Upside risks to the inflation outlook remain large, and more aggressive tightening may be needed if these risks materialize.

Central banks in major economies expected as recently as a few months ago that they could tighten monetary policy very gradually. Inflation seemed to be driven by an unusual mix of supply shocks associated with the pandemic and later Russia’s invasion of Ukraine, and it was expected to decline rapidly once these pressures eased.

Now, with inflation climbing to multi-decade highs and price pressures broadening to housing and other services, central banks recognize the need to move more urgently to avoid an unmooring of inflation expectations and damaging their credibility. Policymakers should heed the lessons of the past and be resolute to avoid potentially more painful and disruptive adjustments later.

The Federal Reserve, Bank of Canada, and Bank of England have already raised interest rates markedly and have signaled they expect to continue with more sizable hikes this year. The European Central Bank recently lifted rates for the first time in more than a decade.

Higher real rates to help push down inflation

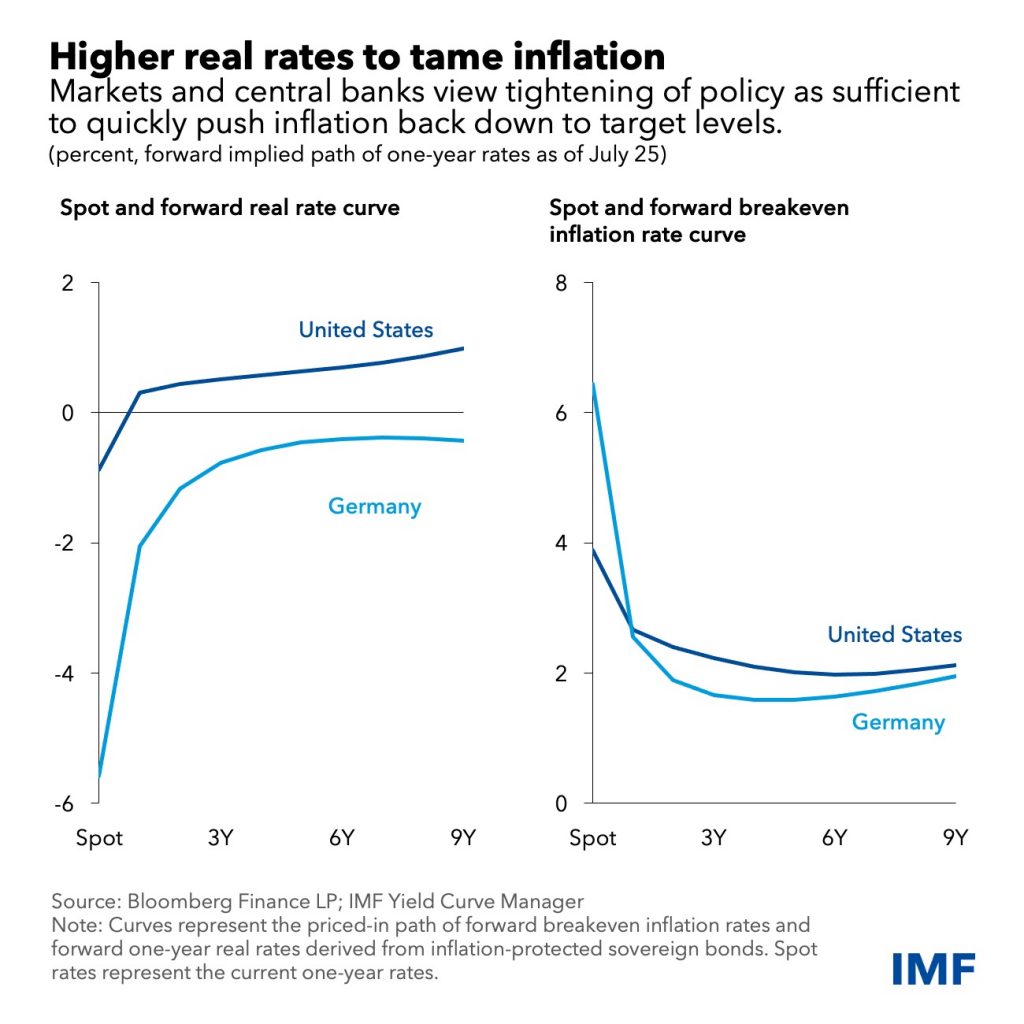

Central bank actions and communications about the likely path of policy have led to a significant rise in real (that is, inflation-adjusted) interest rates on government debt since the start of the year.

