenarios.

Higher sovereign borrowing costs after the financial crisis of 2007-09 turned into a eurozone debt crisis in 2010-13 that hit some southern European Member States, also Ireland. Debt levels have significantly risen during the pandemic. Is there any risk of another debt crisis this time provided interest rates will rise?

Let me make two important points here. One, at that time, there was a significant combination which, by and large, countries had of both high private sector debt – many households, many firms were highly indebted – and there was high government debt. That is a major problem. What we’ve seen in this pandemic is: yes, governments have borrowed more, and some types of firms have borrowed more. But households have been saving a lot. In the banking sector, we also have banks which are better able to handle debt, because they have increased their capital positions. So, when you have a situation where, essentially, in the euro area, debt levels have gone up for the sovereign and for some corporates but have gone down for households, and where the banks, that are kind of in the middle of the system, are in better shape, then I think it’s a different scenario to ten years ago. And then the other issue is: we think the trend level of interest rates is lower today than ten years ago. So, when interest rates go up, it’s from a very low level. And that’s important.

Finally, I have one question as to the elephant in the room: the deteriorating geopolitical situation in Ukraine these days due to the possible Russian military offensive. Do you see any side effects to the ECB monetary policy, should the geopolitical situation in Europe deteriorate further?

Geopolitics always matters. I think if you look at the history of the world economy, the European economy, geopolitical events matter a lot via trade, via global prices, via uncertainty. So, of course, we will be looking very closely at such factors. We already talked about the very high energy prices. And of course, there’s a connection between higher energy prices and these tensions. So of course, it’s very directly relevant for us.

Compliments of the European Central Bank.

The post ECB Interview | Inflation expected to decline over 2022 first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.

25

Jan