While short-term real rates are still negative, the real rate forward curve in the United States—that is, the path of one-year-ahead real interest rates one to 10 years out implied by market prices—has risen across the curve to a range between 0.5 and 1 percent.

This path is roughly consistent with a “neutral” real policy stance that allows output to expand around its potential rate. The Fed’s Summary of Economic Projections in mid-June suggested a real neutral rate of around 0.5 percent, and policymakers saw a 1.7 percent output expansion both this year and next, which is very close to estimates of potential.

The real rate forward curve in the euro area, proxied by German bunds, has also shifted up, though remains deeply negative. That’s consistent with real rates converging only gradually to neutral.

The higher real interest rates on government bonds have spurred an even larger rise in borrowing costs for consumers and businesses, and contributed to sharp declines in equity prices globally. The modal view of both central banks and markets seems to be that this tightening of financial conditions will be enough to push inflation down to target levels relatively quickly.

To illustrate, market-based measures of inflation expectations point to a return of inflation to around 2 percent within the next two or three years for both the United States and Germany. Central bank forecasts, such as the Fed’s latest quarterly projections, point to a similar moderation in the rate of price increases, as do surveys of economists and investors.

This seems to be a reasonable baseline for several reasons:

The monetary and fiscal tightening in train should cool demand both for energy and non-energy goods, especially in interest-sensitive categories like consumer durables. This should cause goods prices to rise at a slower pace or even fall, and may also push energy prices lower in the absence of additional disruptions in commodity markets.

Supply-side pressures should ease as the pandemic relaxes its grip and lockdowns and production disruptions become less frequent.

Slower economic growth should eventually push down service-sector inflation and restrain wage growth.

Substantial risk inflation runs high

However, the magnitude of the inflation surge has been a surprise to central banks and markets, and there remains substantial uncertainty about the outlook for inflation. It is possible that inflation comes down more quickly than central banks envision, especially if supply chain disruptions ease and global policy tightening results in fast declines in energy and goods prices.

Even so, inflation risks appear strongly tilted to the upside. There is a substantial risk that high inflation becomes entrenched, and inflation expectations de-anchor.

Inflation rates in services—for everything from housing rents to personal services—appear to be picking up from already elevated levels, and they are unlikely to come down quickly. These pressures may be reinforced by rapid nominal wage growth. In countries with strong labor markets, nominal wages could start rising rapidly, faster than what firms reasonably could absorb, with the associated increase in unit labor costs passed into prices. Such “second round effects” would translate into more persistent inflation and rising inflation expectations. Finally, a further intensification of geopolitical tensions that ignites a renewed surge in energy prices or compounds existing disruptions could also generate a longer period of high inflation.

While the market-based evidence on “average” inflation expectations discussed above may seem reassuring, markets appear to put significant odds on the possibility that inflation may run well above central bank targets over the next few years. Specifically, markets signal a high probability of inflation rates of over 3 percent persisting in coming years in the United States, euro area and the United Kingdom.

Consumers and businesses have also become increasingly concerned about upside inflation risks in recent months. For the United States and Germany, household surveys show that people expect high inflation over the next year, and put considerable odds on the possibility that it runs well above target over the next five years.

More forceful tightening may be needed

The costs of bringing down inflation may prove to be markedly higher if upside risks materialize and high inflation becomes entrenched. In that event, central banks will have to be more resolute and tighten more aggressively to cool the economy, and unemployment will likely have to rise significantly.

Amid signs of already poor liquidity, faster policy rate tightening may result in a further sharp decline in risk asset prices—affecting equities, credit, and emerging market assets. The tightening in financial conditions may well be disorderly, testing the resilience of the financial system and putting especially large strains on emerging markets. Public support for tight monetary policy, now strong with inflation running at multi-decade highs, may be undermined by mounting economic and employment costs.

Even so, restoring price stability is of paramount importance, and is a necessary condition for sustained economic growth. A key lesson of the high inflation in the 1960s and 1970s was that moving too slowly to restrain it entails a much more costly subsequent tightening to re-anchor inflation expectations and restore policy credibility. It will be important for central banks to keep this experience firmly in their sights as they navigate the difficult road ahead.

Authors:

Tobias Adrian

Christopher Erceg

Fabio Natalucci

Compliments of the IMF.

The post IMF | Soaring Inflation Puts Central Banks on a Difficult Journey first appeared on European American Chamber of Commerce New York [EACCNY] | Your Partner for Transatlantic Business Resources.